{kind=link}

Courtesy of Pam Martens.

A Majority of Americans Do Not Have a Rainy Day Fund That Would Last 3 Months

Any ideas that household balance sheets in the U.S. have been repaired since Wall Street took a wrecking ball to the nation’s economy in 2008 were dashed with the release of a study earlier this month by the Federal Reserve. As Federal Reserve Chair Janet Yellen ponders what will happen in the markets when the Fed starts to eventually raise interest rates, she has to also worry about what will happen to the cash-strapped consumer who is barely hanging on and has no emergency funds to meet a job loss or hike in credit card interest payments.

The Fed study was conducted in September 2013 by the Fed’s Division of Consumer and Community Affairs. Its stated aim was to “capture a snapshot of the financial and economic well-being of U.S. households, as well as to monitor their recovery from the recent recession and identify any risk to their financial stability.”

The Fed didn’t receive welcome news.

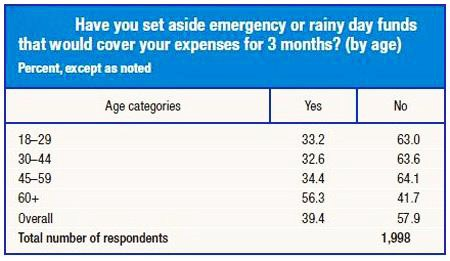

One question in the survey asked respondents if they had set aside an emergency or rainy day fund that would cover three months of living expenses. (See a previous article from Wall Street On Parade on why a rainy day fund needs more than three months of expenses.) Shockingly, the respondents providing an affirmative “no” to the answer went up, instead of down, in the older groups, until age 60. Persons answering “no” in the 18 to 29 age group came in at 63 percent; 63.6 percent of the age category 30 to 44 said “no”; and 64.1 percent of those aged 45 to 59 said “no.” For respondents aged 60 and over, 41.7 percent reported having no rainy day fund. Among respondents of all ages, a majority, 57.9 percent, answered no to the question.

This is not the financial tanker that any Fed Chairman wants to contemplate navigating through future storm waters – particularly a Fed with a $4.3 trillion balance sheet which will restrain its ability to flood the markets again with liquidity in a major downturn – and zero historical perspective on what happens if you hike rates when a majority of Americans are financially struggling. (The survey found that only 48 percent of Americans could raise $400 in an emergency from their own checking, savings, or borrowing on a credit card which they would pay off when the next statement arrived.)

…