Courtesy of Mish.

Central bankers still have not figured out the absurdity of their efforts to cure deflation via low interest rates. By forcing down interest rates and encouraging more lending, debts of all sorts keep piling up with no realistic way of paying those debts off.

Debt and (Not Much) Deleveraging

Inquiring minds are digging into a fascinating albeit lengthy (256 page) McKinsey study of debt and deleveraging since the great financial crisis seven years ago: Debt and (Not Much) Deleveraging

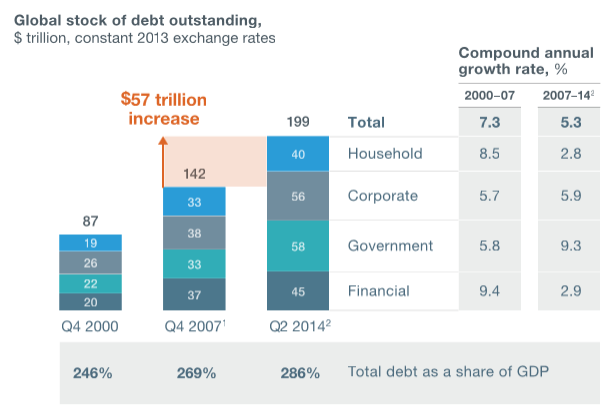

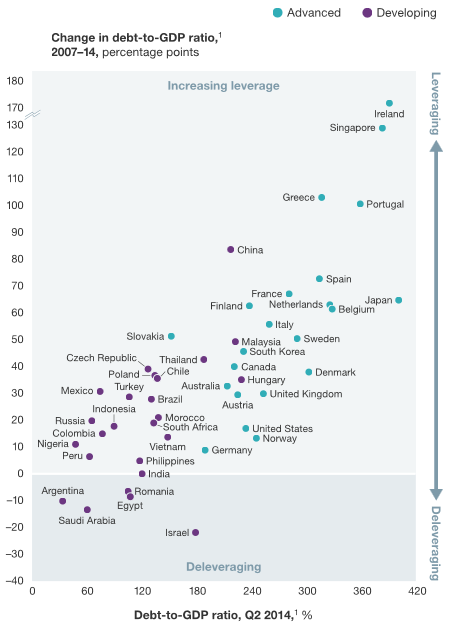

Seven years after the bursting of a global credit bubble resulted in the worst financial crisis since the Great Depression, debt continues to grow. In fact, rather than reducing indebtedness, or deleveraging, all major economies today have higher levels of borrowing relative to GDP than they did in 2007. Global debt in these years has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points. That poses new risks to financial stability and may undermine global economic growth.

Government Debt

Government debt is unsustainably high in some countries. Since 2007, government debt has grown by $25 trillion. It will continue to rise in many countries, given current economic fundamentals. Some of this debt, incurred with the encouragement of world leaders to finance bailouts and stimulus programs, stems from the crisis. Debt also rose as a result of the recession and the weak recovery. For six of the most highly indebted countries, starting the process of deleveraging would require implausibly large increases in real-GDP growth or extremely deep fiscal adjustments.

Household Debt

Household debt is reaching new peaks. Only in the core crisis countries—Ireland, Spain, the United Kingdom, and the United States—have households deleveraged. In many others, household debt-to-income ratios have continued to rise. They exceed the peak levels in the crisis countries before 2008 in some cases, including such advanced economies as Australia, Canada, Denmark, Sweden, and the Netherlands, as well as Malaysia, South Korea, and Thailand. These countries want to avoid property-related debt crises like those of 2008.

China

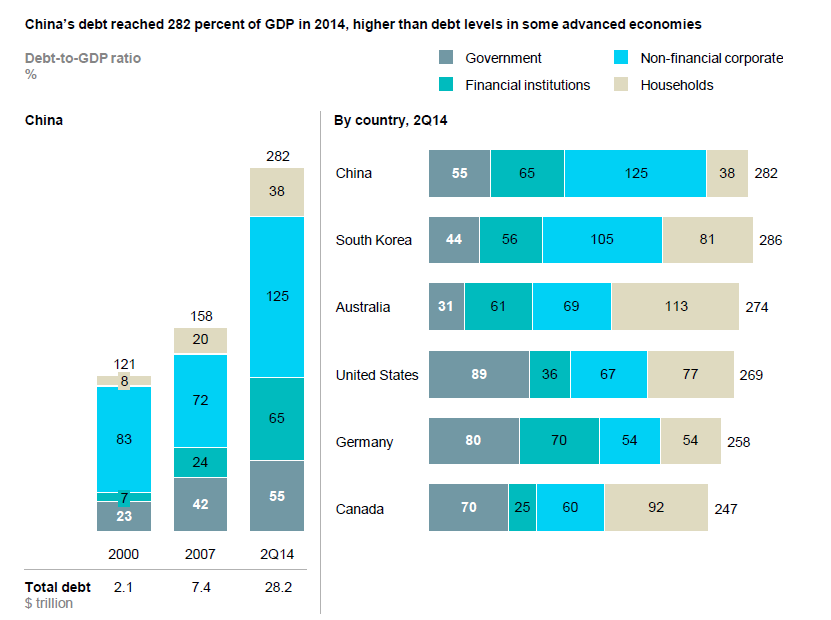

China’s debt has quadrupled since 2007. Fueled by real estate and shadow banking, China’s total debt has nearly quadrupled, rising to $28 trillion by mid-2014, from $7 trillion in 2007. At 282 percent of GDP, China’s debt as a share of GDP, while manageable, is larger than that of the United States or Germany. Three developments are potentially worrisome: half of all loans are linked, directly or indirectly, to China’s overheated real-estate market; unregulated shadow banking accounts for nearly half of new lending; and the debt of many local governments is probably unsustainable. However, MGI calculates that China’s government has the capacity to bail out the financial sector should a property-related debt crisis develop. The challenge will be to contain future debt increases and reduce the risks of such a crisis, without putting the brakes on economic growth.

…

{kind=link}