{kind=link}

Courtesy of Pam Martens.

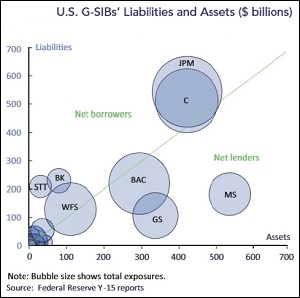

Graph from Office of Financial Research Report on Systemic Risks in U.S. Banking System (Symbols JPM and C denote JPMorgan and Citigroup, respectively.)

Last Thursday, the Office of Financial Research (OFR), part of the Federal boondoggle created under the Dodd-Frank financial reform legislation in 2010 to foster the illusion that the government was reining in risk on Wall Street, released a new study showing almost unfathomable levels of systemic and interconnected risk among the too-big-to-fail banks that cratered the U.S. financial system in 2008 and has left our economy still struggling to right itself.

Authored by Meraj Allahrakha, Paul Glasserman, and H. Peyton Young, the report reconfirms to Americans that nothing significant has been accomplished in the last six years to prevent casino capitalism on Wall Street from crashing our financial system and the U.S. economy again. The report found that five U.S. banks had high contagion index values — Citigroup, JPMorgan, Morgan Stanley, Bank of America, and Goldman Sachs.

The authors write:

“…the default of a bank with a higher connectivity index would have a greater impact on the rest of the banking system because its shortfall would spill over onto other financial institutions, creating a cascade that could lead to further defaults. High leverage, measured as the ratio of total assets to Tier 1 capital, tends to be associated with high financial connectivity and many of the largest institutions are high on both dimensions…The larger the bank, the greater the potential spillover if it defaults; the higher its leverage, the more prone it is to default under stress; and the greater its connectivity index, the greater is the share of the default that cascades onto the banking system. The product of these three factors provides an overall measure of the contagion risk that the bank poses for the financial system.”

It is noteworthy that JPMorgan, the bank that surreptitiously used hundreds of millions of dollars from its FDIC insured bank to gamble in exotic derivative trades in London in 2012 and lose at least $6.2 billion is on the above list for posing high contagion risk. It is equally noteworthy that Citigroup, the global behemoth which started this systemic train wreck in 1999 by forcing the repeal of the Glass-Steagall Act, is also on the list. Citigroup received the largest taxpayer bailout in the history of finance from 2008 through 2010: $45 billion in Troubled Asset Relief Program (TARP) funds; over $300 billion in asset guarantees; and more than $2 trillion in low cost loans.

…