{kind=link}

Courtesy of Pam Martens.

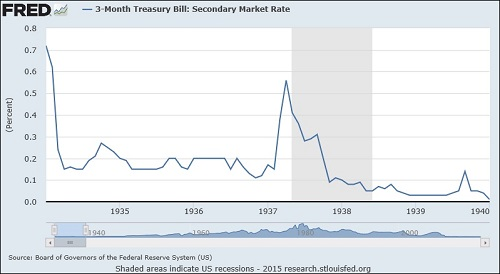

3-Month Treasury Bill Rate During Great Depression

By Pam Martens and Russ Martens: October 15, 2015

Yesterday, the U.S. Treasury auctioned one-month Treasury bills at a zero percent interest rate. By late afternoon, the bills were trading in the secondary market at a negative yield of 0.0152.

As the above chart shows, short term Treasury bill rates today are tracking a pattern similar to that of the Great Depression. That spike in the yield in the above chart in 1937 came as a result of the Federal Reserve increasing bank reserve requirements – a credit tightening – which sent the economy into a further leg of the downturn and more deflation. After the tightening in 1937, GDP fell by 10 percent and unemployment returned to 20 percent. The well known lesson of the 1937 folly is the major reason many Fed historians do not believe the Fed has any serious intention of raising its Federal Funds rate in the foreseeable future.

Instead of deliberating when to hike rates, some Fed watchers say the U.S. central bank is highly likely to be deliberating a problem known as “pushing on a string.” Here’s an easy way to get your mind around the problem. Cut off a piece of twine about 6 inches long. Place it on a hard countertop. Use your finger at one end of the string to try to push it in a northerly direction. You will observe it wiggle. You will observe it bunch up a little. But you will not see it make any material moves in a northerly direction.

Instead of deliberating when to hike rates, some Fed watchers say the U.S. central bank is highly likely to be deliberating a problem known as “pushing on a string.” Here’s an easy way to get your mind around the problem. Cut off a piece of twine about 6 inches long. Place it on a hard countertop. Use your finger at one end of the string to try to push it in a northerly direction. You will observe it wiggle. You will observe it bunch up a little. But you will not see it make any material moves in a northerly direction.

This is where the U.S. central bank, the Federal Reserve, now finds itself in terms of attempting to move the economy north, that is, out of its 2 percent or lower GDP growth since the financial crash in 2008 and 2009 and avoid outright deflation.

[my emphasis]

…