{kind=link}

Courtesy of Mish.

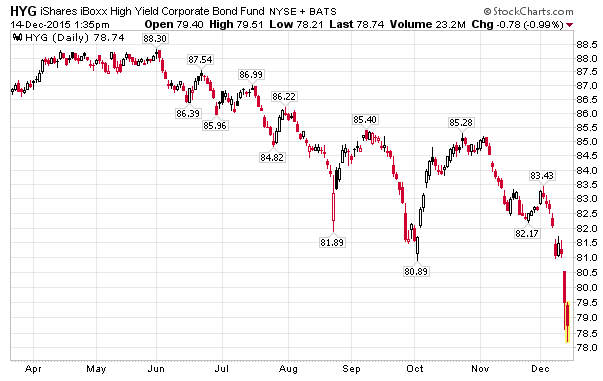

In financial markets rot starts at the periphery and spreads to the core. For weeks, rot has been visible in the junk bond market and that rot has deepened sharply recently.

JNK – Barclays High Yield ETF

HYG – iShares iBOXX High Yield Corporate Bond Fund

Liquidity Trap

A potentially destabilizing run on junk debt has weighed on the bond markets. Investors in one fund are totally locked out of redemptions. Effective yields have soared.

Please consider The Liquidity Trap That’s Spooking Bond Funds.

The debt world is haunted by a specter—of a destabilizing run on markets.

Last week, this took on more form even if there weren’t concrete signs of panic. Only one mutual fund manager, Third Avenue Management, has said it would halt redemptions to forestall having to dispose of assets in a fire sale. The rest of the industry has been quick to say that while redemptions are elevated, particularly in high-yield bond funds, there doesn’t seem to be a rush to for the exits.

Goldman Sachs, for one, put out a note Friday warning Franklin Resources “is most at risk” given the large high-yield holdings of its funds, poor performance and large outflows. On Friday, its shares fell sharply. Meanwhile, there were unusually large declines Friday in the value of exchange-traded funds that track high-yield debt.

The idea of a “run” on mutual funds might sound strange. Typically, runs are associated with highly leveraged banks engaged in maturity transformation, funding long-term loans with short-term debt. Nearly all the programs designed to avoid destabilizing runs—from deposit insurance to the Fed’s discount window to liquidity requirements—are built for banks….