{kind=link}

Courtesy of Pam Martens.

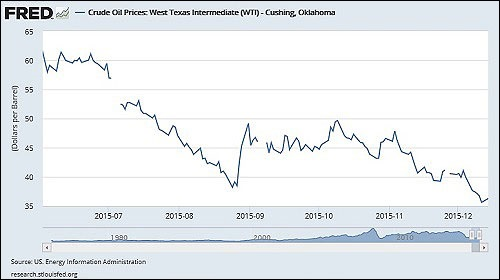

West Texas Intermediate Crude Oil Price Since June 2, 2015

By Pam Martens and Russ Martens: December 23, 2015

Exactly one year ago today, the headline story at Wall Street On Parade was titled: “Oil Crash: Don’t Believe the Happy Clatter.” We explained that there was a “mushrooming false narrative taking over the business airwaves” predicting that the rapid price decline in oil would lower gas prices at the pump, fueling a healthier consumer with more disposable income and thus a more robust economy for 2015. Our counter prediction was that the oil price collapse “will decidedly not lead to a more robust economy in the United States for very long.”

This was our reasoning at the time:

“This isn’t a little speed bump in oil prices. This is one of the most dramatic and rapid crashes in a key industrial commodity in history. Since June, the price of West Texas Intermediate (WTI), the domestic crude oil produced in the U.S., is down by 47 percent. The price of the internationally traded crude oil, Brent, is down by a similar figure.

“If this price collapse were happening in just crude oil, it could be shrugged off as a supply glut problem attributable to growing shale production in the U.S. and over production among OPEC members. But other industrial commodities are in freefall as well. Iron ore prices are down 49 percent this year while copper has declined 15 percent. The price of natural gas is down 30 percent in just the past month, including a plunge of 9 percent just yesterday.

…