{kind=link}

Courtesy of Pam Martens

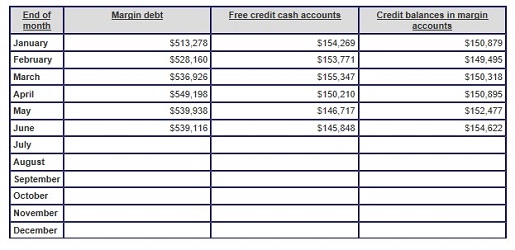

Margin Debt 2017 (Figures in millions of dollars; source, New York Stock Exchange)

By Pam Martens and Russ Martens: August 14, 2017

According to the latest data from the New York Stock Exchange, margin debt has hit new peaks four times this year, starting with a new record of $513 billion in January; $528 billion in February; $536.9 billion in March; and reaching a whopping $549 billion in April. The most recent reading for June shows a decline to $539 billion – but that is still an increase of 64 percent from the margin level of January 2008, the year of the epic financial crash on Wall Street.

Spiraling margin debt, where investors pledge securities at their brokerage firm to obtain a loan, typically to buy more securities, is frequently associated with stock market crashes. The dot.com bust followed a margin buying binge in 1999 and early 2000. Margin debt exploded from $153 billion in January 1999 to $278.5 billion by March of 2000, according to data from the New York Stock Exchange archives.

Loans using securities as collateral may be even more dangerous this time around. According to an enforcement action filed by the Massachusetts Securities Division on October 3, 2016, brokerage firms may be pushing securities based loans on their clients for purposes of mortgage funding, tax liabilities, weddings, and graduations. The enforcement action was brought against Morgan Stanley, the behemoth brokerage firm that gobbled up Smith Barney brokers, but the charges include an interesting statement from a former Morgan Stanley broker that suggests that another giant brokerage firm, Merrill Lynch, is offering similar loans. The statement from the broker reads:

“Morgan Stanley told our office during the end of February [2015] and beginning of March to pitch this product to all its customers. Management said they were doing this to keep up with its major competitor, Merrill Lynch, who was already offering express credit lines. They told us that there was big money to be made by having our customers take out credit since the variable interest rate was profitable to the company and they could just sell out of the customers positions if the customer failed to make the payment. They told us to call our customers to tell them that they could use the credit line to buy a house, pay for a home improvement project, buy a car and/or pay for school, etc. They asked us regularly how many people we had put in these products and used measurement tools to compare us amongst our peers. I did not feel comfortable recommending every customer establish a credit line because I felt that my role as a Financial Advisor and Fiduciary was to help customers save and make money and not go into bad debt.”

…