{kind=link}

Wages.

Wages.

That's what it's all about today as we get the Non-Farm Payroll Report at 8:30 this morning. Average Hourly Wages have been on a 2.7% growth path for the year and it would be surprising then, if we are below 0.2% or above 0.3%, which is the Fed's sweet spot. The closer we are to 0.3%, the more likely the Fed is to hit the brakes before rising wages push inflation out of control (and eat into Corporate Profits – which we really can't have in this country!). The Dollar has been flirting with the 95 line and more wages means more demand for Dollars to pay people with but the Dollar over 95 can put downward pressure on the indexes, as well as commodities.

The best short on a strong Dollar this morning would be oil (/CL) at $69, with tight stops above and we don't want to be greedy into the weekend but every 0.25 drop pays $250 so we can make some quick Egg McMuffin money on Dollar strenght. If there are more than 250,000 jobs created (doubtful), that would be a plus for oil as more jobs, in theory, means more people driving and more factories using oil for whatever (trucks too) – so watch out for that.

On a stronger Dollar, Silver (/SI) makes a good short as it tests the $15.50 line. We have been long on /SI but it popped nicely so now we take that profit off the table as we expect a pullback – even if it is on a run above the line (where we stop the shorts out over).

These are simple, mechanical moves you can make on events where the Dollar is in play and no event is bigger than Non-Farm Payrolls – other than a Fed meeting and this week's was a big nothing – so we have to have a little fun before the week is out!

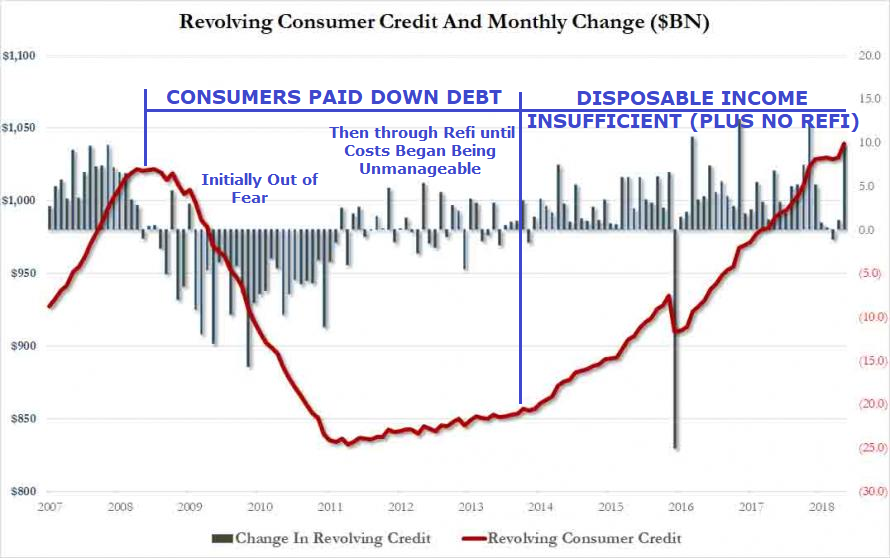

Despite rising wages, Consumer Credit has been rising at an alarming rate and that's something we'll pay attention to in next week's report as, last month, Consumer Credit jumped $24.5Bn, which is a pace to put Americans $300Bn more in debt for the year, a 7.5% gain to the $3.7 TRILLION mark. That's really not a good statistic when interest rates are set to rise (about 1/3 is revolving, credit-card debt that rises quickly).

Consumer Debt matters along with wages because, when debt rises faster than wages, Consumers eventually run out of money and are forced to stop borrowing and then the whole house of cards comes tumbling down and, as you can see from this chart, we're well past the peak we hit in 2008 but we only had 140M people working and now we are at 162M so that's up 22M jobs (15%) so, if we topped out at $1Tn in 2008, we should be able to hit $1.15Tn now – before the economy collapses and we're only at $1.1Tn so – PARTY ON!

Consumer Debt matters along with wages because, when debt rises faster than wages, Consumers eventually run out of money and are forced to stop borrowing and then the whole house of cards comes tumbling down and, as you can see from this chart, we're well past the peak we hit in 2008 but we only had 140M people working and now we are at 162M so that's up 22M jobs (15%) so, if we topped out at $1Tn in 2008, we should be able to hit $1.15Tn now – before the economy collapses and we're only at $1.1Tn so – PARTY ON!

8:30 Update: Oops, payrolls came in a bit shy at 170,000 and that's not good since we had 325,740,830 people in the US last July and, despite Trump's best efforts to kick them out, we have 328,273,764 as of this morning so that's 2.5M more people who need jobs, which means 200,000 jobs a month is the MINIMUM we need to have a healthy economy that keeps up with population growth. Despite all his claims of "miraculous" job growth and "best ever" well, everything – Trump has, for the past two years been anemic in actually creating jobs only managing to get over 200,000 on 7 out of 18 reports (39%) and they were not enough to make up for a couple of horrific misses, so the average is just 176,000 jobs per month – a net LOSS of employment to population for the President:

Meanwhile, wages are still rising on the high end (0.3%) and that means employers are not hiring but paying 2.7% more for the same jobs they were filling last year. That would be squeezing margins but, fortunately, you can't tell because it's offset by Trump's $3Tn in Tax Cuts to our Top 1% Individual and Corporate Masters. I think, when they passed the bill, they said something about it leading to more job creation but maybe they meant in the afterlife because it's been a year and June was worse than last June and July was worse than last July and this trend is not our friend…

So no go on oil – it did dip to our $250 but that's all we're going to get out of that as the Dollar is heading lower (94.84) and /SI is right at $15.49 so no short there either but Gold (/YG) is still down at $1,224 so that's a good long if /SI does pop $15.50. As to the indexes, we expect a bit of a pullback today as there's nothing exciting in the US economy and AAPL is likely to pull back a bit from the $1 TRILLION mark and 7,400 is ridiculous on the Nasdaq 100 (/NQ) – especially when you have signs of the economy slowing down.

So no go on oil – it did dip to our $250 but that's all we're going to get out of that as the Dollar is heading lower (94.84) and /SI is right at $15.49 so no short there either but Gold (/YG) is still down at $1,224 so that's a good long if /SI does pop $15.50. As to the indexes, we expect a bit of a pullback today as there's nothing exciting in the US economy and AAPL is likely to pull back a bit from the $1 TRILLION mark and 7,400 is ridiculous on the Nasdaq 100 (/NQ) – especially when you have signs of the economy slowing down.

We've done very well shorting the Dow (/YM) at the 25,300 mark, so why stop now? Tight stops above, of course, but the potential rewards far outweigh the risks on that one as does 2,830 on the S&P (/ES) and 1,685 on the Russell (/RTY).

The indexes are at record highs but the economy is struggling and, in case you forgot, we're in the middle of an escalating Trade War with the World's 2nd largest economy – might be a good idea to be a bit more cautious, right?

Have a great weekend,

– Phil