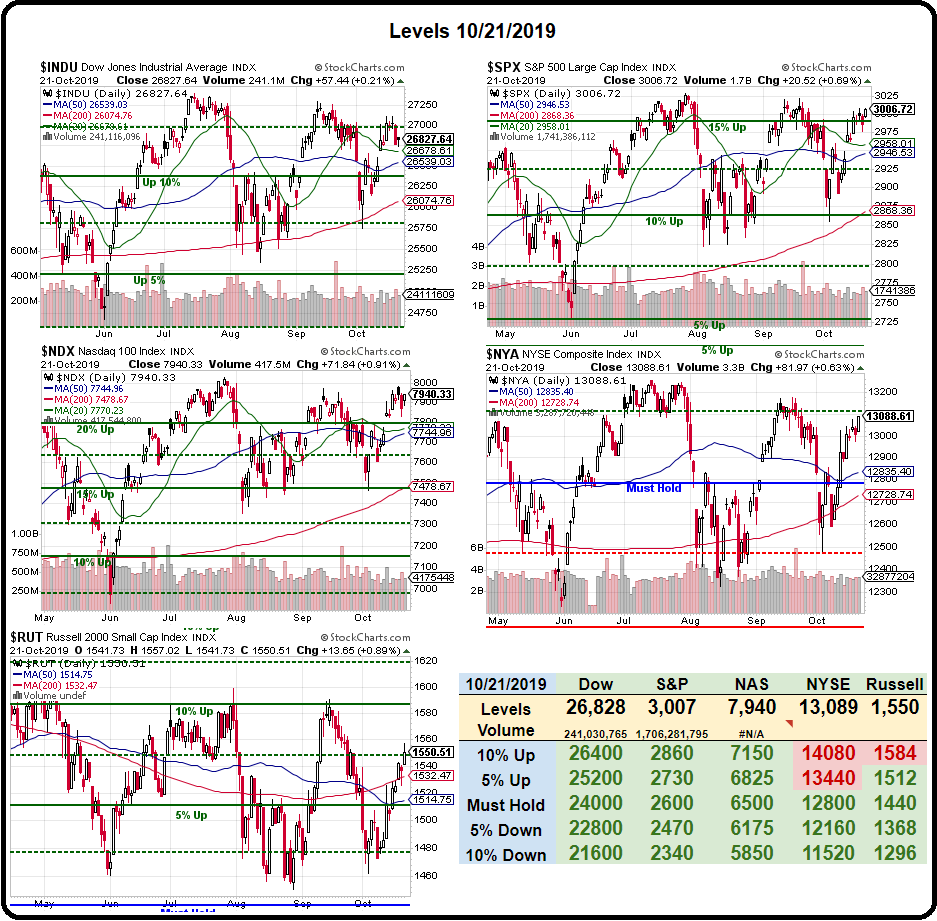

{kind=link}

Can things get worse for Boeing (BA)?

Since Thursday's close, BA has dropped $40, from $370 to $330 and that's 10.8% in two sessions so we'll watch the $333 line (10%) to see if they can getg back over that and then we'd look for a weak bounce at $340 and a strong at $348 but the news on BA has been very, very bad with two downgrades yesterday as rumors came out that BA had lied to regulators – leading to hundreds of deaths.

BA booked a $5.6Bn charge in Q2 and estimated the 737 Max grounding would cost them $8Bn overall but that was before the new revelations. BA makes $10Bn a year, usually, but lost $3Bn last quarter and they will report again tomorrow – so get ready for some fireworks. It's very unlikely we'll hear that "all is well" tomorrow and it's too risky to play short puts in this environment but, we can still play for an eventual recovery with a Bull Call Options Spread as the first trade in our new Earnings Portfolio:

- Buy 5 BA 2022 $300 calls for $72.50 ($36,250)

- Sell 5 BA 2022 $350 calls for $50 ($25,000)

That's net $11,250 on the $25,000 spread that is currently over $15,000 in the money so, if BA gets back over $350 by Jan, 2022, you will make $13,750 (122%), which is not bad money for 2 years. If BA is flat or goes lower, we can begin to recoup our money by selling short calls, like the Jan $330 calls, which are $20. Just selling 1 contract for those puts $2,000 in our pocket and we have 8 quarters to sell so it's very possible we can generate $16,000 worth of income while waiting for our $13,750 pay-off!

We decided to make a new $100,000 Earnings Portfolio, mostly for quick trades duing the season as we are mainly in cash and have plenty to play with. Yesterday, in our Live Member Chat Room, I suggested the following trade on TD Ameritrade (AMTD):

Let's make an Earnings Portfolio with $100,000 to do some earnings plays while we wait for a good time to start rebuilding the main portfolios. For AMTD, we can:

- Sell 5 AMTD 2022 $30 puts for $4.20 ($2,100)

- Buy 10 AMTD Jan $38 calls for $2.30 ($2,300)

- Sell 5 AMTD 2021 $45 calls for $2.60 ($2,600)

That's a net credit of $1,800 on a $7,000 spread where we are disadvantaged by time but not really as an up move or flat would let us cash out Jan and then pick up a 2022 bullish spread to cover the short 2021 $45 calls and a down move would give us a better entry on a 2022 spread and we could roll and DD on the short puts and sell more calls.

Earnings went well last night and the stock should be up a bit this morning and we'll see how it goes but the suggestion came in too close to the closing bell for us to be able to include it in the portfolio, unfortunately so BA will be our first official trade idea to be included. Still, it will be interesting to see how this one pans out.