{kind=link}

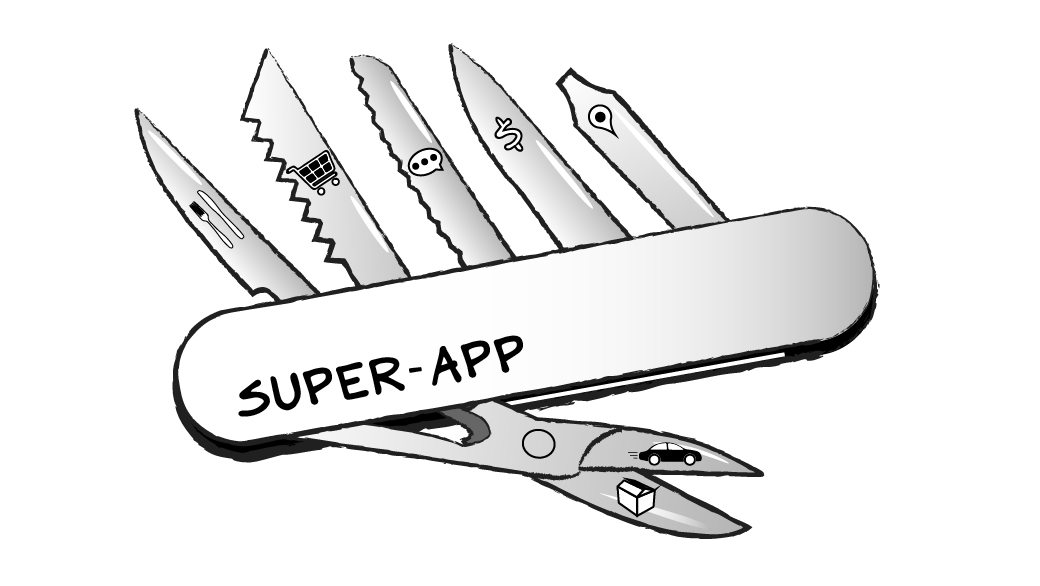

Super-App

Courtesy of Scott Galloway, No Mercy/No Malice, @profgalloway

Two years ago I wrote a letter to the chairman of Twitter calling for Jack Dorsey to be replaced as CEO. Or, more to the point, for the board to appoint a full-time CEO. An executive who spends 90% of his time running another company and plans to spend half the year on a different continent looked like a recipe for poor shareholder returns. Spoiler alert: It was.

This past February, as there were now directors on the board acting as fiduciaries, I predicted Dorsey would be replaced by the end of the year.

Between the day @jack reclaimed the CEO position and the day he resigned (six years), Twitter’s stock increased 33%. The S&P 500, Facebook, and Google rose by 121%, 283%, and 447%, respectively.

My next prediction? Twitter will be acquired by the end of 2022, most likely by Salesforce or a fintech company like PayPal or Stripe with inflated currency. Jack could also reunite his sister-wives — in a man-bites-dog scenario, the company formerly known as Square could acquire Twitter. Why? For the same reason it’s now called Block. Super-apps.

A super-app offers a suite of internet services on one platform. Block already boasts an armament of super-app services: peer-to-peer payments (CashApp), crypto and stock trading (also CashApp), lending (Afterpay), music streaming (Tidal), it’s dabbled in food delivery (Caviar, sold to DoorDash in 2019), and its core merchant-payment platform (Square). Building social into the platform is the logical next step to becoming America’s first super-app.

I wrote about super-apps last week in New York magazine, and excerpts from that article appear below. It was timely: Super-app stories have been in the news ever since.

- Square changed its name to Block — this was announced 48 hours after Dorsey exited Twitter. “Square” will be reserved for the merchant-payment business; the three-dimensional moniker encapsulates all its various products. Twitter would give Block even more dimension.

- ByteDance (TikTok’s parent company) invested in iMile, a last-mile courier service that connects mostly Chinese e-commerce companies to consumers in the Middle East. Dance videos are just the bait — commerce is the hook, and ByteDance is building services for more than limber-limbed teens.

- Grab, the “everyday everything app” from Singapore, made its public debut yesterday after a $40 billion SPAC deal. It’s the biggest SPAC to date, though the stock fell more than 20% by the closing bell.

- Indian super-app Paytm IPO’d with a $20 billion valuation — the largest public listing in the nation’s history. However, however … it, too, shed more than a fifth of its value on the first day of trading. Then slid further before maybe finding solid ground at $14 billion.

In sum, it’s getting crowded in the super-app lobby. The competition in India now includes: Amazon Pay, Google Pay, WeChat, and PhonePe (owned by Flipkart/Walmart). Southeast Asia also hosts many players: Gojek, Line, Sea Limited, Tokopedia, Zalo, and more.

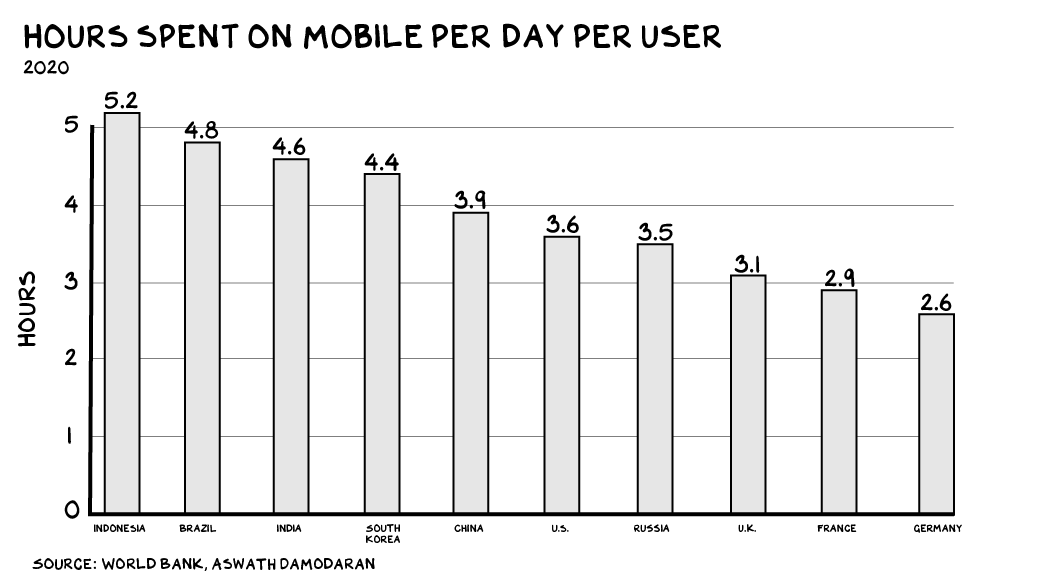

And for good reason. The super-app market is the digital Iron Throne. Super-apps live on mobile, and mobile is the internet in emerging markets. India, for example, has three times as many cellular subscribers as the U.S., and Indians spend 17% more time per day on their phones.

Long term, however, it’s the world’s largest economy that is the biggest prize. A platform that services every aspect of the consumer experience in any market will be one of the most valuable companies in that market. The firm that establishes super-app leadership in America will be the most valuable company in history. Some thoughts below, with excerpts from our piece originally published in New York magazine on November 24, 2021.

The metaverse is best described as a consensual hallucination between Mark Zuckerberg and the media — a fantasy that we’ll trade pleasurable activities in the physical world, like cooking and dating, for nausea-inducing hours in a virtual realm full of legless avatars. To most ordinary people, the Facebook CEO’s aspiration to be the god of a universe we can enter only by affixing a prophylactic to our heads seems megalomaniacal. They’re correct. However, every time you hear Zuckerberg say metaverse, swap in super-app and the plan sounds less stupid.

A super-app is a single mobile app that offers basic services including chat and payments, along with a suite of “mini-apps” from third parties, ranging from stores and restaurants to government agencies. Westerners aren’t familiar with them, but across much of Asia, super-apps are the internet. The largest is China’s WeChat, possibly the most used piece of software on the planet. On WeChat, you can find a date, hail a cab, pay utilities, even get divorced. An app reaches super status when it knits together a critical mass of services, makes them so easy to toggle across that, even if they aren’t as good as sole-purpose apps, the app becomes your OS for your digital life. The more services, the less reason to ever leave.

A super-app can start small: WeChat began in chat; Indonesia’s Gojek started in ride hailing; and in India, Paytm was originally for buying prepaid mobile minutes. All eventually expanded from their niche and snowballed to dominance. The economics of super-apps are powerful — and possibly inexorable. I’m convinced that constructing a U.S. super-app is the strategic-imperative of the next decade and could result in the first $5 trillion company.

Already, there are a host of companies looking to replicate the Asian model — but to do so, they’ll have to get past Apple and Google, the nearly hegemonic mobile-OS providers, which are investing billions to prevent a super-app from inserting itself between consumers and the OS. The radical transformation of Apple under Tim Cook has been a decade-long project to extend the company’s ecosystem to nullify the potential for a super-app to sit on top of iOS. It explains why Apple now offers both credit and debit payment systems, why you can use your Apple ID to sign in to a huge range of third-party services, and why Cook is giving Reese Witherspoon and Jennifer Aniston hundreds of millions of dollars to produce an inferior version of Murphy Brown.

??Who are the strongest challengers to Apple and Google? Most apparent, the other Big Tech behemoths, Amazon and Facebook/Meta, who aim to leapfrog by building alternative interaction paradigms, a pretentious way to say “voice” (Amazon) and “VR” (Meta). And while they are both trying to skate to where the puck is headed, Meta is on thin ice with a portal that makes you nauseous. Voice is underhyped, and VR overhyped.

The likely epicenter for aspiring super-apps is fintech. Payments in particular: PayPal, which owns Venmo, and Block né Square. And new fintech unicorns are being birthed weekly, including crypto-based businesses that are also in a position to leapfrog with long legs of capital, vaulting over the entire existing financial system. Fintech companies that reach scale have valuable infrastructure, acquisition currency in the form of overheated stock, and trust. Traditional Big Tech leaders, social media companies especially, have burned through acres of PR heat shields over the past years, relentlessly assaulted by bad press as they ask people to come for teen depression and stay for insurrection. Fintech has been (relatively) unscathed. Plus, these companies begin their assault from higher ground: payments.

Payment processing is the foundation of a super-app. It’s the glue that integrates core features with those provided by third parties on the platform, and it gives users the convenience of not needing to enter credit-card information across apps and sites. A shift in the arbitrage of attention, from ads to the more potent payments business, promises to fuel a historic merger-and-acquisition binge that will reshape the array of industries that tech derisively labels “content.” The likely biggest acquirers will be in finance — not just start-ups but Wall Street’s Old Guard, whose imminent panic will manifest in M&A banker fees.

Financial-services firms are already expanding into new markets. Not long ago, American Express acquired the reservation service Resy. There was a brand logic to that deal, as AmEx has long offered concierge services. In addition, JPMorgan recently purchased the Infatuation, the restaurant-review site and owner of Zagat, which is considerably more curious. In March, Square paid nearly $300 million for the music streamer Tidal, prompting a wave of WTF? coverage. You’ll know the super-app conquest has hit another level when Jack Dorsey combines Square with the other company he used to stop by on Wednesday and Friday afternoons, Twitter, and offers useful services.

I’ve lived through half a dozen of these techno-social transitions, from the PC era to “dot-coms” (ask your parents), through mobile and social, and now this. Every shift has created more wealth than the one before — but also levied more harm. One thing they all had in common is that we never really saw them coming. In hindsight, these things look obvious, but none of these transitions have manifested as we expected. For the most part, they’re worse. The difference now is that we can see super-apps coming. In Asia, they’re already here. As consumers, investors, and political leaders, we have a chance to do better. To set the stage for competition and empowerment, not co-option and enragement. Whether our future is mediated by Siri, Alexa or by Meta, it doesn’t need to be a world of addiction and exploitation. The virtual world isn’t “it is what it is,” but what we make of it.

Life is so rich,

P.S. Making predictions can be dangerous. It might put you in the Twitter crosshairs of Elon Musk. Yet I persist. Join my free Predictions livestream on December 7. You probably won’t regret it.