The Last Last Mile

Courtesy of Scott Galloway, No Mercy/No Malice, @profgallowa

On Black Friday, we wrote about the dangers of the Buy Now Pay Later industry, which takes advantage of our psychological makeup to trick us into spending more than we can afford. From our lips to Uncle Sam’s ears: Yesterday, the Consumer Financial Protection Bureau announced it is collecting “information on the risks and benefits of these fast-growing loans” from five leading BNPL companies. It’s not (yet) the breakup of Big Tech, but it’s something.

OK, enough told-you-so. On to the post.

As I age (happening more and more recently) it feels as if the call from the Old World grows louder. We’re in the U.K. checking out boarding schools for my oldest (I’m a wreck over this) and telling my boys stories of their grandparents and the war. My mom and dad were born and raised in London and Glasgow, respectively. It’s the perfect vacation: We’ve watched 1917, Dunkirk, and the Blues (Chelsea Football Club) draw with the Toffees (Everton). Tomorrow we’ll see Tottenham face off against Liverpool. I love it here and want our soon-to-be teenage boys to be somewhere besides Florida for a few years. But that’s another post.

As I age (happening more and more recently) it feels as if the call from the Old World grows louder. We’re in the U.K. checking out boarding schools for my oldest (I’m a wreck over this) and telling my boys stories of their grandparents and the war. My mom and dad were born and raised in London and Glasgow, respectively. It’s the perfect vacation: We’ve watched 1917, Dunkirk, and the Blues (Chelsea Football Club) draw with the Toffees (Everton). Tomorrow we’ll see Tottenham face off against Liverpool. I love it here and want our soon-to-be teenage boys to be somewhere besides Florida for a few years. But that’s another post.

The U.K. is responsible for some of the world’s greatest innovations, including chocolate bars, the hovercraft, Adele, and … next-day delivery. Not Jeff Bezos, but a 19th-century Welsh flannel-maker. In 1861, Pryce Pryce-Jones (great name) began accepting mail-in orders for his flannels and promising next-day delivery nationwide. By 1880 he had more than 100,000 customers. One of them was the Queen, who later knighted him.

Sir Pryce-Jones leveraged the British railway network’s expansion and brokered a deal with the North Western Railway Company for three carriages on the Newtown-Euston line. These carts moved the flannels across the country daily. He then closed the gap between production and distribution. This meant building a warehouse next to the Newtown station. Then a factory next to the warehouse and a post office next to the factory. Pryce-Jones realized people liked his flannels but loved immediacy. Speed was the differentiator.

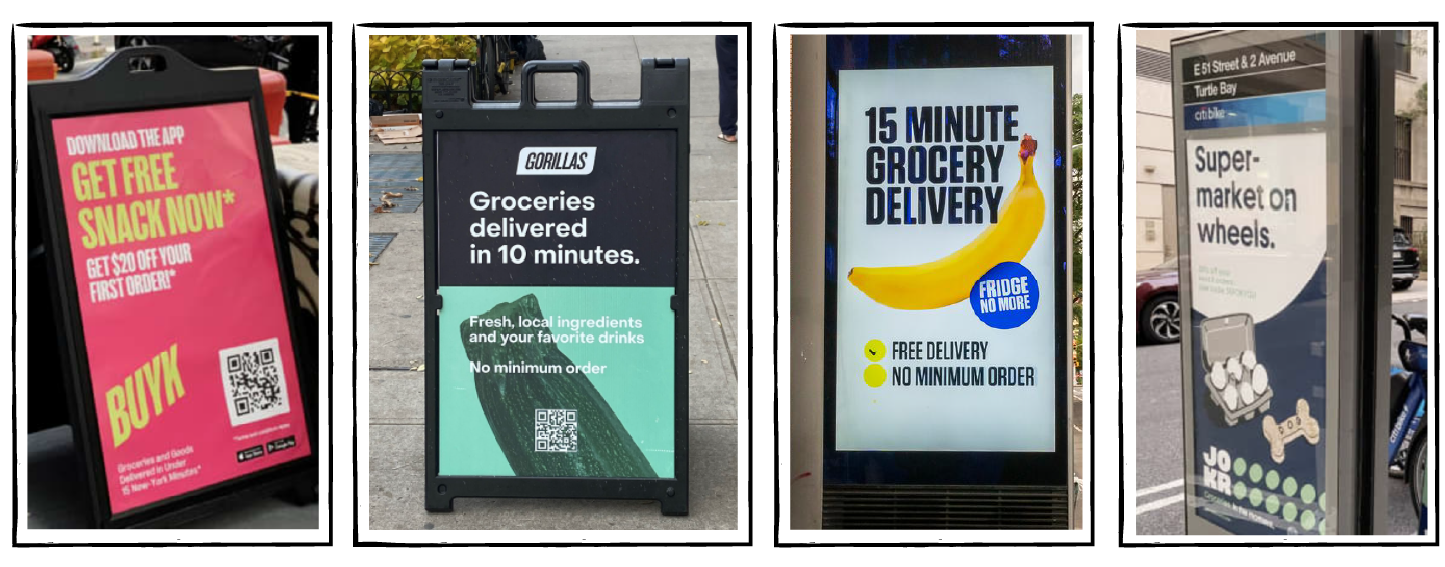

A century and a half later, Pryce’s impact has manifested in Jokr, Buyk, Gorillas, and Fridge No More. These firms were all birthed during the pandemic and may be points in a line of the prosperity often registered post-crisis. New York City has become a petri dish for dozens of budding delivery startups. They’re recrafting the supply chain with hundreds of millions in venture capital to achieve (roughly) the same thing:

Get you your shit fast, really fast.

{kind=link}

The Need for Speed

These companies erect hyperlocal grocery stores — “dark stores” — that are only open to employees. Each hub serves an area no greater than a mile in radius. Once your order is processed, pickers collect and package your groceries in 3 minutes and a courier e-pedals them to your doorstep within the next 12.

The final step in delivery, handing a product to the consumer, is known as the last mile. Historically, the mile has been rhetorical. The nearest UPS hub or DHL warehouse might be 10 or 20 miles. These businesses, however, have dispersed their distribution networks to within an actual mile. The last last mile.

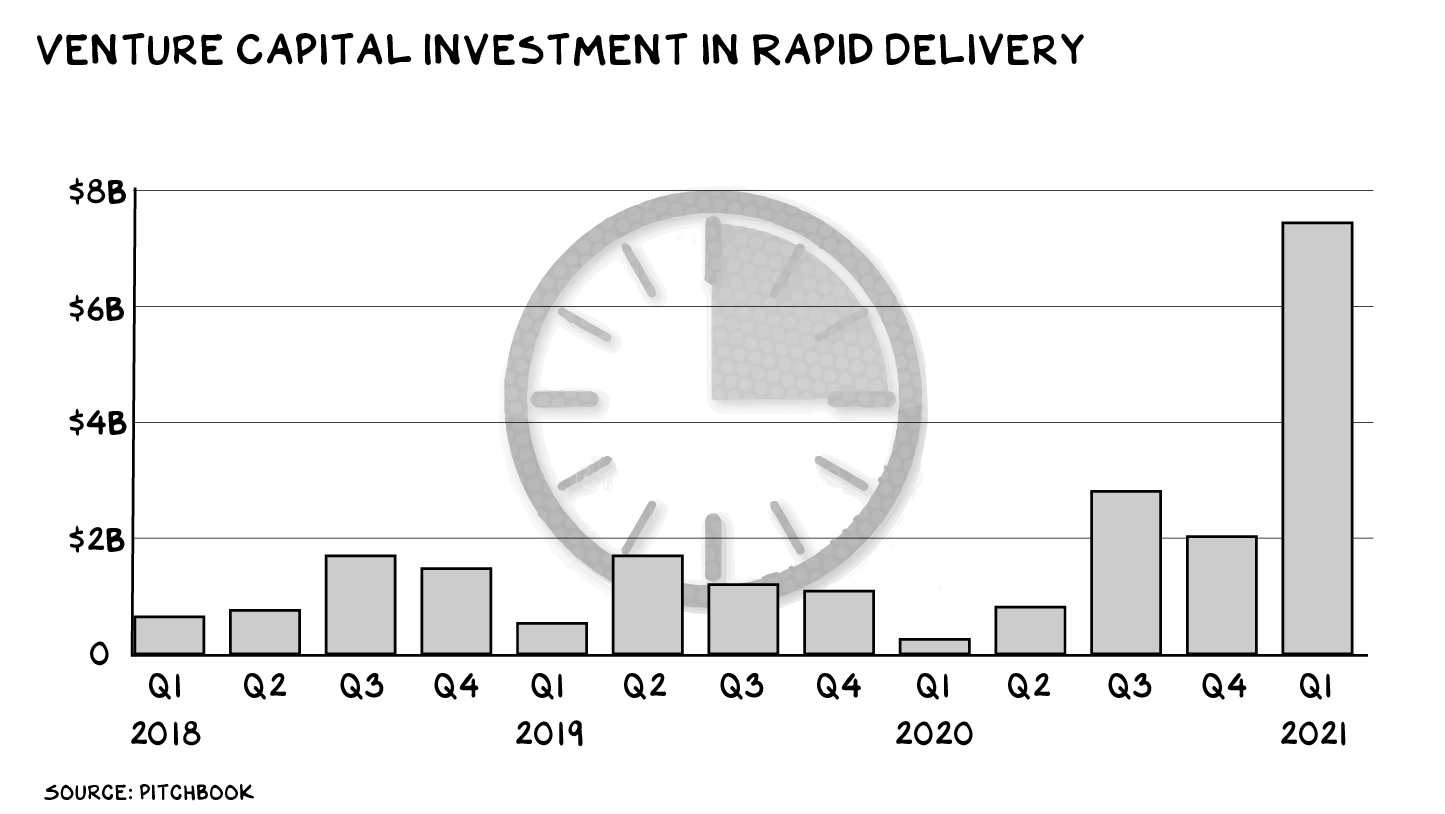

VCs recognize the opportunity. Gorillas has raised more than $300 million since its founding last year and is valued at over $1 billion. Jokr, which started delivering groceries eight months ago, has raised $350 million at a $1.2 billion valuation. They’re two of the fastest zero-to-unicorn firms in history.

It’s a global phenomenon. Spain’s Glovo raised $528 million in April ($2 billion valuation). Turkey’s Getir raised $550 million in June ($7.5 billion valuation). America’s Gopuff raised $1 billion in July ($15 billion valuation). Prague has Rohlik, London has Zapp, Moscow has Samokat … the list goes on. In the first quarter of this year alone, instant-delivery startups raised nearly $8 billion — more than in all of 2020.

Delivering at these speeds is similar to supersonic travel: expensive. It means operating hundreds of distribution hubs and hiring thousands of full-time couriers. (To get the reliability they require, these companies put their delivery staff on salary, in contrast to Uber’s gig-economy model.) That’s on top of enormous marketing budgets. Buyk will spend a fifth of its new capital on marketing this year. Jokr lost $13.6 million on just $1.7 million in revenue. You read that right — it had losses equal to eight times its revenue.

Déjà Vu

In 1999, Webvan went public at an $8 billion valuation (a big number back then). The company promised grocery delivery to your doorstep in 30 minutes thanks to state-of-the-art fulfillment centers manned by robots. At its peak in 2000, Webvan was registering $180 million per year. Unfortunately, the cost of processing, fulfilling, and delivery was … half a billion dollars. Delivery in 30 minutes is compelling. But the concept was ahead of its time, and though capital was cheap, it was expensive vs. today. Webvan filed for bankruptcy within two years of listing.

While we’re strolling down memory lane, Kozmo.com raised $250 million in 1999, promising free one-hour delivery for small items like DVDs, magazines, snacks, and coffee. It made $3.5 million in revenue that year, but lost $26 million and went bust in 2001. Urban Fetch (a Kozmo rip-off) was another: It raised some cash in 1999, burned it all, and shut down in 2000. At the San Francisco office of my consulting firm, employees would order a pint of Ben & Jerry’s or a pack of gum from Kozmo rather than walk to the convenience store. Again, the value proposition was there, just not the capital to achieve requisite scale.

Arrival

Bezos felt speed could be the skeletal structure of a megalodon. In 1999 getting everything you wanted within a day of ordering was expensive. And with only a third of Americans using the internet, the customer base was sub-scale. Books were the placeholder. The real product, speed, would take decades and tens of billions of dollars to develop.

At the time, shipping costs at “catalog” companies such as Williams Sonoma were steep: 30% or more of the product price in some cases, just for “regular” delivery, which might take several days. Two-thirds of larger retailers made a profit on shipping, but retailers relied on third-party providers (UPS, FedEx, and the postal service), marking an era of great brands with little underlying product differentiation — FedEx didn’t offer The Marvelous Mrs. Maisel.

Amazon.com began the same way. In 2004 it charged $9.48 for two-day shipping on a book and $16.48 for overnight. Bezos envisioned another way — the way of Pryce-Jones. Both men understood speed was a differentiator worthy of investment. The next year, he turned unlimited two-day shipping into the core feature of the most accretive innovation in business history: Amazon Prime.

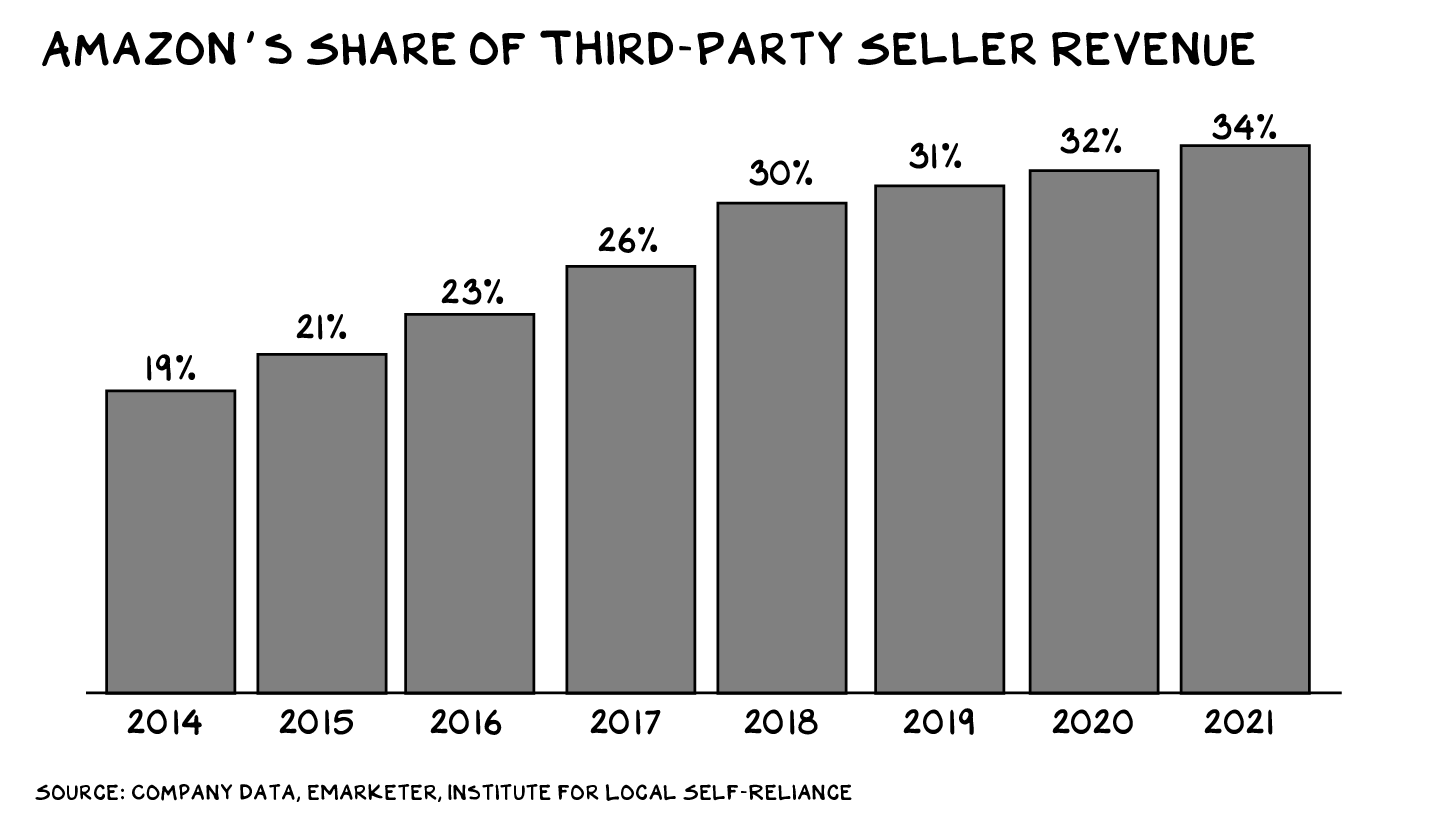

After achieving a monopoly on speed, Amazon began turning it into a profit center and became a platform for other retailers, charging them for its best-in-class fulfillment. Then, once Amazon got these third-party sellers on the platform, Bezos started extracting more from every sale. In 2014, Amazon took 19% of third-party seller revenue. Today it takes 34%. That number’s mostly a mix of the company’s referral fees (what you pay to be on the platform) and fulfillment fees (what you pay for your product to be delivered). An increasing share is now coming from advertising fees — and the rent for visibility on Amazon is rising. People posit the economic value of beachfront real estate in a/the metaverse. It already exists. It’s the results page in the online retailer’s metaverse that retailers are paying for, and it’s likely worth tens (if not hundreds) of billions.

Amazon’s toll road on third parties generated $90 billion in revenue last year — if it were a stand-alone business, it would rank 31st on the Fortune 500. This year, it’s projected to clock $120 billion, ahead of both FedEx and UPS.

Watch Your Back

Some instant-delivery companies say they’re competing with supermarkets. Jokr’s co-founder says he’s coming after Amazon. That might sound crazy, but when your valuation is 706 times your revenue … you need to articulate a big vision and assure investors you are hunting elephants.

The market’s growing, and so are our expectations. In 2015 most consumers defined fast shipping as three or four days. The next year, it was two days. If these companies normalize 15-minute delivery, we’ll likely develop a taste for last-last-mile flesh. And that could reshape the $1 trillion grocery market.

That might be enough to scare the delivery behemoths into action. In October, Uber launched a 15-minute grocery-delivery program in Paris. Last month, DoorDash acquired Finland’s ultrafast service Wolt for $8 billion. Instacart is reportedly launching its own trial program, as is … Amazon.

This is part of a larger trend that’s bigger than just physical delivery. Everything is getting delivered. Streaming brought the box office into the home; roughly half of pre-pandemic moviegoers aren’t buying tickets. Telehealth brought doctors and therapists into the home; telehealth claims are up 37 times from before the pandemic. Yet more evidence of the Great Dispersion.

Over the past two decades, the dispersion of retail from shelves to porch fronts has created and reallocated trillions in value. A similar tectonic shift is likely to occur in grocery and restaurants at the hands of ghost kitchens, ride-hailing companies, and well-capitalized last-last-mile firms. The question is, will new giants be birthed or will the existing behemoths grow new heads?

Slow … Down

Something is lost in the rush towards the instant distribution of everything. There’s something unmistakably human about a doctor placing a hand on your shoulder when they break good or bad news, or a therapist looking you directly in the eye when you start telling them what’s on your mind, or being part of a collective when you see a bunch of old people sending young people to die (see above: 1917 and Dunkirk). We’re losing these moments by the day, minute by minute.

Yet something is gained, as well. Innovation in the last mile has likely created more shareholder value in the past two decades (e.g., Apple Stores, Amazon Prime, streaming) than any innovation in any era. Why? Because they help us make the most of our time. The same is possible in our personal lives. We, too, would benefit from an investment in going the last mile. Do we get to the love and admiration we feel? Do we tell our spouse we appreciate the life we’ve built together? Do we show our kids, every day, that they are wonderful? Do we practice citizenship, every day, in ways that supersede partisanship or empty recognition from media algorithms? Most of us feel all these things, but do we say at the same rate what we think and feel?

Take it from two of the clearest blue flame thinkers in business history, Mr. Bezos and Sir Pryce-Jones: The only real asset is time. And at the end of this sentence you’ll be closer to having … less. The unlock in many of our own lives is the last last mile.

Life is so rich,

P.S. This February in Miami, the heat is on. Kara Swisher and I debut Pivot MIA, a new type of conference that will challenge convention. Join us in America’s most vibrant and future-forward city February 14-16 as we assemble the hottest names in fintech, media, entertainment, education, climate, and more. You don’t want to miss this.

P.P.S. My goal with No Mercy / No Malice is to make you more successful, both professionally and personally. That’s also the goal of my upcoming Business Strategy Sprint with Section4, kicking off January 10. Join us.

Picture of road via Pixabay