{kind=link}

Apple: Thief

Courtesy of Scott Galloway, No Mercy/No Malice, @profgalloway

Round numbers have no inherent meaning — they’re a consequence of 10 fingers. But they provide a benchmark, a way to focus our observations. The last few years in tech, we’ve witnessed several firms breach $1 trillion market capitalizations, a few hit $2 trillion, and one touch $3 trillion.

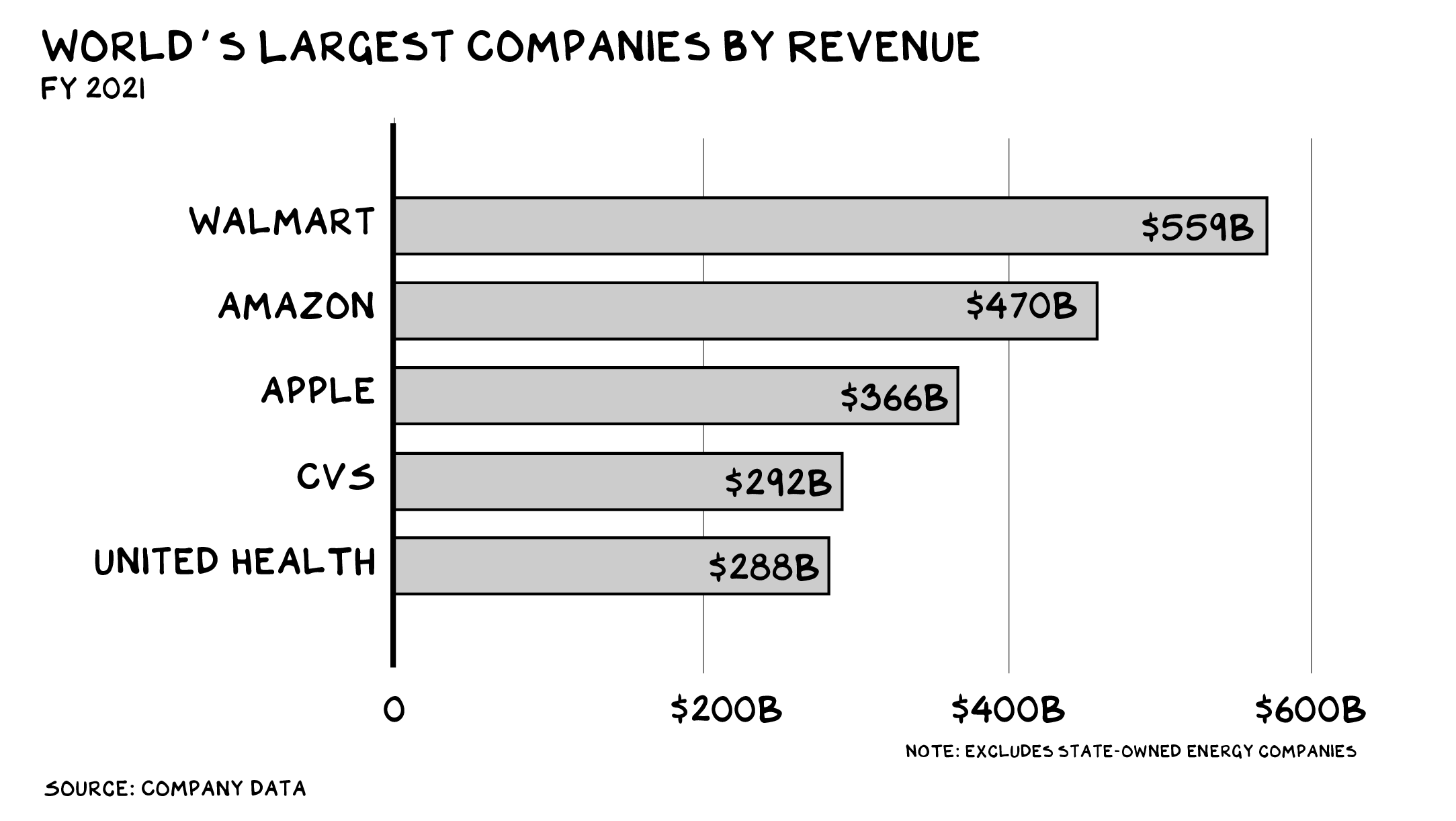

Let’s set a more audacious goal: $1 trillion in revenue. We’re still a few years away — the largest company by revenue today, Walmart, brought in $559 billion last fiscal year. And while market cap can fluctuate 20%+ in several minutes, revenue is closer to the epicenter of stakeholder value, because it benchmarks actual commerce. The English call revenue “turnover,” which conveys someone doing actual work.

The Great Heist

Revenue of $1 trillion won’t be found in a single category. Few categories even offer a $1 trillion market, and market dominance in any category comes with problems. It’s better to have a 20% share of five markets than 100% of one. Diversity offers security, and monopolies attract legal attention: Facebook and Google’s shared dominance of digital advertising makes it easier to fit them into the antitrust legal framework.

A trillion in revenue will require stealing markets from incumbents. It’s already happening in Big Tech: Amazon flew head-on into the cloud, Microsoft is eating gaming, and in the next decade we will see The Great Heist: $1 Trillion Edition. One company is best poised to ascend to the Iron Throne of theft.

Six-Shooter

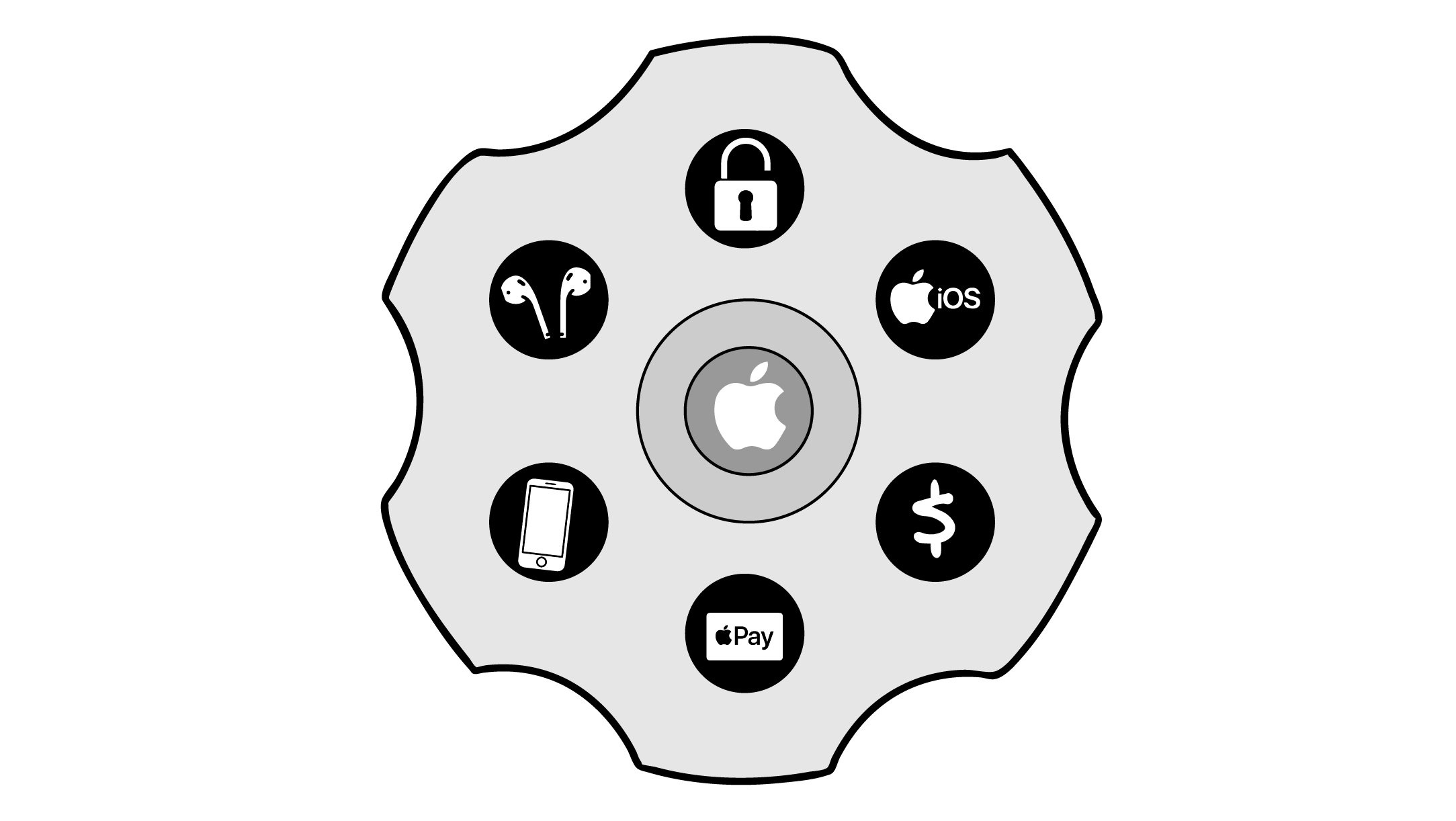

Apple’s sidearm is a thermonuclear device. Each bullet, an unmatched asset.

Familiar operating system. For the wealthiest billion people on earth, iOS is the operating system of their life. When presented with a “smart” television, home, car, or retail store, they don’t want to learn a second language.

Epicenter. The iPhone, the most successful consumer product in history, is the epicenter of tech. The phone contains speakers and microphones, a barometer, an accelerometer, a proximity sensor, an ambient light sensor, a gyroscope, and four cameras. And it connects a web of interfaced devices that meet you everywhere: living room (Apple TV), kitchen (HomePods), keys (AirTags), ears (AirPods), and wrist (Apple Watch). Nobody else has this, or any discernible path to it. The Android ecosystem is fragmented across a dozen competitors; Alexa can’t leave the house alone; and Facebook (Meta) has given up on the real world entirely.

Beachheads. Apple has established a beachhead in multiple businesses beyond its core hardware products, including payments (Apple Pay, Apple Card, Apple Cash), games (App Store, Apple Arcade), media (Apple TV+, Apple Music, Apple News), mapping (Apple Maps), cloud and email services (iCloud), and even advertising (App Store Search Ads).

Hardware expertise. As capital increasingly funneled to a monster that would eat the world (software), Apple further differentiated its hardware competence. Think about it: There are dozens of great software firms, but scant firms (i.e., one) that have dominated hardware for decades. Nobody rivals Apple’s refined hardware or ability to produce actual things on a global scale. The company shipped 236 million iPhones and 58 million iPads in 2021. That’s a stack of devices 1,400 miles high — 23 times further than Bezos’ trip to “space.”

Trust. Most battles are determined before the first shot is fired. The cache of the invading army here is trust. One of the great brand moves in history was anticipating the increasing relevance of privacy and staking huge capital and focus on it. Apple’s much vaunted iOS tracking change was a ninja move, registering damage not from sheer force, but by striking where it hurts the most. Violating privacy is central to the business model of Apple’s rivals, and thwarting that has left them befuddled.

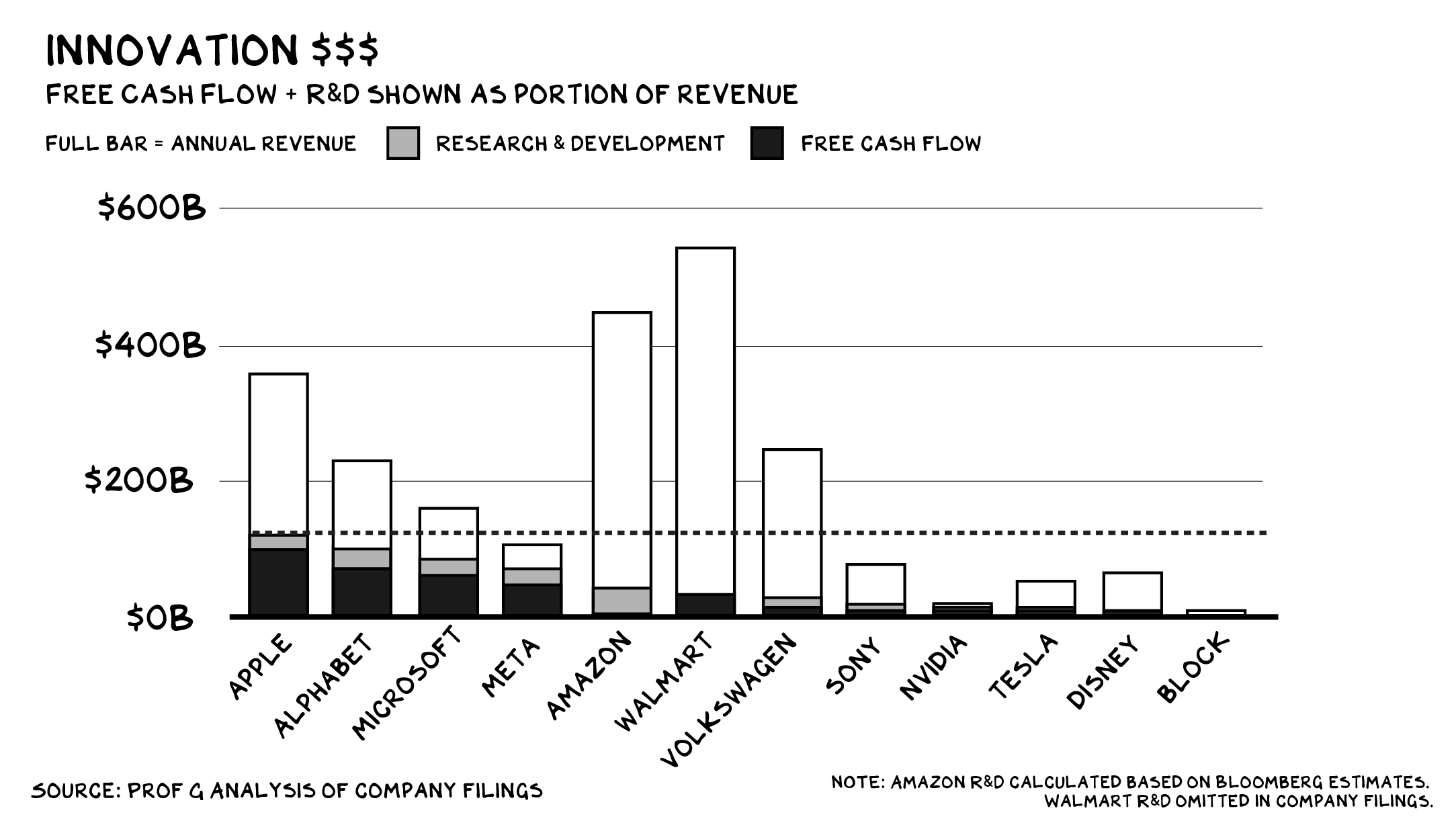

Capital. In 2021, Apple generated an astounding $93 billion in free cash flow (operating cash flow minus capital expenditures), which are funds it can allocate toward new opportunities. That’s on top of a $22 billion R&D budget. Meaning Apple has potentially $126 billion annually to invest in new battles. This number is staggering and singular.

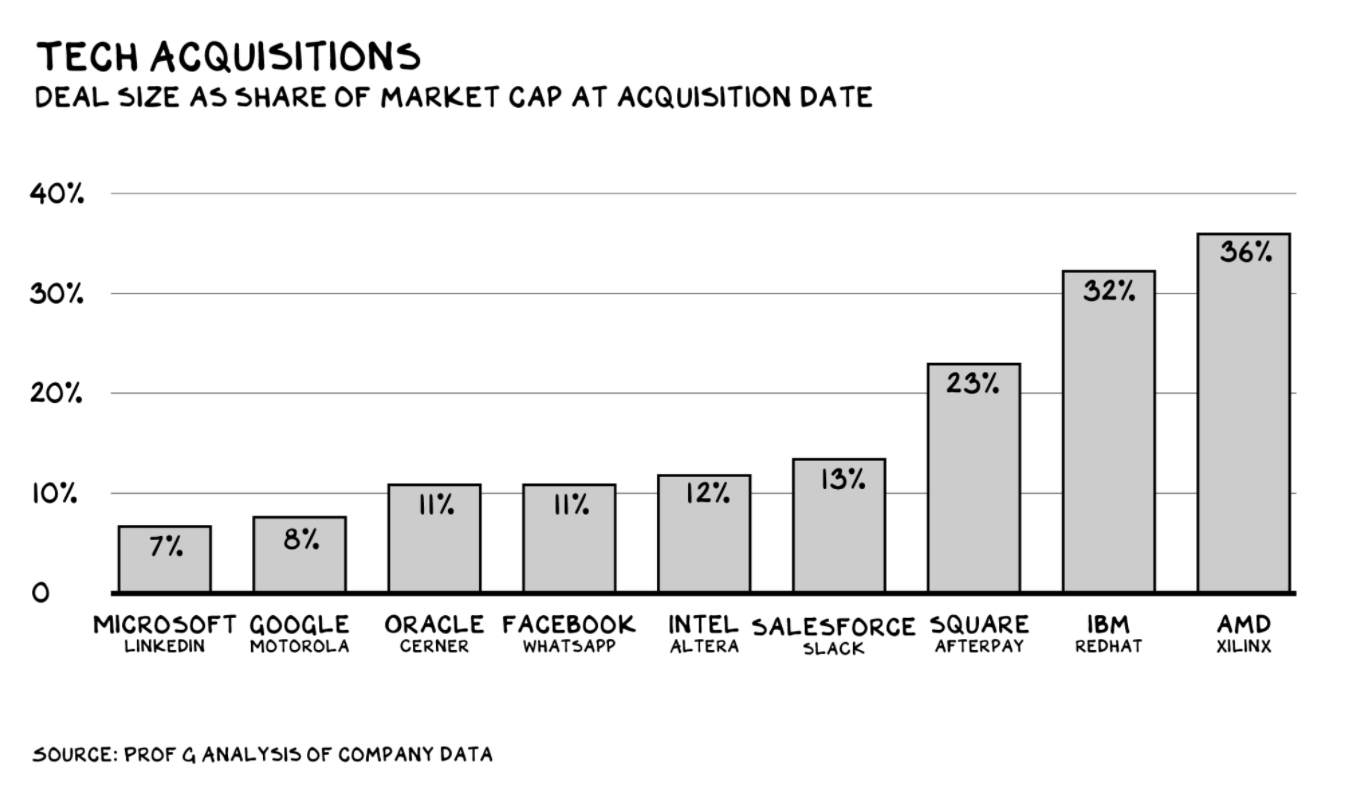

And Apple’s stock is also currency. Tech companies routinely make acquisitions equal to 10% or more of their total value. What could Apple purchase with 10% of its market cap?

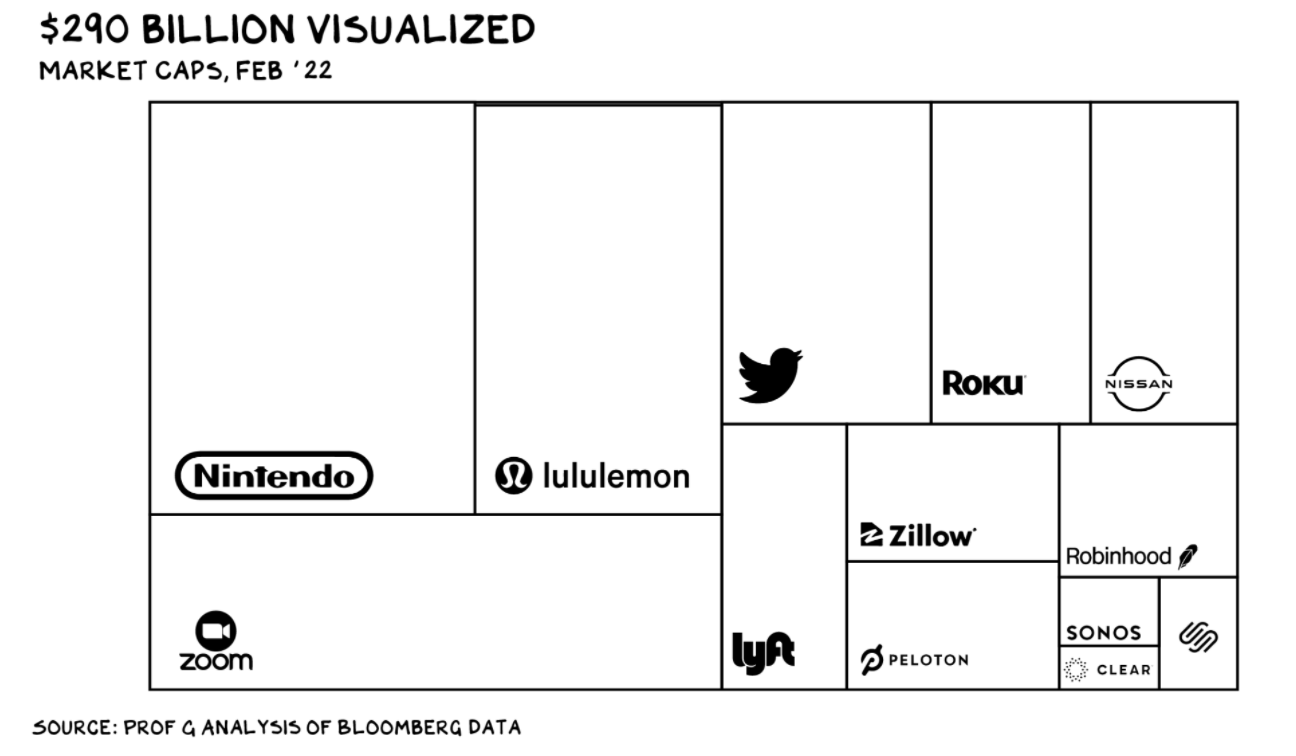

BTW, 10% of Apple is $290 billion.

Apple could swallow all these firms and the total haul would represent a smaller acquisition, on a relative basis, than Salesforce buying Slack. And then, the following year, Apple could buy Salesforce ($197 billion market cap). That’s not to say Apple could or should try to buy into all these markets at once, but it’s market cap gives the company virtually unlimited strategic agility.

So with more than $100 billion in cash and $290+ billion for M&A, where might Apple go next?

Tim Cook’s mantra is “the intersection of hardware, software, and services.” He said it twice on the company’s last earnings call, and words uttered in these calls are a tell for a firm’s plans. What does that cover? Better question: What doesn’t it cover?

Let’s Get Ready to Rundle

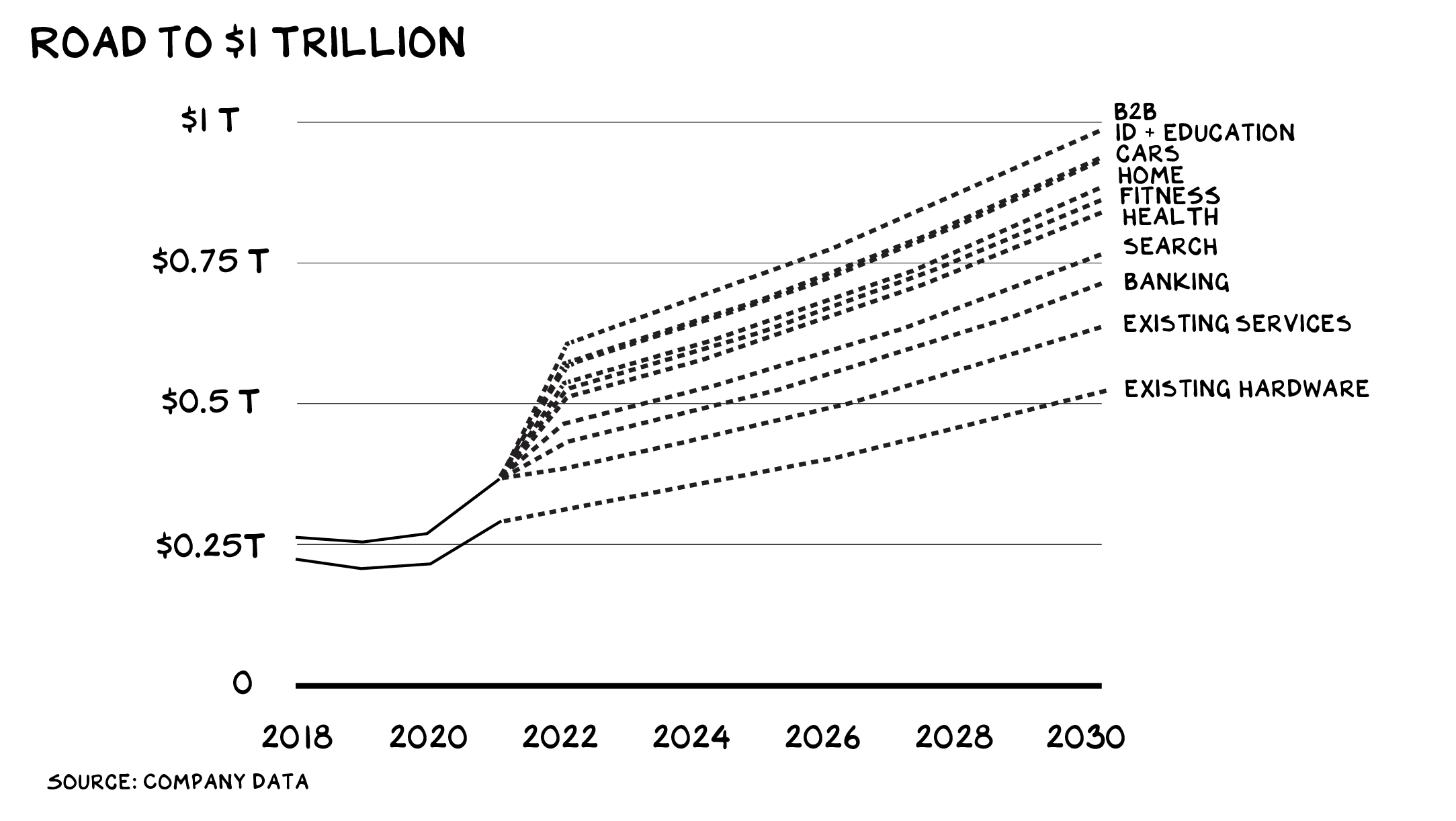

Apple’s road to $1 trillion in revenue starts with the markets it’s already in. iDevices and Macs are still setting sales records. But there’s more upside in Apple’s ancillary markets.

Apple Pay removes at least five steps of motor function required to pull out a credit card. Our lizard brain doesn’t want to fumble with wallets and pockets, and our conscious brain understands there’s no reason a cheap piece of branded plastic processes a payment better. Today, we tap. Tomorrow, Siri will confirm payment via our AirPods.

Apple has gotten off the sidelines in gaming. Mobile gaming is a nearly $100 billion market, larger than PC and console gaming combined, and 45% of it flows through the iOS App Store, where Apple charges a mob-like 30% toll.

AppleTV+ produces Murphy Brown on a Game of Thrones budget, and it’s thus far been underwhelming. But it doesn’t matter — eventually, the army with the most tanks wins. And Apple’s armament makes NATO look like Peacock. I just read the last sentence, and it makes almost no sense, but I’m too lazy to fix it. (It’s late — 4 a.m. in Tulum.)

As strong as these businesses are, Apple can unlock more value by rolling them together into the ultimate subscription product: You’d pay one monthly fee for all your Apple needs. The company currently offers AppleOne, combining the company’s media and cloud services, and, separately, the iPhone Upgrade Program, which offers a new iPhone annually in return for a monthly fee. Serving up the latest hardware (auto-shipped on release) is a no-brainer and likely coming. But Apple shouldn’t (and won’t) stop there.

So let’s play Tim Cook. Going full rundle will maintain Apple’s historic 7%-8% annual revenue growth — the company will generate $650 billion in revenue by 2030. That leaves $350 billion it needs to take from someone else.

Let’s light this candle.

Consumer Banking

Banks offer two things: capital and trust. Done and done. The next step is to let people direct their paycheck auto-deposit into their Apple Cash account (perhaps offering a modest interest rate), so they can send money or print checks to recipients not on Apple Cash. Apple could/will offer checking/savings accounts with modest tweaks to existing features.

From there, Apple moves into loans and investment products. Auto loans (offering a preferred rate on an Apple Car?), home mortgages, lines of credit. It might stretch Apple’s brand to go full Robinhood, with margin trading and crypto, but it could do something akin to Goldman’s Marcus product, a robo-advisor that directs customer’s investments toward diversified holdings.

The largest U.S. banks each pull in around $35 billion in consumer banking revenue. Investment advisers such as Schwab and Fidelity generate $10 billion to $20 billion in turnover. The industry is awash in new entrants and uncertainty. Apple is a global player that already has many of the pieces in place. By 2030, this is a $75 billion business for the Iron Bank of Cupertino.

Search

Search is the most potent advertising channel in history. It’s the bottom of the funnel for trillions in consumer purchases, the point of maximum leverage for marketers. Google made $149 billion in revenue from advertising against search results last year — greater than the total for global TV and radio businesses, and soon print, combined. Apple is already in this business, albeit in a smaller way, selling ads against App Store searches. Search is too big to ignore.

Moving into search would initially decrease Apple’s revenue, as the company would forfeit the estimated $15 billion per year Google pays to be the default search engine on the iPhone. But it’s a strategic unlock. Keeping iOS searches inside the Apple ecosystem, and integrating results with the contacts, calendars, locations, and other data in that ecosystem, would make the whole show more valuable (and undermine the value of Google’s ecosystem), driving year-over-year growth in Apple’s iCloud subscriptions and its soon-to-be-supercharged rundle. It’s coming. Apple has gone vertical in a variety of categories (i.e., microprocessors) that appeared unthinkable at the time.

Apple is unlikely to squeeze as much ad revenue from searches as Google: The search giant has structural advantages thanks to its role across the ad ecosystem, two decades of advertising AI expertise, and the absence of any moral compass. But $50 billion in annual revenue by 2030 is within reach.

Health

To date, Apple has positioned the health capabilities of the Apple Watch as a feel-good consumer benefit. Fall down, it calls 911. Have an irregular heart beat, it tells you to contact a cardiologist. But on Apple’s most recent earnings call, Tim Cook said, “we’re still in the early innings with our health work.” Apple is continuing to build an array of sensors (hardware) and data mining and analysis tools (software). The low-hanging fruit: athletic heart rate monitors. A bit further up the tree: hearing aids. But what’s likely next? Services.

“Hey Siri, does this mole look suspicious to you?”

Unless CVS starts putting devices in customers’ hands, the best decision it can make is to pay to become the default integrated health-care provider on the iPhone — the medical version of the Apple-Google search contract. Google pays about 6% of its revenue for that contract. If CVS made the same calculation, Apple would receive another $17 billion direct deposit every year.

Or, Apple could just … become CVS. There’s nothing stopping the company from turning the iPhone into a homing device for a network of Jokr-like dark stores that could deliver every consumer health-care item (plus diapers) to your doorstep. Health services and premiums aside, Apple could take out CVS’s product sales. What’s reasonable? Half? A third? Let’s say a quarter: $75 billion by 2030.

Fitness

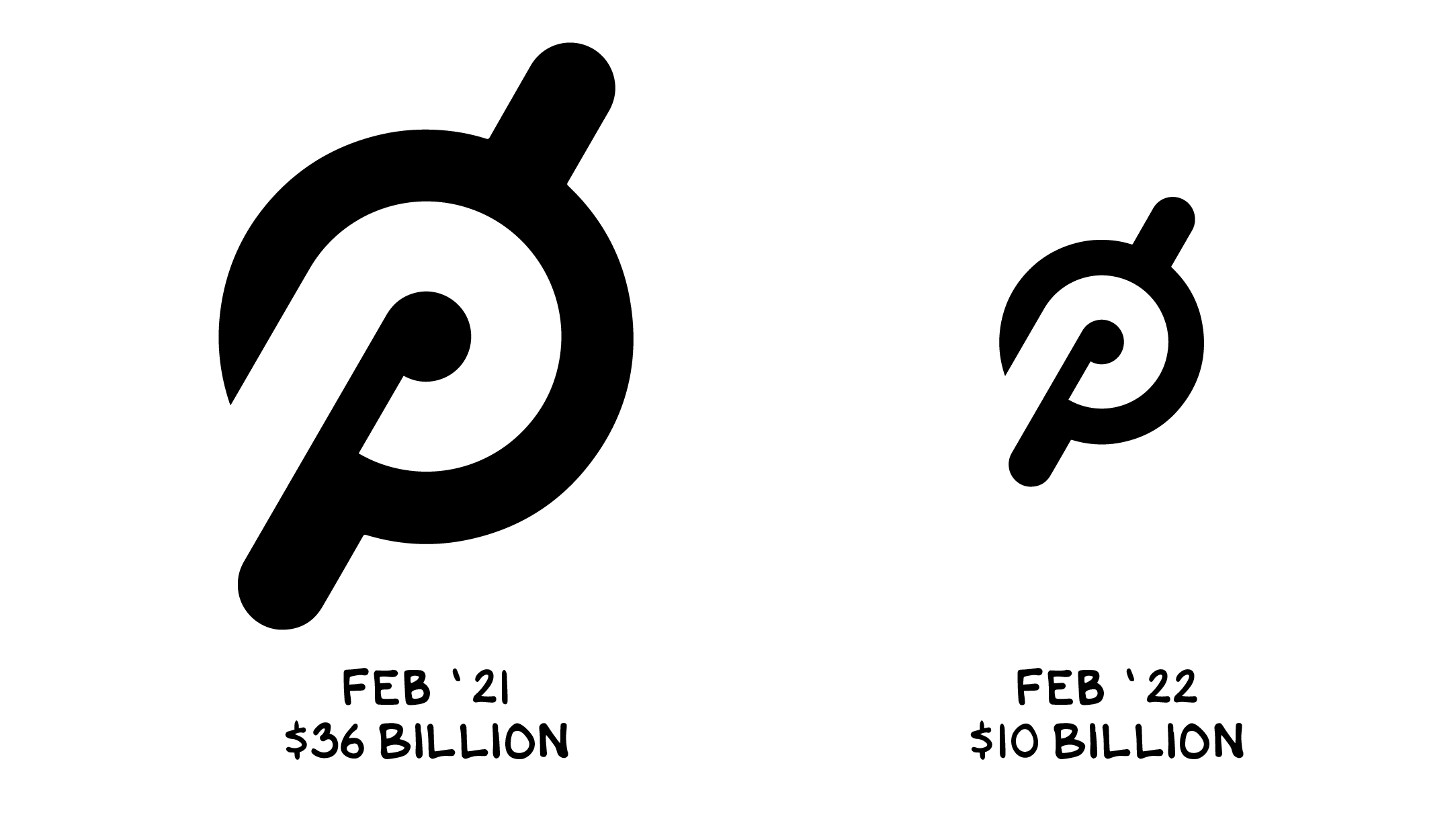

A year ago, I said Peloton’s $36 billion valuation was hard to justify. For Apple, however, I said it would be difficult not to justify paying $36 billion for two to four hours of attention per week from the most influential people on the planet. Peloton is now 70% off at $10 billion.

Peloton projects $5 billion in revenue this year, but that’s without the power of Apple behind it. Fitness is a much bigger market. Roughly 64 million Americans belong to a health club, a $40 billion industry. Gym members skew (are) rich — I speculate 75% of these people own an iPhone. Nike makes nearly $50 billion in annual revenue. This is a $20 billion business for Apple by 2030.

Home

Home automation is an $80 billion market, thanks to the potential for upgraded appliances, new tech, and services. The current Apple Home offering is weak, but once the company aims that $22 billion R&D cannon at it, the Apple brand will be a huge differentiator in a category that involves listening to your every word and watching your every move. In addition, the amount of friction in home automation is maddening. Apple reigns supreme at integrating devices, and this is where the familiar interface of iOS and that central hub in your pocket can really shine.

Connected doorbells, thermostats, and speakers are nice, but one device rules the American home: the big-screen TV. Rumors of an Apple television are a Silicon Valley evergreen. The global smart TV market is worth more than $300 billion and projected to grow to nearly $1 trillion by 2028. It’s a natural fit for Apple, which makes industry-leading displays from 1 to 32 inches in size (including the $6,000 nano-textured glass Pro Display XDR). It will be bundled with Apple TV+ and integrate the Apple ecosystem and features including Facetime and Shareplay.

I don’t see Apple getting into connected refrigerators by 2030 (not saying I wouldn’t buy one), but between smart TVs, automation control, and other devices, this is another $20 billion opportunity.

Cars

This one’s obvious: The first overnight $250+ billion transfer of shareholder value from a guy who finds humor in Hitler memes to a guy who’d never find himself in that position will occur when Tim Cook stands onstage in front of an automobile bearing an Apple logo.

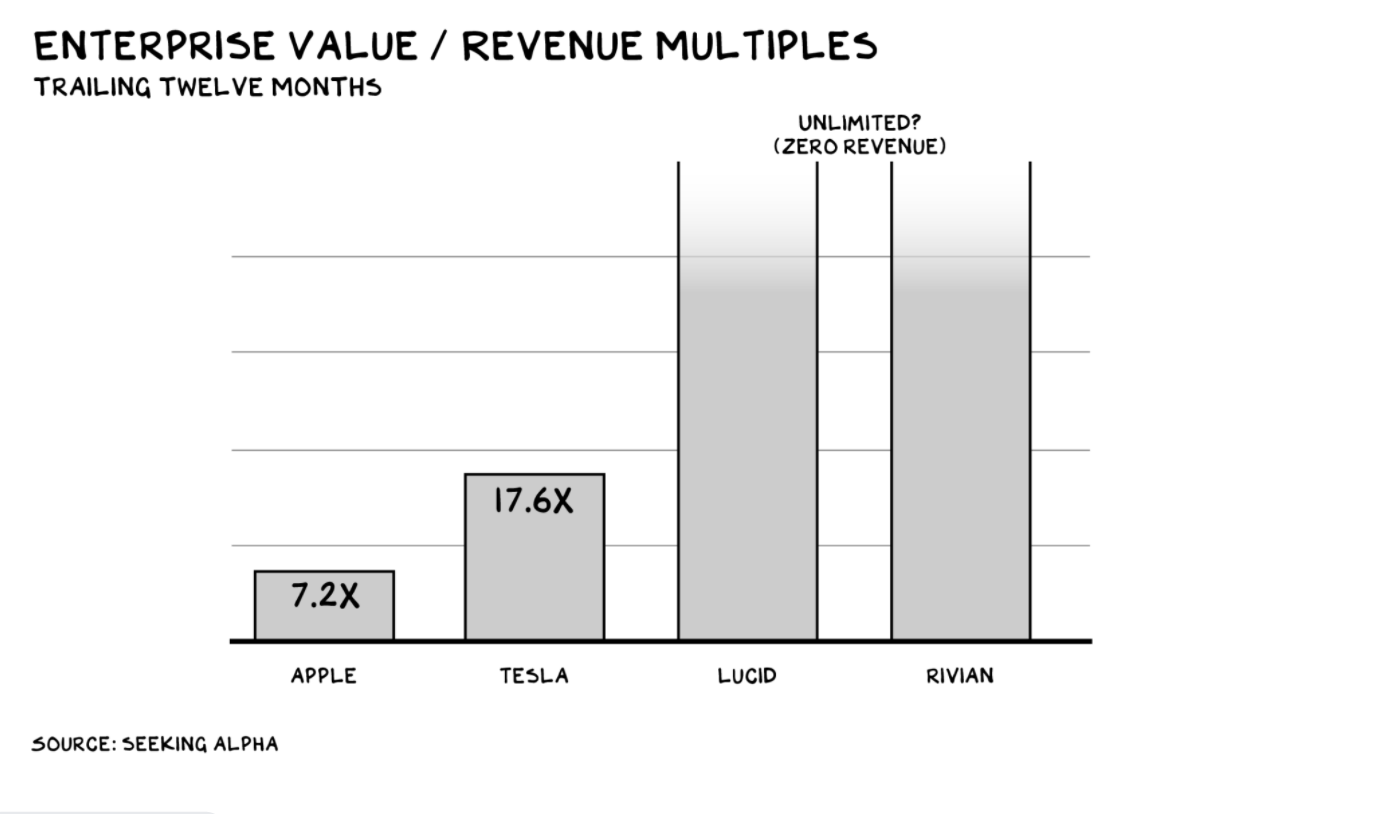

The Apple car is in the works, and it could transform the company’s business just as the iPhone did. And not to get carried away with market cap, but imagine how much Apple will be worth if it starts receiving the multiples that are now standard in the electrical vehicle market.

Tesla controls roughly 70% of the U.S. EV market today and does more than $50 billion in revenue per year. Tesla’s revenue is a drunk tourist stumbling home late at night wearing a Hublot. Apple taking half of Tesla’s sales is, in my view, a conservative estimate: $25 billion. This is a high growth market, and I expect to see $50 billion in Apple Cars driving themselves off the lot by 2030. Tim Cook cost Facebook a quarter of its market cap just flexing its privacy muscles — the Apple Car will cost the inner child from outer space a similar share of the value of his firm.

Identity and Inconveniences

The breadth of Apple’s ecosystem will sweep up many more relatively small opportunities. Anywhere that requires an ID to enter could turn that infrastructure over to Apple. Expedited airport security as a premium service, a la Clear, is an obvious fit, and why wouldn’t Madison Square Garden and The Colosseum at Caesars Palace just hand over the whole interface to Apple? Let’s call it $4 billion.

And then there’s my domain: education. It’s time for Apple to show up at reunion as an alumni who wants to make their mark. U.S. education from preschool to college is in dire need of a technological revolution. The leading provider is Blackboard, a privately held business with products that are … OK. Apple could become the operating system of education — an alchemy of Chegg, Coursera, and Udemy: $2 billion per year.

Blend up all these and more, Apple could be generating $10 billion in revenue from businesses that fall into its lap.

B2B

It’s an inevitable part of the tech cycle — innovation sparks in the consumer space, but as the tech matures, the smart players head where the real money is … the business-to-business economy. In 2020, Apple acquired a startup called Mobeewave for $100 million. It wasn’t a sexy brand acquisition like Beats, so no one cared. But we should have. Mobeewave develops technology that lets smartphones process payments with the tap of a credit card. In other words, it turns iPhones into credit card readers.

This is bad news for payment processors. Especially Square, which has been hard at work installing terminals in coffee shops since 2009. Apple’s strategy will be different. It’ll simply turn on a feature in the next software update and boom: a billion credit card machines. Out of the gate, Square offers a suite of services that Apple doesn’t, so this looks like a partnership. Sure, like a virus partners with a host.

Today, Apple relies on AWS and Google to supplement its own data centers, just to handle its consumer iCloud business. But the company is one of the largest data center operators in the world, and it’s finishing a five-year, $10 billion expansion. It’s only a matter of time before Apple flips the script and offers its own commercial cloud services.

Half of Square’s revenue (not including its “revenue” from Bitcoin) + half of AWS’s revenue = $35 billion. Eight years later it’s $50 billion.

Will I Dream?

Imagine Apple executed the above. We’d have the first $1 trillion revenue company.

At our Pivot MIA conference this week, my NYU colleague Aswath Damodaran called Apple a “rare exception” to the life cycle rules that govern almost all companies. He credits its success in part to discipline. The largest acquisition the company has ever made? A mere $3 billion for Beats — nearly eight years ago. They’ve been looking at cars, AR, and televisions for a decade or more. If it’s the first company to get to $1 trillion, and we think it will be, it’ll likely be because Cook & Company isn’t in a hurry to get there.

Life is so rich,

P.S. You haven’t taken my Brand Strategy Sprint yet, and honestly — I’m hurt. There’s still time. Sign up now or check out our scholarships.