“Lord, here comes the flood

We’ll say goodbye to flesh and blood

If again the seas are silent, in any still alive

It’ll be those who gave their island to survive

Drink up, dreamers, you’re running dry” – Peter Gabriel

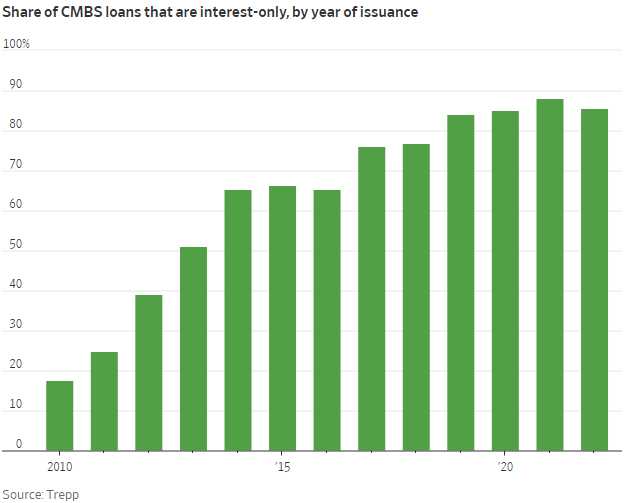

As we’ve seen this morning from Russian war crimes – it only takes one break in a dam to flood an entire region and, not to belittle the pain in Ukraine but we are facing an economic catastrophe of Biblical proportions as $1,500,000,000,000 worth of Commercial Mortgage-Backed Securities – 6% of the GDP of our nation, 85% of which are interest-only loans – are coming up for renewal over the next 3 years.

Unlike most home loans, which get paid down each year, most CMBS loans are “interest only” loans, where the borrower only pays the interest for a set period of time, usually five to seven years, and then repays the loan in full at the end of the term. These loans helped fuel a boom in Commercial Real Estate before the pandemic (4 years ago), but now many of them are coming due and many borrowers are struggling to refinance or sell their properties.

Fitch Ratings recently estimated that 35% of pooled securitized commercial mortgages coming due between April and December 2023 ($140Bn) won’t be able to refinance based on current interest rates and the properties’ incomes and values. While many malls and hotels face high default risks, the situation is particularly dire for office owners.

Many banks, fearful of losses and under pressure from regulators and shareholders to shore up their balance sheets, have mostly stopped issuing new loans for office buildings already. Office and some mall owners are currently facing falling demand for their buildings because of remote work and E-commerce. Interest rates have more than doubled for some types of commercial mortgages and the market is very wrong about rates coming down in the near future. Already CMBS issuance volume plunged by 85% year-over-year in January, from $11.9Bn in January 2022 to just $1.8Bn, reflecting impossible refinancing conditions most companies are already facing.

As you can see from the price and volume of the CMBS ETF, investors are racing to get off of this sinking ship as fast as they can. The pie chart shows delinquencies are piling up – hitting 34.9% in the Retail Sector last month and 31.5% in Office Space. Oh sure, the economy is fine…

As you can see from the price and volume of the CMBS ETF, investors are racing to get off of this sinking ship as fast as they can. The pie chart shows delinquencies are piling up – hitting 34.9% in the Retail Sector last month and 31.5% in Office Space. Oh sure, the economy is fine…

The banks, just like their borrowers, are crossing their fingers and hoping conditions are improving because there’s no point in foreclosing on a half-empty office building or a collapsing Retailer – the bank doesn’t want to own these businesses either! Again, don’t forget, these are generally interest-only loans – the principle is completely outstanding – the banks are totally screwed!

In theory, CMBS’s are just hot potatoes – they get passed around from bank to bank and they all hope they don’t get stuck with the defaulting company. Usually companies can just refinance at a higher-risk rate and that’s fine when rates are steady but now the underlying rates are 5% higher than they were when the loan was taken and rolling that over with 2 more points for risk can topple the whole house of cards as NOBODY is going to extend that kind of credit – especially when you underlying asset is devaluing.

“When the flood calls you have no home, you have no walls

In the thunder crash you’re a thousand minds, within a flash

Don’t be afraid to cry at what you see

The actors gone, there’s only you and me

And if we break before the dawn, they’ll use up what we used to be” – Same Song!

Like any good flood, this one starts with someone saying “There’s going to be a flood.” The timing of these loans means the water will keep on coming and coming and coming over the next 3 years and it’s going to impact bank earnings as well as the earnings of the borrowers, who scramble to repay or refinance these loans. Forced building sales can crash the already-fragile Commercial Real Estate Market and our new Debt Ceiling is only $4Tn higher – we can’t afford another massive bail-out – can we?

Like any good flood, this one starts with someone saying “There’s going to be a flood.” The timing of these loans means the water will keep on coming and coming and coming over the next 3 years and it’s going to impact bank earnings as well as the earnings of the borrowers, who scramble to repay or refinance these loans. Forced building sales can crash the already-fragile Commercial Real Estate Market and our new Debt Ceiling is only $4Tn higher – we can’t afford another massive bail-out – can we?

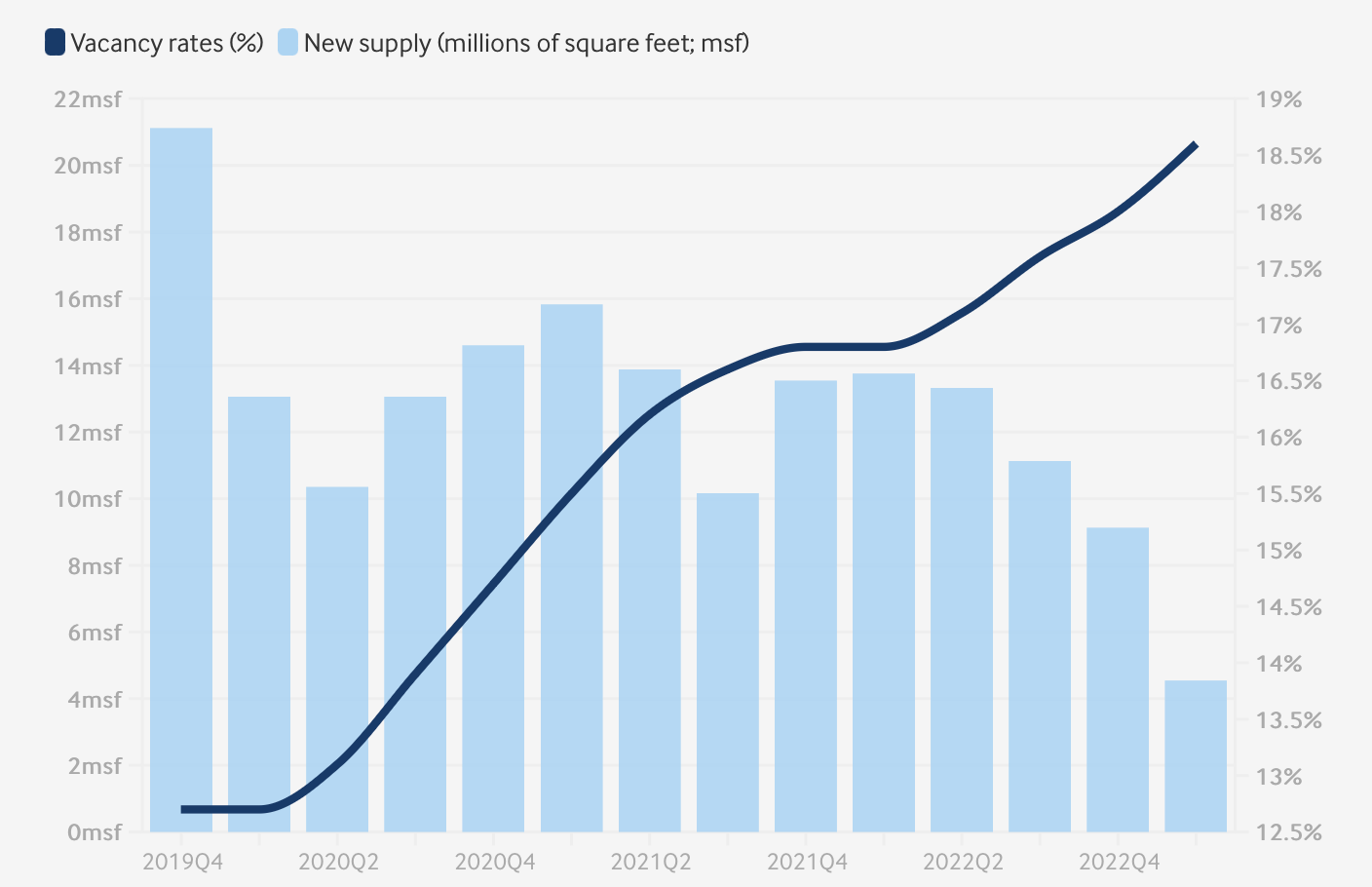

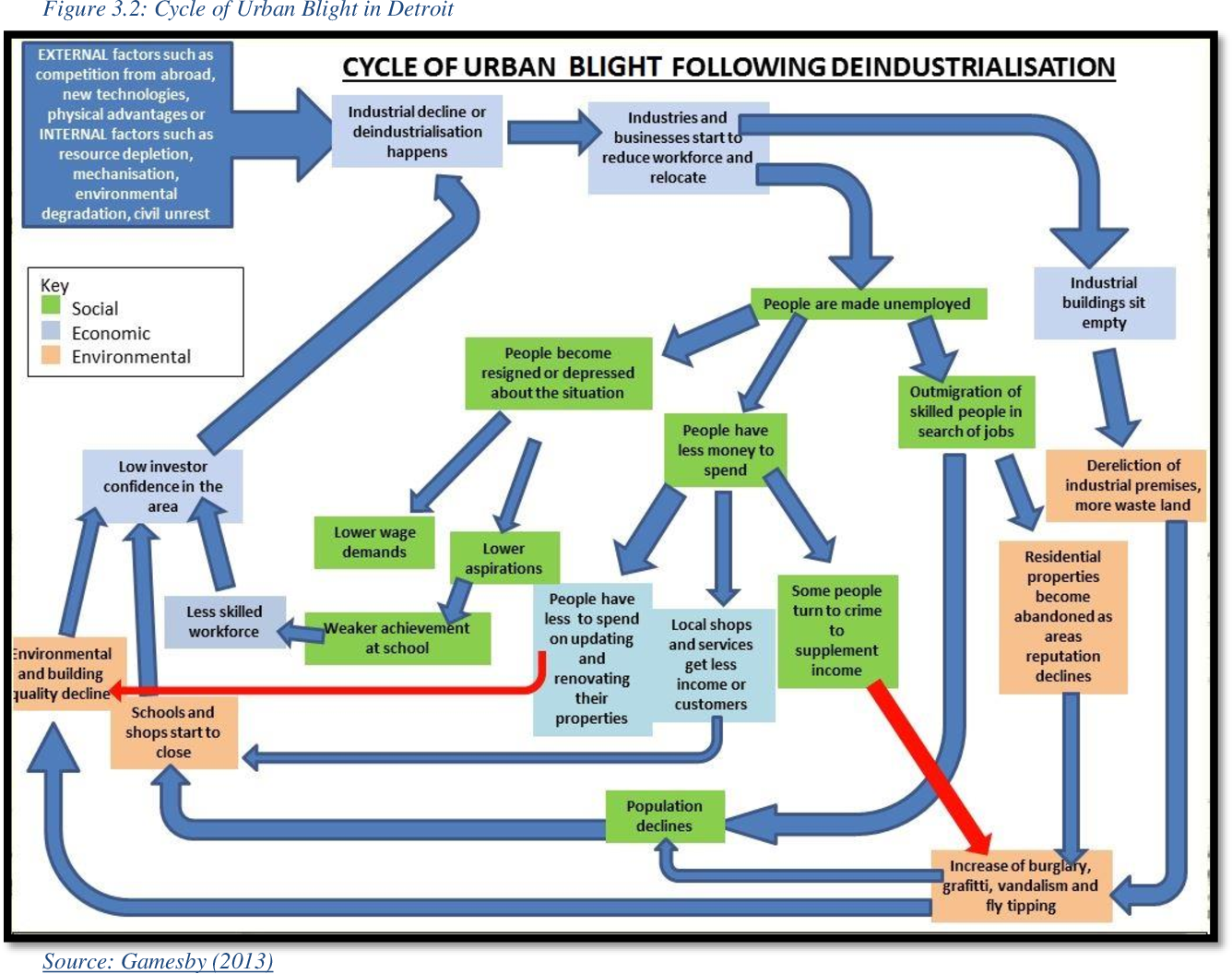

20% of CRE is already vacant (anyone walking around their town knows that) but 50% of the rented space is also unused due to the new work-from-home economy, which is turning out very much NOT to be a “fad”. Commercial leases are long so the impact is spread out but if the 80% occupied space drops half their space when they renew – that leaves just 40% of the remaining space occupied and that, my friends, looks very much like Detroit at it’s worst.

We’re already seeing the results: Perversely, as the occupancy dwindles, cities have to increase taxes and fees on the remaining landlords and tenants to make up for what they are losing but it’s never enough and infrastructure and city services begin to collapse, which cause more people and companies to leave, etc. etc…

So what is the S&P 500 so happy about? Frankly, I couldn’t tell you – it seems sort of ridiculous. We resolved the debt ceiling issue by going 13% deeper into debt and AI is going to replace about 1/3 of the workforce by the end of the century – making the CRE problem seem charming by comparison. Replacing workers with robots is great for our Corporate Masters when there are plenty of employed people left to buy their goods and services but, 30% of the population is out of work, they may begin to have issues.

Of course, the S&P 500 isn’t REALLY happy. That’s the magic trick. As it turns out more than half of the S&P 500 are still trading below their 200-day moving averages and ONLY 8 STOCKS (AAPL, AMZN, GOOGL, META, MSFT, NFLX, NVDA and TSLA) make up 32% of the S&P 500’s entire market cap AND they even double-count GOOG (which we’ve talked about before) so $1.6Tn (5%) of the $34Tn market cap of the S&P 500 is “fake, Fake, FAKE!!!“

| # | Company | Symbol | Weight | Price | Chg | % Chg |

|---|---|---|---|---|---|---|

| 1 | Apple Inc | AAPL | 7.450243 |  180.24 180.24 |

0.66 | (0.37%) |

| 2 | Microsoft Corp | MSFT | 6.9756 | 336.00 |

0.06 | (0.02%) |

| 3 | Amazon.com Inc | AMZN | 3.116038 |  125.25 125.25 |

-0.05 | (-0.04%) |

| 4 | Nvidia Corp | NVDA | 2.687968 | 389.70 |

-2.01 | (-0.51%) |

| 5 | Alphabet Inc Cl A | GOOGL | 2.093556 | 126.01 |

-0.00 | (-0.00%) |

| 6 | Alphabet Inc Cl C | GOOG | 1.834043 | 126.65 |

0.02 | (0.02%) |

You can see the proof right here. GOOG has a $1.6Bn valuation and so does GOOGL and they are both in the S&P 500 (and the Nasdaq, where it’s a much bigger fake!) as if they had a $3.2Tn valuation. That’s just ridiculous!

I don’t like to be the doom and gloom guy but, when I see nothing but happy talk in the rest of the media – I do feel an obligation to supply a little balanced perspective. There’s a reason we’re being slow to deploy capital in our new Member Portfolios and we’ll discuss that a lot more between now and next Friday.

Until then – be careful out there!

{kind=link}