This is a biggie.

This is a biggie.

Job creation has been running hot for over 2 years now and all this rate-hiking by the Fed was supposed to calm things down. Instead, according to yesterday’s ADP Report, along with the planet – jobs are heating up this summer – not cooling down!

Economorons have consistently underestimated job growth this year and the Federal Reserve is closely monitoring wage data, expecting an increase in average hourly earnings, which would add pressure for further interest rate hikes to combat inflation. Some members of the Fed’s rates committee have already expressed the need for more rate increases. The overall employment picture is somewhat perplexing, as there are fewer job vacancies compared to a year ago, and the “great resignation” trend appears to be fading, suggesting a potential easing in wage growth.

However, other indicators, such as data from ADP showing a surge in hiring, especially in the leisure and hospitality sector, and a decline in JOLTS jobless claims, indicate a robust labor market. These figures imply that the jobs report may reveal strong job growth. Jeffrey Roach, an economist at LPL Financial, believes that signs point to another positive jobs report.

Despite the positive outlook on jobs, Wall Street seems to be preparing for negative news. Futures markets are pricing in a potential 0.25 percentage point increase in interest rates at the Fed’s upcoming rate-setting meeting, with growing odds of a second increase in September. Stocks and bonds declined after the ADP numbers were released, as investors expressed concerns that further Fed actions could hamper economic growth.

The Fed’s own economists have predicted a mild recession in the fourth quarter, but this projection could change based on the jobs report. The minutes from the Fed’s recent meeting indicate that the staff sees the possibility of continued slow economic growth and the avoidance of a downturn as almost as likely as the mild-recession baseline, given the strength of the labor market and consumer spending resilience.

A strong jobs report today could complicate the Federal Reserve’s efforts to control inflation. Positive job growth may lead to pressure for further interest rate hikes, which has sparked concerns among investors about potential harm to economic growth. The overall economic outlook, including the potential for a recession, may depend on the outcome of the jobs report.

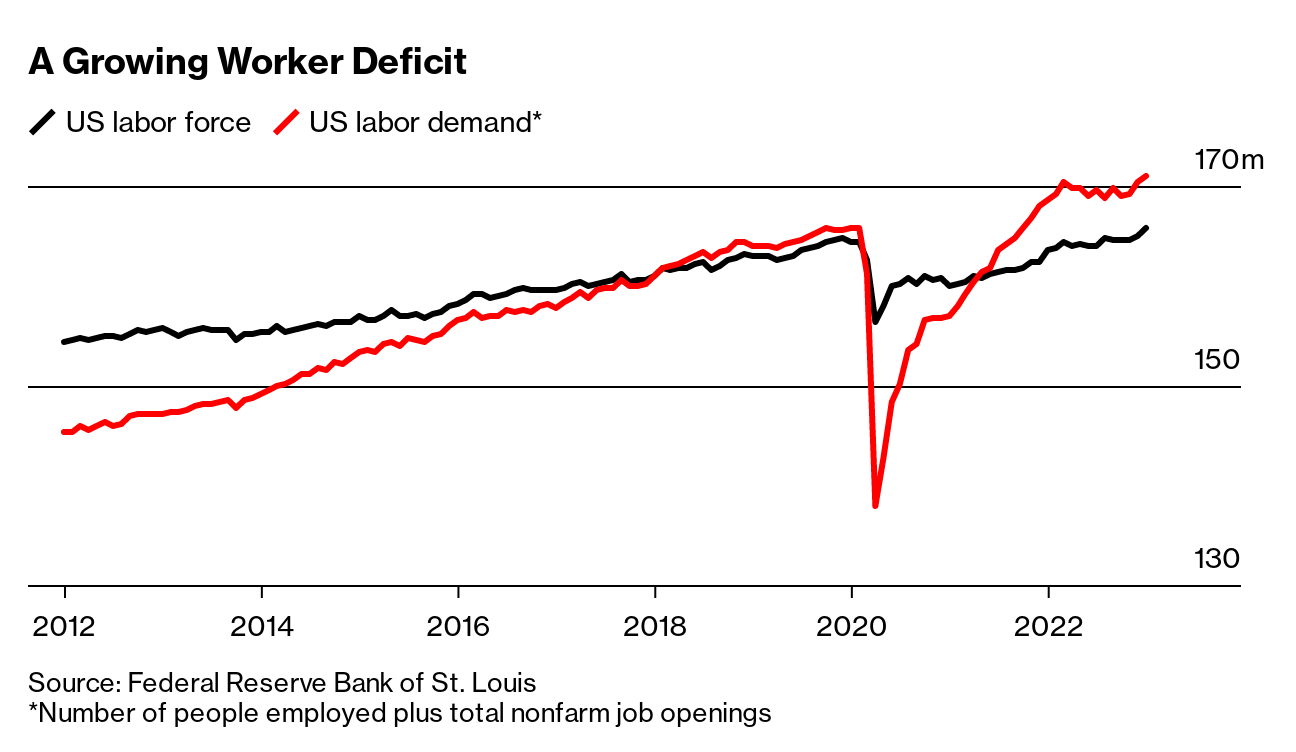

As I said in yesterday’s Webinar, the job and wage situation in the US (and Globally) is a slow-moving macro issue that is NOT going away. We are facing a long-term labor shortage in the US due to many factors, including:

-

-

Demographic changes: Low birth rates and an aging population have reduced the number of people entering the workforce. The retirement of the baby boomer generation exacerbates this trend, creating a gap between the number of retiring workers and new entrants.

-

Immigration policies: Restrictions on immigration and deportation of immigrants in recent years have reduced the pool of available workers. Immigration plays a significant role in filling labor market gaps, especially in sectors such as agriculture, construction, and hospitality.

-

Skills mismatch: There is a disconnect between the skills possessed by job seekers and the skills demanded by employers. Rapid technological advancements have created a demand for workers with specialized skills, while many job seekers lack the necessary training or qualifications.

-

Education and training: Disruptions caused by the COVID-19 pandemic, including lockdowns and remote learning, have impacted the quality and continuity of education. This can result in graduates who may lack the practical skills and experience desired by employers.

-

Generational shifts and changing job preferences: Younger generations often seek different types of work arrangements, prioritizing factors such as work-life balance, flexibility, and purpose-driven careers. This shift in preferences can contribute to labor shortages in traditional industries that may not align with these priorities.

-

Pandemic-related factors: The COVID-19 pandemic has led to various factors affecting the labor market. Some workers may be reluctant to return to work due to health concerns (long Covid), childcare challenges (which we’ve discussed), or even enhanced unemployment benefits themselves. Industries such as hospitality and tourism have been particularly impacted by reduced travel and restrictions.

-

Retention and wage issues: Companies may struggle to attract and retain workers due to factors such as low wages, inadequate benefits, and limited career advancement opportunities. In some cases, businesses may need to reevaluate their compensation and benefits packages to attract qualified employees.

-

It’s important to note that the labor shortage is a complex issue influenced by multiple factors that can vary across regions and industries. Addressing these challenges requires a comprehensive approach involving policy changes, investments in education and training, and efforts to align the skills of the workforce with evolving job market demands. The Fed can’t just wave their magic rate wand and make this all go away!

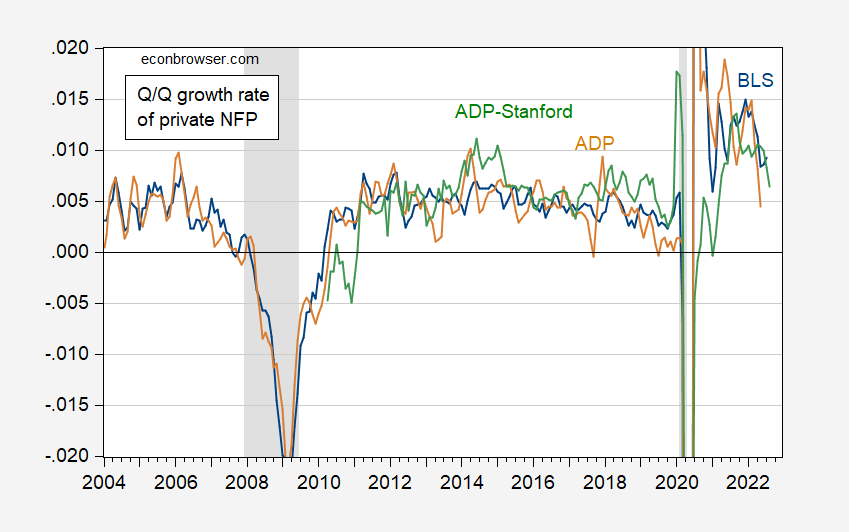

8:30 Update: Forget what I just said – 209,000 jobs added is LOWER than 230,000 expected and nothing like ADP and last month was revised down 33,000 and April has been revised down by 77,000 – we’ll have to see what the data reveals as we did deeper but this should be quite a relief for the markets.

Oddly enough, the Unemployment Rate dropped from 3.7% to 3.6% and the Average Workweek rose from 34.3 to 34.4 hours and, even more importantly, the Average Hourly Earnings went up from 0.3% to 0.4% (+4.8% annualized) – these are all contrary to the job count – possibly they have made a “seasonal adjustment” that has brought the numbers down – which is why there is such a mismatch with ADP.

As you can see from the chart, USUALLY ADP and NFP are pretty much in sync so we just have to wait and see when they are moving in different directions. This is nothing for the markets to get excited about and I think the overall pressure will still be lower into earnings next week (yes, it’s that time again!).

Meanwhile, another weekend is upon us – 3-day workweeks would solve a lot of problems…

Have a great weekend,

-

- Phil

{kind=link}