Happy Monday!

Everything you see this morning is artificial as the Japanese Yen hit an all-time low this weekend and this morning, the BOJ took emergency measures to prop up the currency by dumping Dollars and buying Yen.

This is what happens when your country goes deeper and deeper in debt while you try to maintain ridiculously, artificially low interest rates because, if you didn’t, the interest on your 1,300,000,000,000,000 (1.3 QUADRILLION) Yen debt would be 26Tn Yen at just 2% and the ENTIRE budget of Japan is 110Tn Yen ($687Bn) so debt service alone at 2% would be 23% of their budget but it’s much worse than it seems because 36% of Japan’s annual outlays are already deficit spending.

If Japan had to actually pay 5% interest on their borrowed money, then there would be no money left in the Government budget for anything else so they are desperately manipulating their currency to attempt to stop it’s decline because bondholders who invest in declining currencies expect the interest rates to offset those risks and – Catch 22 – Greece is the word!

Despite losing the #3 spot to India this year, Japan’s GDP is $4.2Tn, about 20% of ours and economic upheaval over there (or even a default), will send ripples across the Pacific that will certainly be felt over here.

They already are this morning as the Dollar is down 0.5% and that’s popping the indexes as well as commodities but the BOJ simply can’t keep this up and, rather than restoring confidence in the Yen, moves like this smack of desperation and can induce a reaction that is the opposite of what they intended. Stay tuned!

Anyway, that’s all the way on the other side of the World – give the globe a quarter turn to the left and we get to the Middle East, where peace is in danger of breaking out and that makes Oil Traders very unhappy but not us, as our Members took a short on Friday morning at 9:34 as I said the following in our Live Chat Room:

Oil is $84.23 and /BZ is $89.62 so I say short /CL here and stop out if /BZ breaks over $90. Risky into the weekend, of course but Oil couldn’t hold $85 even when bombs were actually being dropped on Iran and Israel and I’m not seeing anything that indicates escalation this weekend.

As you can see we pretty much nailed it and we were up $1,230 per contract at $83 before the bounce but those who are still in it can look forward to a massive breakdown once this weak-Dollar nonsense washes over us and currencies go back to normal as the BOJ’s manipulations are the only thing keeping oil from re-testing $82.

See, day trading is fun! And, speaking of fun, we’re getting into the fun part of earnings season next week – after we get away from about 30% of the S&P 500 reporting this week. With all that data behind us, we should be able to make some decent predictions on the stragglers but, for now, we’ll just keep going with the flow:

And all this doesn’t happen in a vacuum. We also have a new rate announcement from the Fed on Wednesday (spoiler – nothing will happen) and then Powell speaks at 2:30 and we’ll be covering that one LIVE – during our trading webinar (1-3pm, EST) – tune in for that too!

See, we’re a good 8 years away from being Japan!

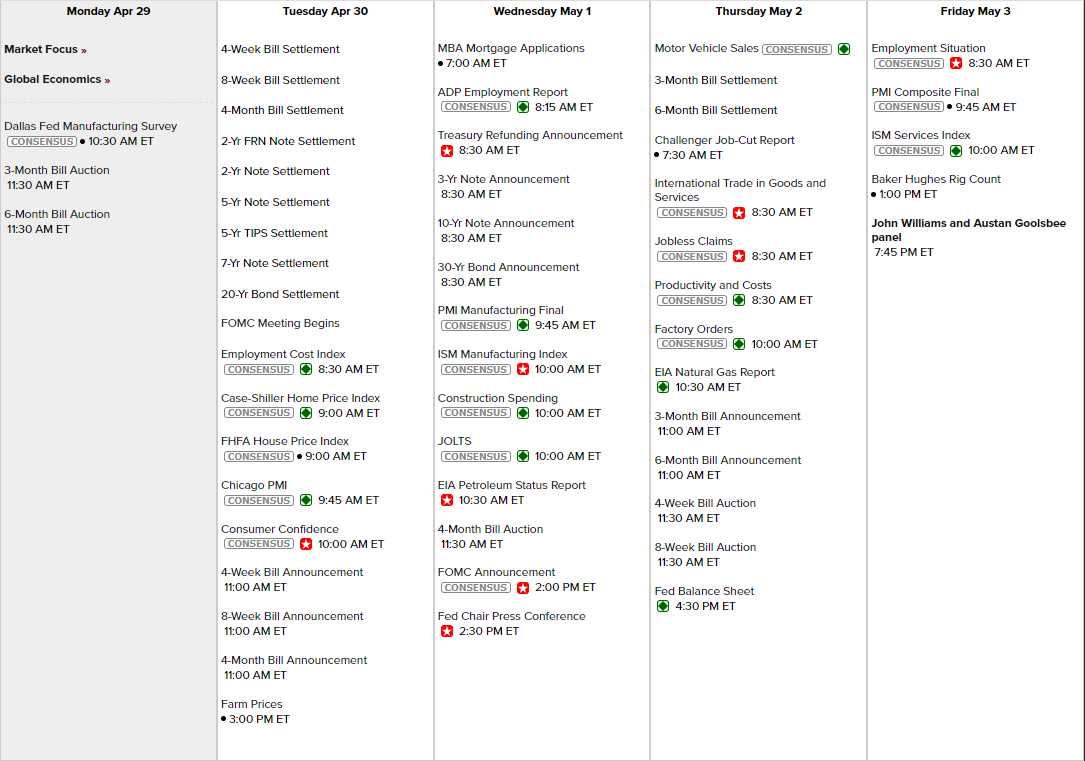

Anyway, debt, debt, debt and some data like the Dallas Fed this morning and Chicago PMI tomorrow along with Case-Shiller, Home Prices and Consumer Confidence (likely to be a buzz-kill). Wednesday it’s debt, debt, debt and PMI, ISM, Construction Spending, JOLTS, the Fed Statement and Powell’s BS. Thursday starts out with debt but then Productivity (which has been the only bright spot in the economy) and Factory Orders, followed by more debt and Friday it’s the Big Kahuna – Non-Farm Payrolls with PMI and ISM and then there’s some sort of Fed Panel overnight – in case Powell spooks the market and they need to steer us away from the rocks again…

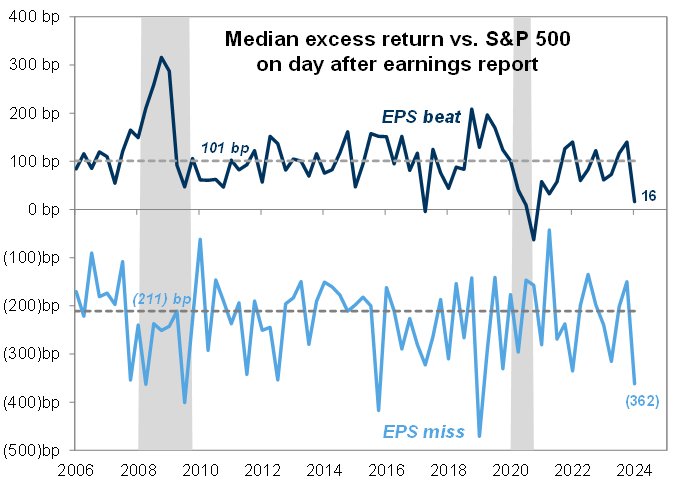

So far, this earnings cycle, 228 S&P 500 companies have reported and 63% have beat consensus and only 10% have missed by more than one standard deviation BUT expectations were SO HIGH that even the companies who beat barely moved the scales while the companies that missed have been severely punished. Interesting times indeed:

{kind=link}