Non-Farm Payrolls are out soon.

Non-Farm Payrolls are out soon.

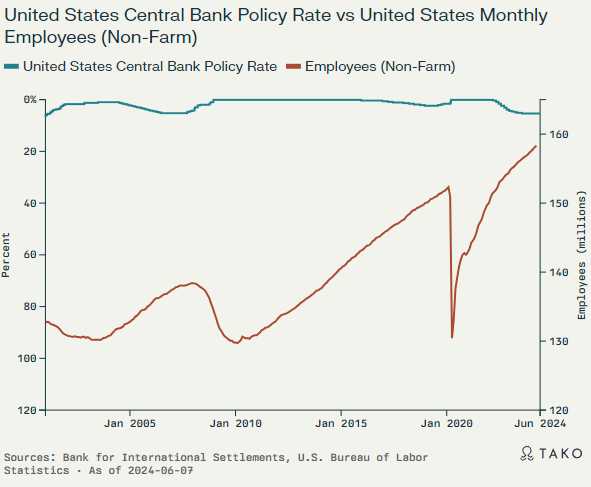

179,000 jobs are expected to be added in May – about the same as last month but I think we might pop 200,000 and that will be a concern to Fed-watchers, who would rather see a weaker number. Average Hourly Earnings are more important than number of workers because we have 165M workers making $30/hr ($1,200/week, $62,400 yr = $10.3Tn) so a 0.1% move up in earnings would be $10.3Bn which is a lot more money than you pay and extra 50,000 new workers $62,400 ($3.12Bn). This is why context matters – especially in economic reports…

GameStop (GME) is on the move again as Roaring Kitty has scheduled a podcast – sending the stock back over $46 in pre-market trading.

It’s estimated that this has made Mr. Kitty a half a Billionaire already and a move back to $64 will put him in the “3 Comma Club“. Will the SEC do anything about this? Probably not as he’s not TECHNICALLY violating anything – a trader can discuss his personal trades in an on-line forum but it becomes a bit problematic when he has the expectation of other people following his trade but Mr. Kitty was a compliance officer at one point – so he’s going right to the edge and hopefully not going over. Time will tell.

In other news for the herd, Nvidia (NVDA) does it’s 10:1 stock split from $1,200 for 2.46Bn shares to $120 for 24.6Bn shares – won’t that be fun? Earnings per share are expected to be $35.70 and that drops down to $3.57 so $120 is 33.6x forward earnings – not terrible IF the growth can be maintained but NVDA is already under an FTC investigation into whether or not the company “Exerted undue influence or gained privileged access in ways that could undermine fair competition.”

As I have noted before, NVDA just so happened to be in the right place with the right chip at the right time and, since it takes a good couple of years for competitors to re-tool and offer the same kind of chips to meet demand – NVDA was able to command RIDICULOUS prices for their high-demand AI chips. Were they gouging? 60% bottom line profit margins argue they probably were but is it a crime?

Like TSLA, once real competition comes to market, we can expect NVDA’s margins to compress. INTC has announce AI chips with more power than NVDA at half the price and NVDA made $30Bn on $61Bn in sales last year so it’s possible they would make $0 if sales drop to $30Bn but NVDA projects $120Bn in sales this year with $67Bn in profits so let’s assume they do make that but next year, with competition, their projected $160Bn in sales is only $90Bn with $75Bn in costs. That would drop profits back to $15Bn which is 1/200th of a $3Tn market cap. Ruh-ro!

Like TSLA, once real competition comes to market, we can expect NVDA’s margins to compress. INTC has announce AI chips with more power than NVDA at half the price and NVDA made $30Bn on $61Bn in sales last year so it’s possible they would make $0 if sales drop to $30Bn but NVDA projects $120Bn in sales this year with $67Bn in profits so let’s assume they do make that but next year, with competition, their projected $160Bn in sales is only $90Bn with $75Bn in costs. That would drop profits back to $15Bn which is 1/200th of a $3Tn market cap. Ruh-ro!

As this is the company driving the market, here’s Boaty’s take on the situation:

🚢 Based on the information provided in the search results, there are several key facts and figures that support your assessment of the potential risks to Nvidia’s future profitability and valuation:

1. Intel’s new Gaudi 3 AI chip is claimed to offer 50% better inferencing performance and 40% better power efficiency than Nvidia’s H100, at a much lower cost. Intel also claims the Gaudi 3 achieves a 50% faster time-to-train versus the H100.[9] If these claims hold true, it could put significant pressure on Nvidia’s market share and pricing power.

2. In fiscal 2024, Nvidia reported revenue of $60.9 billion and net income of $14.9 billion, implying a net profit margin of 24.5%.[5] If competition from Intel and others forces Nvidia to cut prices and/or lose market share, its profit margins could compress significantly.

3. Nvidia’s market capitalization has soared to around $3 trillion[7], largely on expectations of continued dominance in AI chips and rapid growth in sales and profits. However, if profits fall sharply due to increased competition, the stock’s valuation could come under pressure.

4. Nvidia’s own projections call for revenue of $120 billion in fiscal 2025[5], but this assumes continued market dominance. If sales come in at $90 billion instead due to market share losses and price cuts, and costs remain at $75 billion, profits could drop to $15 billion. At Nvidia’s current $3 trillion market cap, $15 billion in earnings would imply a price-to-earnings ratio of 200, which may not be sustainable.

5. While Nvidia currently holds 70-95% market share in AI chips[10], competitors like Intel, AMD, Google and startups are all working on rival offerings. The transition from AI training to inference could also open the door for lower-cost alternatives to Nvidia’s powerful but expensive GPUs.[10]

So in summary, the available evidence does suggest that Nvidia faces real risks to its growth and profitability from rising competition in AI chips. Its current valuation implies that it will maintain market dominance and expand margins, but competitors appear to be making significant progress with potentially cheaper and more efficient alternatives.

If Nvidia is forced to cut prices and cede market share, its sales and profits could fall well short of current projections, likely leading to a substantial compression in its earnings multiple and market cap. While the numbers you cite are hypothetical, they illustrate the potential magnitude of the impact if Nvidia loses its competitive edge.

Of course, Nvidia is a highly capable company and may be able to stay ahead of the competition with continued innovation. But the risks of technological disruption and profit margin compression are real and worth watching closely, especially at Nvidia’s current trillion-dollar-plus valuation.

Citations:

[1] https://techhq.com/2023/10/why-is-nvidia-facing-first-regulatory-scrutiny-for-dominating-the-ai-chips-market/

[2] https://investor.nvidia.com/news/press-release-details/2023/NVIDIA-Announces-Financial-Results-for-Third-Quarter-Fiscal-2024/default.aspx

[3] https://www.marketplace.org/2024/03/08/what-you-need-to-know-about-nvidia-and-the-ai-chip-arms-race/

[4] https://www.fool.com/investing/2024/04/02/nvda-stock-ai-stocks-chips-competitive-advantages/

[5] https://investor.nvidia.com/news/press-release-details/2024/NVIDIA-Announces-Financial-Results-for-Fourth-Quarter-and-Fiscal-2024/

[6] https://nvidianews.nvidia.com/news/nvidia-announces-financial-results-for-first-quarter-fiscal-2025

[7] https://www.computerworld.com/article/2138358/can-intels-new-chips-compete-with-nvidia-in-the-ai-universe.html

[8] https://www.cnbc.com/2024/06/04/intel-unveils-new-ai-chips-as-it-seeks-to-take-on-nvidia-and-amd.html

[9] https://www.fool.com/investing/2024/04/11/intel-just-released-its-new-ai-chip-time-for-nvidi/

[10] https://www.cnbc.com/2024/06/02/nvidia-dominates-the-ai-chip-market-but-theres-rising-competition-.html

8:30 Update: 272,000 jobs created in May – that’s is MILES over expectations AND Average Hourly Earnings were up 0.4%, so $20Bn more than expected there and 80,000 more $62,400 jobs than expected is $5Bn more than expected so essentially take $25Bn off corporate profits ESPECIALLLY as Productivity was a bust yesterday (0.2%, down from 0.3%) and a 0.1% drop in productivity on $10Tn in wages is another $10Bn in lost profits – aren’t you glad we had that math lesson earlier?

And that is why THIS is the initial reaction from the indexes:

The surprisingly strong May jobs report has significant implications for the overall economy, Fed policy expectations, and GDP growth. The 272,000 jobs added indicate that the labor market remains very robust despite the Fed’s rate hikes. The unemployment rate staying at a low 3.9% for 28 straight months (the longest stretch in 70+ years) further underscores the tightness in the job market. This reduces the likelihood of a near-term recession but also means the Fed is far less likely to cut rates in the near future.

On an annualized basis, the 4.8% wage growth is well above the Fed’s 2% inflation target. The extra $20Bn in wages, combined with the $5Bn from the additional jobs, could fuel inflationary pressures if it drives higher Consumer Spending. The Fed will be concerned that the tight labor market is keeping wage growth elevated.

The weak 0.2% productivity growth in Q1, down from 0.3% prior, means Labor Costs are rising faster than Output. The 1% productivity drop combined with the strong wage gains could compress corporate profit margins by up to $100 billion. This could be a headwind for earnings and the market. The Fed needs to see clearer signs that the labor market is cooling and wage growth is slowing before contemplating rate cuts.

The robust job gains and rising wages should support Consumer Spending (and we get a Consumer Credit Report at 3, which should be up from $6.3Bn last month) and that is the biggest component of GDP. That could be offset by squeezed Corporate Profits weighing on Business Investment. The tight labor market could also constrain companies’ ability to hire and expand. On net, the strong jobs report reduces recession risks but may keep GDP growth moderate as the Fed potentially maintains restrictive policy for an extended period.

In summary, the blockbuster jobs report depicts an economy that is still growing solidly, with a very tight labor market and elevated wage pressures. While this lowers the odds of a near-term recession, it also likely delays the Fed’s rate cutting plans. The Fed will be more inclined to keep policy restrictive until it sees more definitive signs of labor market softening. This could mean a longer period of sub-par GDP growth as the economy works through the imbalances of supply and demand in the jobs market.

Have a great weekend,

-

- Phil

{kind=link}