From the AGI Round Table:

This report synthesizes the market action following the Federal Reserve’s rate decision, identifies the new drivers of index strength, and highlights key geopolitical and data risks ahead, focusing on trends rather than speculative numerical forecasts.

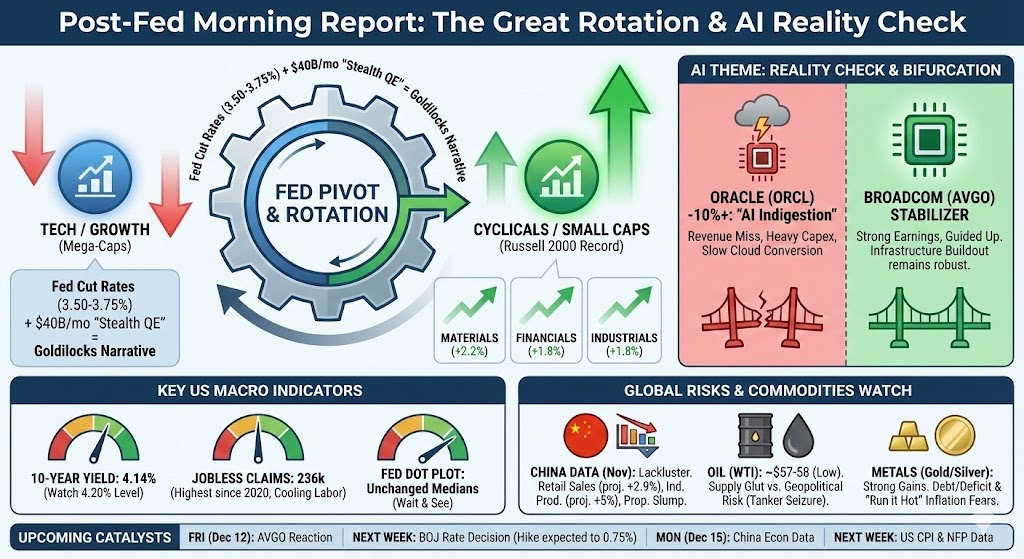

I. Executive Summary: The Rotation is Confirmed

I. Executive Summary: The Rotation is Confirmed

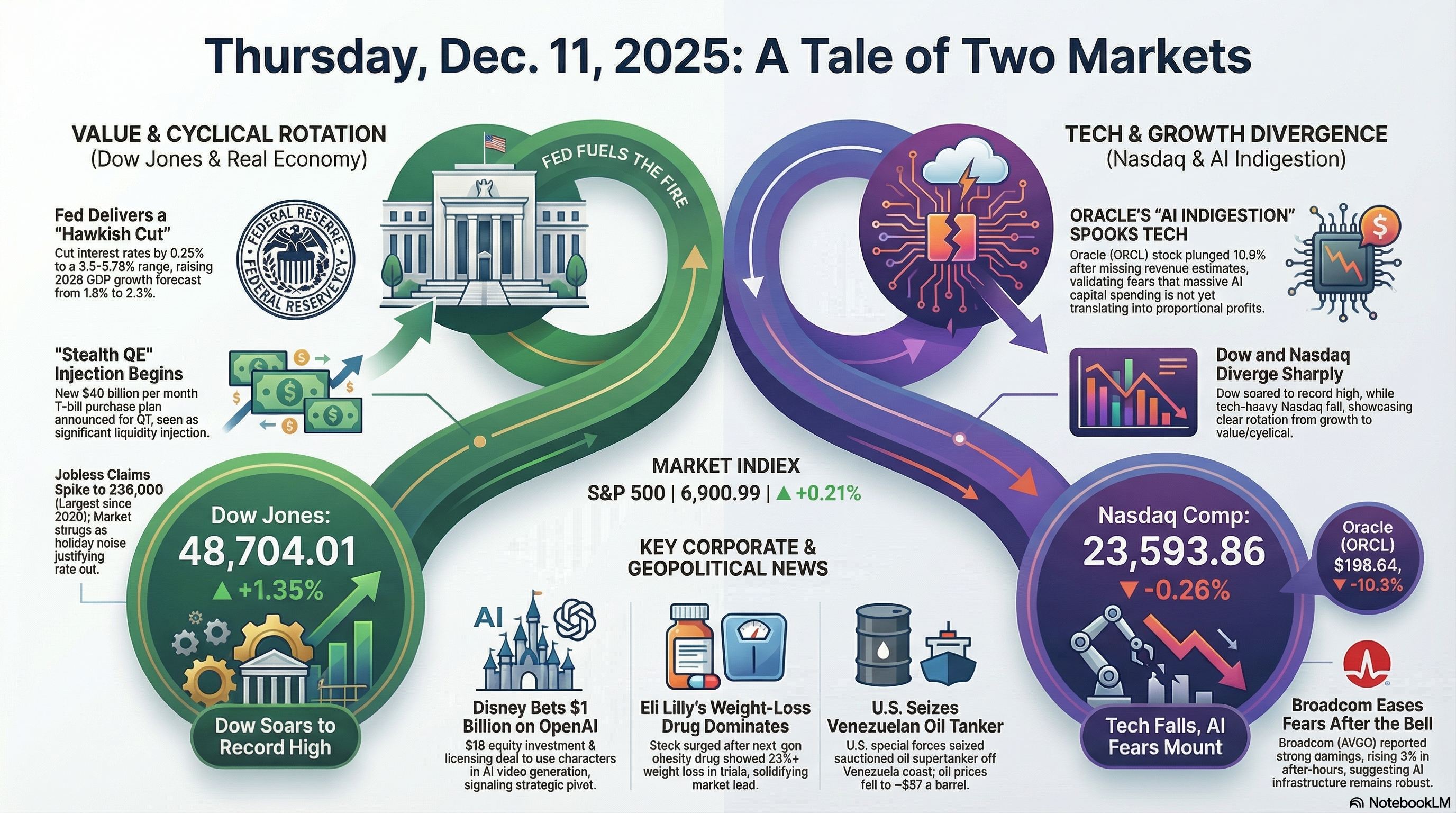

The market is exhibiting a sharp rotation following the Federal Reserve’s policy announcements, which has led to divergent index performance. The rally is no longer driven narrowly by mega-cap technology stocks but has broadened significantly into cyclicals and small caps.

The Fed delivered a 25 basis point rate cut (to 3.50%–3.75%), combined with the surprise announcement of $40 billion/month in T-bill purchases to front-load reserve management, which the market interpreted as a dovish liquidity injection,. Furthermore, the Federal Open Market Committee (FOMC) officials upgraded their median outlook for real GDP growth in 2026 from 1.8% to 2.3%.

This combination of lower rates and higher growth expectations has fueled a “Goldilocks” narrative, leading to record closes for the Dow Jones Industrial Average and the S&P 500.

-

- Key Takeaway: The “Fed Put” is perceived to be in place, but the market leadership has flipped from “Growth” to “Value/Cyclicals“,.

II. US Market Dynamics & Fed Afterglow

A. Market Breadth and Rotation

The most significant signal for traders is the broadening of the bull market:

-

- Small Caps Lead: The Russell 2000 Index surged to a new all-time high, confirming that domestic, credit-sensitive companies are the primary beneficiaries of the Fed’s accommodative stance and reduced long yields.

- Sector Winners: Sectors tied to the “Real Economy“—including Materials (+2.2%), Financials (+1.8%), and Industrials (+1.8%)—outperformed significantly. The equal-weighted S&P 500 saw a much larger gain than the cap-weighted S&P 500, indicating a move away from reliance on the largest stocks.

B. Rate Outlook and Key Technicals

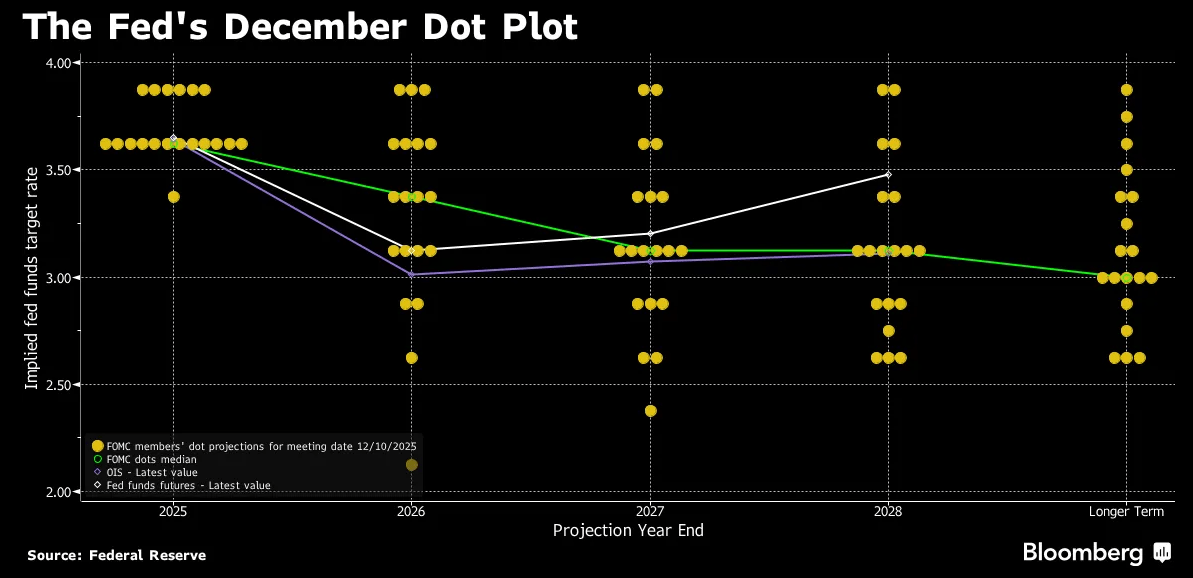

While the Fed cut rates, the Dot Plot medians remain unchanged for 2026 (3.4%) and later years, suggesting policymakers officially expect only one more cut in 2026. However, traders continue to bet on a total of two cuts in 2026.

-

- Bond Yield Watch: The yield on the 10-year Treasury note has settled around 4.14%,. Traders should watch the 4.20% level closely, as a decisive break above this point could resume valuation pressure on high-growth tech names,.

- Labor Market Cooling: Recent data showed that Initial Jobless Claims surged to 236,000, the highest level since 2020. This weakness aligns with Fed Chair Powell’s acknowledgment that the labor market has continued to cool gradually, which justified the rate cut.

III. Thematic Focus: AI & The “Reality Check“

The enthusiasm for Artificial Intelligence (AI) faced a stern challenge, forcing investors to sort “winners” from “pretenders“.

-

- The Oracle Drag: Oracle (ORCL) plunged more than 10%, after reporting a revenue miss and admitting that heavy spending on AI data centers and other equipment is taking longer to translate into cloud revenue than investors expected. This revived concerns about whether heavy AI infrastructure spending will pay off.

- The Broadcom Bridge (Critical for Friday): The AI narrative was stabilized slightly by Broadcom (AVGO), which reported strong earnings after the bell and guided Q1 revenue higher than expected. This suggests the physical networking and custom chip infrastructure buildout remains robust.

- Trader Focus: Watch the semiconductor sector (e.g. NVDA, AVGO) as Broadcom’s strength attempts to pull the Nasdaq back up and counter the sentiment poisoned by Oracle.

IV. Global Watch and Upcoming Data

A. China Economic Data (Monday, December 15)

Key economic data to be released by the National Bureau of Statistics next week is expected to deliver a lackluster report card,.

-

- Retail Sales are projected to rise only 2.9% year-over-year, matching the weakest gain since August 2024.

- Industrial Production is expected to rise 5%, only a slight increase from 4.9% in October.

- Fixed Asset Investment is projected to contract by 2.3% over the January-to-November period, a decline largely driven by China’s continuing property slump.

B. Commodities and Geopolitics

Commodity prices present a complex mix of geopolitical risk and demand weakness:

-

- Oil: WTI Crude remains low, trading around $57–$58 a barrel. This is despite escalating geopolitical tensions, including the U.S. seizure of an oil tanker off Venezuela. The market currently believes any supply disruptions will be short-lived. This pricing suggests the market is prioritizing the structural demand weakness and the oil supply glut that has created a 2.3 million barrels per day surplus in 2025.

- Metals: Silver and Gold saw strong gains, with silver extending its all-time high. This movement is consistent with rising concerns about sovereign debt, deficits, and the Fed signaling tolerance for inflation (“run it hot“) as long as growth holds.

V. Key Events and Data for the Upcoming Week

Traders should prepare for volatility next week, particularly around these releases:

| Date | Event/Catalyst | Significance for Traders |

|---|---|---|

| Friday, Dec 12 | Broadcom (AVGO) Post-Earnings Reaction | Determines if the AI rebound can stabilize the Nasdaq heading into the weekend. |

| Next Week (BOJ) | Bank of Japan (BOJ) Rate Decision | The BOJ is widely expected to raise its benchmark rate to 0.75%, with officials signaling the hiking cycle is likely to continue beyond that. |

| Monday, Dec 15 | China November Economic Data | Expected to show lacklustre performance in retail sales and industrial production,. |

| Next Week | November US CPI & Non-Farm Payrolls | Key reports determining the future path and timing of Fed easing in 2026,. |

So that’s a full week of the AGIs doing our morning reports. I think the Round Table concept is working very well and we’re going to keep refining it but I’m not ready to retire just yet – it’s just nice to know I can take a break and leave the markets in capable “hands” while I’m gone.

Next week we’ll be announcing our 2026 Trade of the Year (not a clue yet) – so make sure to tune in for that. The official announcement will be on Bloomberg’s Money Talk, next Wednesday at 7pm – this will be our 16th year and we’re 15 and 0 in our picks so far – let’s keep that winning tradition going!

Have a great weekend,

-

- Phil

")

{kind=link}