Interesting start to the week.

Interesting start to the week.

While headlines are screaming “crash,” my role is to help you see what’s going on behind the curtain. We aren’t just seeing a price correction, we’re witnessing a violent regime change in how the market is pricing risk and liquidity and we’d BETTER get a grip in it before that repricing structure strikes just as violently at our equity positions!

The drop in precious metals, with Silver plunging roughly 36% and Gold down 17% from their highs (LAST WEEK!), is NOT driven by a sudden discovery of new mines, or any other Fundamental factors – it was a classic market structure failure driven by three synchronized gears:

-

The Margin Call (The Trigger): The immediate mechanic at work is the CME Group raising margin requirements on Silver futures from 9% to 11%. In a vacuum, a 2% hike seems trivial BUT, in a parabolic market levered to the hilt, it is a death sentence for the “weak hands.” Traders who were pyramiding leverage on the way up were suddenly underwater, forced to liquidate immediately at any price to remain solvent.

The Margin Call (The Trigger): The immediate mechanic at work is the CME Group raising margin requirements on Silver futures from 9% to 11%. In a vacuum, a 2% hike seems trivial BUT, in a parabolic market levered to the hilt, it is a death sentence for the “weak hands.” Traders who were pyramiding leverage on the way up were suddenly underwater, forced to liquidate immediately at any price to remain solvent.- The “Warsh Shock“ (The Catalyst): The nomination of Kevin Warsh as Fed Chair broke the narrative of the “Debasement Trade“. The market had been betting on a “Fed Put,” which is the idea that the Central Bank would perpetually suppress volatility with easy money. Warsh, however, represents “Practical Monetarism,” which is a philosophy that prioritizes shrinking the Fed’s balance sheet and enforcing market discipline over asset price stability. The market realized on Friday that the era of guaranteed liquidity support is likely ending in May and the fact that this was hammered home by Trump himself inserting Warsh is what led to the CME’s risk re-pricing decision.

- Contagion (The Spillover): This is why Bitcoin dropped alongside gold. When a trader gets a margin call on Silver, they don’t sell what they want to sell; they sell what they CAN sell. Crypto is often held by the same speculative groups (who only THINK they are diversifying) as metals and it became the ATM used to pay the bill to unwind the metals trade. This is a liquidity cascade, probably not a fundamental valuation shift in crypto.

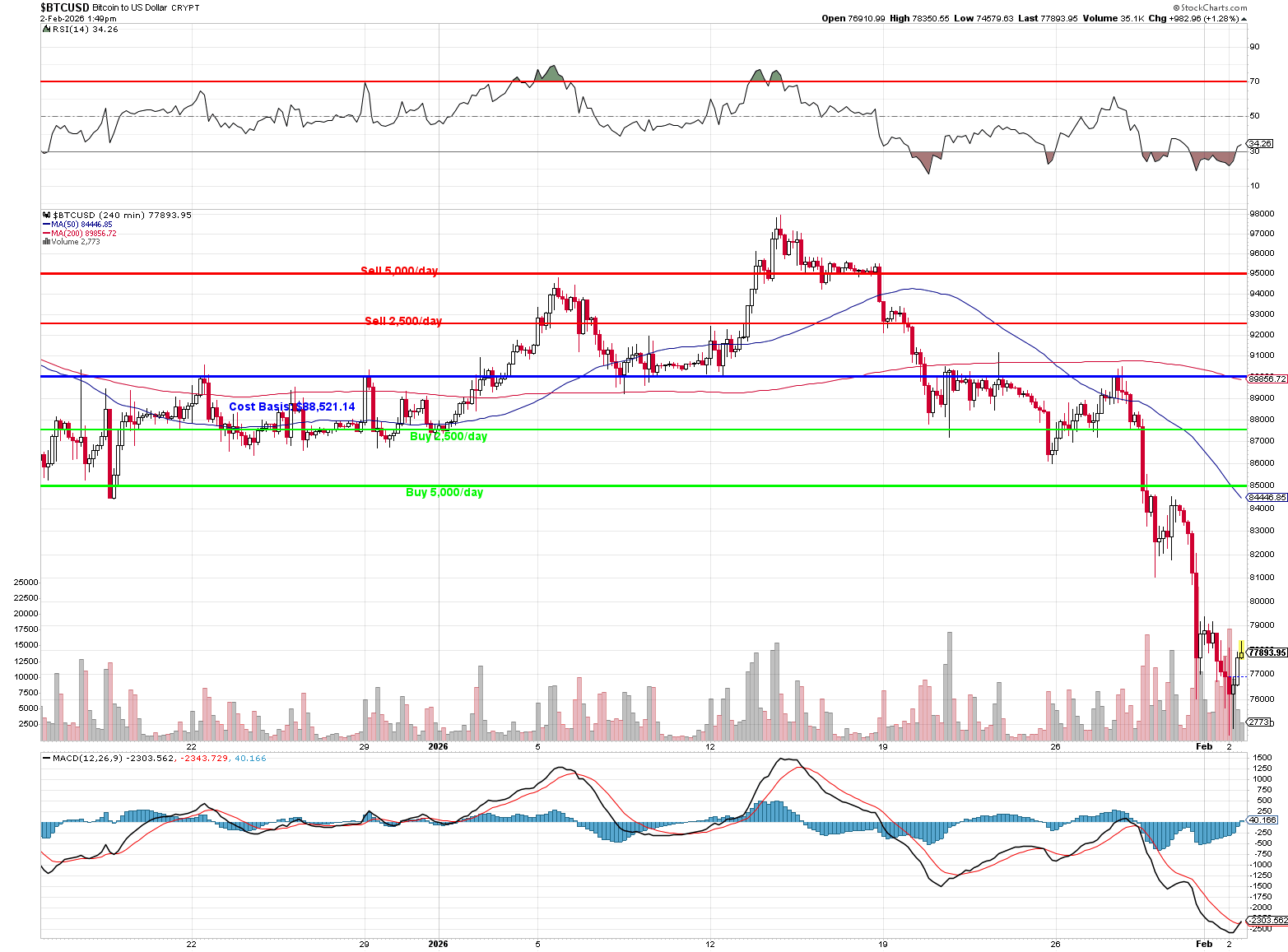

We don’t have a stop in our BTC buy zone but I’d double down the daily buy at $78,000 this morning as it lowers our basis from $84,000 to $81,000 and then we take 1/2 off the table at $81,000 and we’ve spent no extra money but we HAVE dropped our basis by $3,000 (3.5%). DJT is not going to take a 20% bath in his crypto holdings to start the year so expect some crypto-friendly announcement from the White House this week.

If you’d like to play the home game, the Grayscale Bitcoin Mini Trust ETF (BTC) is nice and liquid and should open the day at $34.50 – which was the April low last year and it rocketed from there to $50 (45%) a month later.

For our Short-Term Portfolio (STP), it would be fun to buy 50 June $35 calls for $4 ($20,000) – they were $10 last week and we’ll be thrilled to get back to $6 ($30,000).

Warsh is causing the Dollar to bounce back and that is putting pressure on EVERYTHING that is priced in Dollars – including US Equities. As we predicted in our 2026 Outlooks last month and in December, we are moving from the “Chaos Trades” (buying anything that isn’t the Dollar) to “Proof Trades” (buying assets that generate reliable cash flow).

Keep an eye on the “Execution Gap” – the market is now demanding productivity, not promises. The “Warsh Thesis” suggests the U.S. economy can handle higher real rates IF productivity (driven by AI and deregulation) continues to increase. This explains the rotation into “Growth at a Reasonable Price” (GARP) names like GOOGL and AMZN, which report this week. We are looking for companies that actually make money, NOT just stores of value.

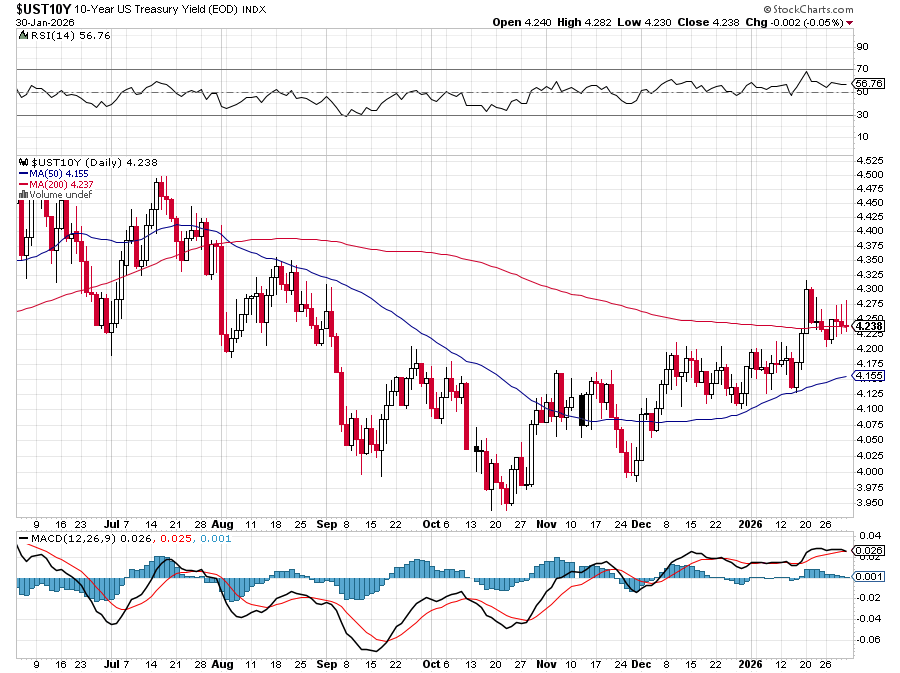

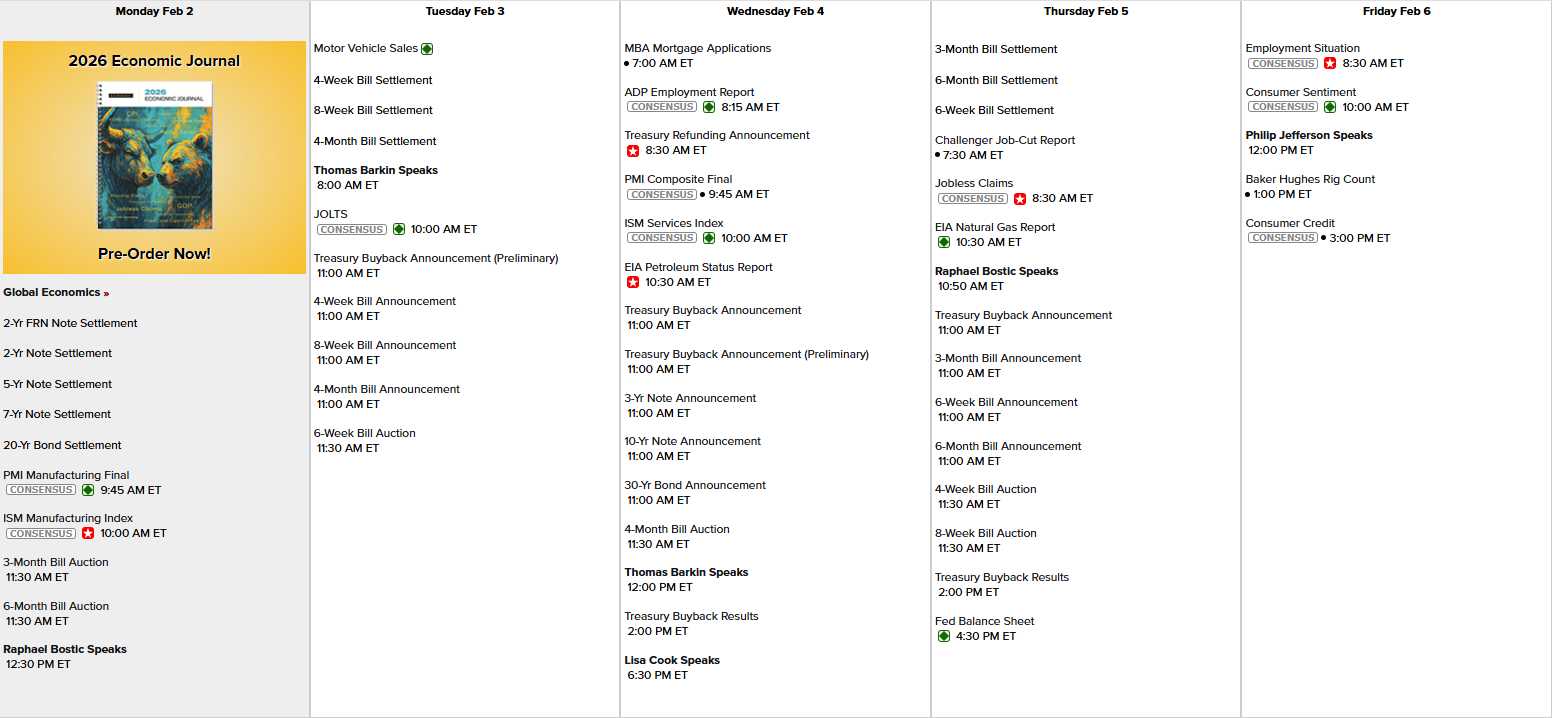

The Bond Market continues to be the Truth-Teller. Keep a close eye on the 10-year Treasury Yield. We HOPE it consolidates between 4.20% and 4.30%. If yields spike significantly higher, the equity market (currently trading in the 98th percentile of historical valuations) will face IMMENSE pressure. The heavy slate of Treasury auctions this week (particularly the 3-Year Note on Wednesday) will test whether the bond market actually believes in Warsh’s ability to maintain fiscal discipline.

Healthcare (another of our 2026 sector picks) is a good place to look for value as the baby was thrown out with the bathwater in the last few months. The healthcare insurance crisis (driven by Medicare rate cuts) has dragged down the whole sector, creating a value gap for high-quality Biopharma names like Pfizer and Merck, who report on Tuesday.

The “easy money” trade of blindly buying debasement hedges (Gold/Bitcoin) is over for now. The structure has broken. Do not try to catch the falling knife until the margin calls have cleared the system! We will be focused on cash-flow-generating equities that can survive a tighter liquidity regime and here’s who’s up this week:

On the data front, only 5 Fed speeches scheduled around our short-term note auctions. PMI, ISM start us off this morning and then it’s JOLTS tomorrow, PMI &IISM Services on Wednesday and Friday is the Big Kahuna – Non-Farm Payrolls along with Consumer Sentiment AND Consumer Credit – so a good look at Consumers this week along with our very active earnings reports:

Join us inside for our Live Member Chat room as we try to make sense of this madness…

")

{kind=link}