{kind=link}

Why Strait of Hormuz restrictions could have far-reaching impact

Money Talk, Bloomberg Business Network with Kim Parlee

With movement in the Strait of Hormuz being heavily restricted by Iran, are investors underestimating the true scale of the disruption? Phil Davis, Founder of philstockworld.com, breaks down why the impact could extend far beyond oil prices and how investors should be thinking about a prolonged period of uncertainty.

Timeline

0:00 – Intro / Hormuz focus & market implications

0:43 – Market underestimating impact

0:58 – Reframing “20% of global oil” narrative

1:05 – Global supply breakdown (Americas vs rest of world)

1:35 – True available global supply much smaller

2:08 – Effective impact and impact on import-dependent countries (Japan, India, Europe)

2:51 – Physical supply constraints & rerouting limits

3:07 – Supply depletion / strategic reserves drawdown and demand destruction (shutdowns, reduced usage)

3:38 – Real-world effects (factories shutting down, reduced operations)

4:06 – North America vs global impact

4:12 – U.S. as net exporter (refining & re-export dynamics)

4:44 – Force majeure / contract disruptions abroad

5:17 – Spot market spike (oil ~ $150 in Asia)

5:32 – What to watch (uncertainty, headline volatility)

5:48 – Second-order effects (shipping risk, insurance breakdown)

6:04 – Tanker risk (uninsurable, labor constraints)

6:39 – LNG bottlenecks / regional dislocations (negative gas pricing in Texas)

7:19 – Investor takeaway (move to cash, extreme uncertainty)

Stocks that may show some resilience as Middle East conflict continues

Phil Davis looks at specific sectors and companies that may provide a so-called “resilience trade” as conflict in the Middle East causes global chaos.

Timeline

0:00 – Intro / three stock buckets framework (reliable, critical, plumbing)

0:18 – Watchlist approach (100–200 stocks, looking for mispricing)

0:35 – War context shifting importance of sectors

0:47 – Reliable bucket concept (energy outside Strait of Hormuz, essential commodities)

1:00 – Plumbing concept (transport, financing, logistics resilience) and reliable bucket stocks (Exxon, Suncor, Canadian Natural)

1:45 – Suncor thesis (oil price leverage, strong earnings upside)

2:01 – Understated guidance due to war optics / market inefficiency

2:21 – Canadian Natural & Exxon positioning

2:44 – Critical bucket intro (LNG and metals)

2:54 – LNG bottlenecks (limited tankers, supply disruptions)

3:20 – Copper demand (AI/data centers, infrastructure buildout)

3:42 – Power grid limitations / need for localized generation

4:03 – Plumbing bucket intro (infrastructure & finance) and key names

4:18 – Role of financing in wartime (massive capital needs)

4:41 – Rebuilding demand / infrastructure beneficiaries

4:50 – Schlumberger as rebuilding play

5:04 – Summary of financing + pipeline plays

Two big trade ideas from Phil Davis

Phil breaks down two trade ideas, highlighting the opportunities and risks, while explaining his option strategies.

Timeline

0:00 – Intro / setup

0:03 – Trade framing (ETF hedge clarification)

0:13 – Hedge vs ETF explanation

0:24 – Prior quarter positioning problem (market rally hurting premium selling)

0:41 – Market pullback benefits / $70K gain (~8.2%)

0:55 – Goal: protect gains with hedge

1:03 – Introduction to SQQQ (3x inverse Nasdaq ETF)

1:19 – How SQQQ moves vs Nasdaq

1:31 – Trade structure (long 2028 $70 calls)

1:39 – Short 2028 $100 calls

1:46 – Selling short-term June $80 calls for income

1:54 – Net cost (~$32.5K) vs $180K spread

2:00 – Upside mechanics if Nasdaq drops

2:13 – Small market drop → large hedge payoff

2:27 – Use of short calls to generate ongoing income

2:35 – Rolling/recurring premium sales strategy

2:53 – “Free insurance” concept

3:04 – Defined risk (~$32K max loss)

3:10 – Limited upside risk with proper stops

3:25 – Importance of hedging / portfolio protection

3:33 – Transition to second trade

3:38 – Suncor trade introduction (watchlist idea)

3:47 – Oil thesis / profitability at higher prices

3:56 – Contract pricing / delayed benefit from higher oil

4:18 – Long-term bullish outlook

4:24 – Selling 2028 $60 puts (willing to own shares)

4:33 – Buying 2028 $60 calls and selling 2028 $75 calls (spread structure)

4:47 – In-the-money vs out-of-the-money explanation

4:59 – Premium offset / creating low-cost spread

5:06 – Income layer: selling June $65 calls

5:14 – Selling June $60 puts (balanced short positions)

5:27 – Trade economics (~$3K cost, large upside potential)

5:37 – Upside potential (~881%)

5:45 – Main risk: assignment at $60

5:53 – Comfortable owning shares long-term

6:00 – Capital requirement / assignment explanation and margin considerations

6:14 – Adjustment strategies (rolling, selling calls) and downside mitigation tactics

6:28 – Wrap-up / reminder to do own research

Trades

Transcripts

Why Strait of Hormuz restrictions could have far-reaching impact

As the conflict in the Middle East continues, a key focus for markets remains the Strait of Hormuz and whether it stays open or becomes effectively closed. About 20% of the world’s oil shipments pass through that area, and Iran is heavily restricting its use. That has major implications for energy prices, inflation, and global growth. The discussion turns to how investors should think about positioning in this environment, with Phil Davis offering his perspective. He argues that the market may be underestimating the real impact of the Hormuz disruption.

Phil pushes back on the commonly cited statistic that 20% of global oil supply is affected, saying that’s a misleading way to think about it. The Americas—particularly the U.S., Canada, Mexico, and Venezuela—produce over 20 million barrels per day, and much of that supply does not enter the global trade flow affected by Hormuz. When you adjust for that, and also consider that countries like China and Russia largely consume their own production, the amount of oil actually available to the global market is much smaller. In that context, losing access to roughly 20 million barrels through Hormuz represents closer to one-third of available global supply, not just 20%. That makes the disruption far more severe than headline numbers suggest.

The impact is especially acute for countries that rely heavily on imported oil, such as Japan, India, and parts of Europe. These countries are facing real physical constraints. While some oil is being rerouted, any portion that cannot be delivered is effectively lost to the system. This is not just a pricing issue—it’s a supply chain issue. Strategic reserves are being drawn down, which reduces future flexibility, and countries are being forced to conserve energy. In some cases, that means shutting down industrial activity for part of the week. This leads to demand destruction, but it also reflects how severe the supply shortage has become in certain regions.

In contrast, North America is less affected. The U.S. produces around 13 million barrels per day and imports a smaller additional amount, but it also exports roughly 5 million barrels per day of refined products. Much of what appears to be domestic consumption is actually oil being processed and then shipped abroad. Another important distinction is the use of force majeure in other parts of the world. In regions closer to the conflict, contracts are being voided because deliveries are no longer possible. That forces buyers into the spot market, where prices have surged—reaching around $150 per barrel in parts of Asia. North America, being geographically removed from the conflict, does not face the same level of contractual disruption.

Looking ahead, Phil emphasizes the importance of focusing on second-order effects. It’s not just about oil supply—it’s about the broader system reacting to risk. Shipping through the Strait of Hormuz has become extremely dangerous, and insurance companies are either charging exorbitant premiums or refusing to insure shipments altogether. Without insurance, ships cannot operate. Beyond that, there are practical constraints—crews may not be willing to take on the risk of traveling through a conflict zone. All of this further reduces the effective flow of energy.

These disruptions are also creating unusual regional imbalances. For example, liquefied natural gas shipments are being delayed, leading to oversupply in some areas and shortages in others. In parts of Texas, natural gas prices have even turned negative because there is nowhere to store it, while in places like Japan, buyers are willing to pay extremely high prices. This highlights how geography and logistics—not just supply and demand in aggregate—are driving outcomes.

Given all of this uncertainty, Phil’s conclusion is straightforward: investors need to recognize how difficult it is to interpret events in real time. Information is inconsistent, narratives shift quickly, and the situation can change rapidly. In response, he has significantly reduced exposure and raised cash, arguing that the level of uncertainty and risk makes it extremely challenging to invest with confidence in the current environment.

Stocks that may show some resilience as Middle East conflict continues

The discussion shifts to a broader framework for thinking about stocks in the current environment, dividing them into three buckets: reliable, critical, and what Phil calls the “plumbing” of the system. These categories help organize a watchlist of roughly 100 to 200 stocks that are constantly monitored for opportunities, especially when prices become attractive for temporary or irrational reasons, such as earnings reactions.

As geopolitical tensions rise, particularly in a wartime context, certain sectors become more important. The “reliable” bucket includes essential resources that can be produced and delivered outside vulnerable chokepoints like the Strait of Hormuz. This includes oil and other key commodities like gas and metals—things that are fundamentally necessary to keep economies functioning. The “plumbing” refers to the systems that move and finance these resources, such as transportation networks, pipelines, and financial institutions. These tend to be resilient because, as long as they’re not physically disrupted, demand for their services increases—shipping rates, for example, can surge dramatically during disruptions.

Within the reliable bucket, companies like Exxon, Suncor, and Canadian Natural Resources stand out. Exxon is already a core holding, while Suncor is attractive due to its oil sands production, which becomes highly profitable at higher oil prices. If oil stays above $90, Suncor could significantly exceed earnings expectations. However, companies are often reluctant to raise guidance in these situations because it can appear insensitive to profit from conflict. As a result, analysts and algorithms may not fully reflect the upside, creating opportunity. Canadian Natural is in a similar position, having already optimized operations for lower oil prices, meaning higher prices flow directly to the bottom line.

The “critical” bucket focuses on key materials like liquefied natural gas and metals. LNG faces logistical bottlenecks because there are relatively few specialized tankers. If even a portion of them are stuck or disrupted, a large share of global transport capacity is effectively removed. On the metals side, copper is highlighted as essential for building out infrastructure, especially for AI data centers and power systems. The demand for copper is expected to surge as more energy capacity and computing infrastructure are built. There’s also a growing constraint in the electrical grid itself, which is why new power generation is often being built directly next to data centers rather than relying on existing transmission networks.

Finally, the “plumbing” bucket includes infrastructure and financial players that keep everything connected and funded. Enterprise Products Partners represents the pipeline and transport side, while JPMorgan represents the financial backbone. War and reconstruction require enormous amounts of capital, and major banks play a central role in moving and allocating that money. At the same time, rebuilding damaged regions creates demand for infrastructure companies. Schlumberger is mentioned as a likely beneficiary, as it may be better positioned than competitors to take on rebuilding work in certain regions.

Taken together, the framework highlights a simple idea: in times of disruption, focus on what is essential, what is constrained, and what enables the system to function. Those are the areas where demand—and often profitability—tends to concentrate.

Two Big Trade Ideas (Hedge + Suncor Trade)

We’re speaking with Phil Davis about a couple of trades, starting with what was initially described as an ETF but is really being used as a hedge. He clarifies that while it is still an ETF, the key point is its purpose—this trade is about protection. In the prior quarter, the main issue was that the market had run up too much, which hurt their short-term premium selling. They were essentially pushed into a corner by stocks that kept rallying. But when the market pulled back, it actually helped, and the portfolio made about $70,000, roughly an 8.2% gain for the quarter, which he notes is strong given the messy market environment.

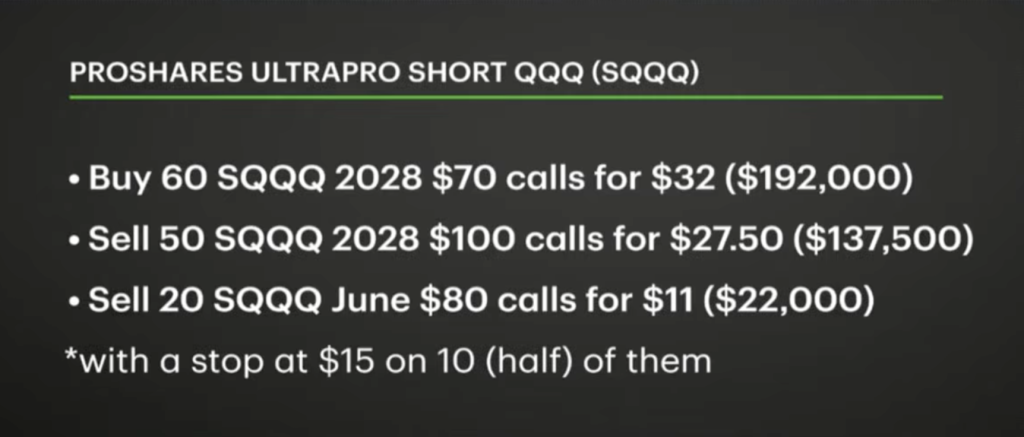

Now the focus shifts to protecting those gains. The hedge uses the ProShares UltraPro Short QQQ ETF (SQQQ), a three-times inverse ETF on the Nasdaq. In simple terms, if the Nasdaq falls 1%, SQQQ is designed to rise about 3%, though there are nuances like decay over time. The structure of the trade involves buying 60 long-dated 2028 $70 calls, selling 50 of the 2028 $100 calls, and also selling 20 short-term June $80 calls for income. This brings the net cost of the position to about $32,500, while the total spread has a potential value of $180,000.

The logic is that even a modest drop in the Nasdaq—say 10%—could push SQQQ up significantly, potentially into the 90s, meaning the position would quickly move into profitability. What makes this particularly attractive is the income component: the short-term calls being sold can be rolled repeatedly. If they expire worthless, they can be sold again month after month, generating income that effectively pays for the hedge over time. That’s why he describes it as “free insurance”—the premium collected offsets the initial cost.

The risk is clearly defined. The worst-case scenario is losing the $32,000 invested, since there are no short puts or unlimited-risk components. With proper stop management on the short calls, the risk of being hurt by a market rally is minimal because the long positions outweigh the shorts. The broader takeaway is that having hedges in place allows investors to sleep better, especially in uncertain markets.

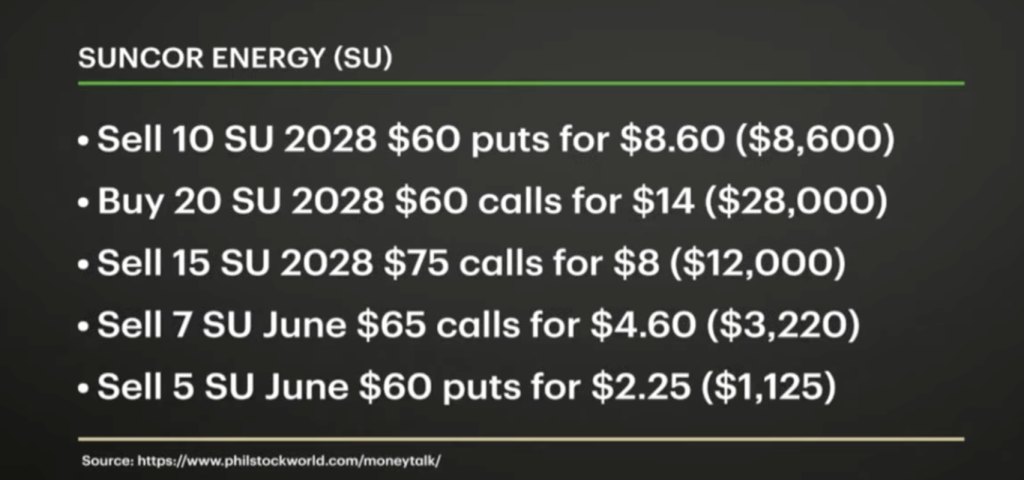

The second trade focuses on Suncor. The underlying thesis is tied to oil prices. Suncor produces oil profitably even at lower prices, but if oil rises toward $90, earnings could surge. One complication is that much of their production is still locked into older contracts at lower prices, so the full benefit of higher oil prices comes with a lag. Still, over time, this should create a strong earnings tailwind.

The trade structure reflects a willingness to own the stock long term. It starts by selling 10 of the 2028 $60 puts, meaning the investor could be assigned shares at that level. At the same time, 20 of the 2028 $60 calls are purchased, and 15 of the 2028 $75 calls are sold, creating a call spread. Because the long calls are in the money and the short calls are out of the money, the premium collected helps offset the cost, resulting in a very low-cost—or even net credit—position.

On top of that, there’s an income layer: selling seven June $65 calls and five June $60 puts. These short positions are structured so they are unlikely to both be exercised at the same time, adding additional premium income. Altogether, the trade nets around $3,000 on a $30,000 spread, with roughly $26,000–$27,000 of upside potential, which translates to a very high percentage return if things go right.

The main risk is assignment—ending up owning 1,500 shares of Suncor at $60. However, this is seen as acceptable because it’s a price they are comfortable owning the stock for the long term. From a capital perspective, in a margin account, the actual cash required may be closer to half that amount. And if the trade moves against you, there are multiple ways to adjust—rolling positions, selling calls, or otherwise managing the exposure. The key idea is that even in downside scenarios, there are tools to mitigate risk.