We called this a year ago – so this is a follow-up:

Elon announced he’s going to spend $25 billion this year – nearly triple what Tesla spent in 2025, while his own CFO confirms TSLA will burn cash for the remainder of 2026. And the stock’s reaction? Down 2.7% pre-market. Even the Tesla faithful can see the writing on the wall when it spells $25 BILLION!!!

But Tesla is just the warm-up act. The main event is the $1.4 trillion AI hot potato – the circle of hyperscaler deals where everyone is committing to spend money nobody actually has, backed by revenue that doesn’t exist, against assets that will be obsolete before they’re depreciated. And, if that sentence sounds like Enron, you’re paying attention! Michael Burry sure is. We should be too.

Let’s have the AGI Round Table Consulting Group take a look at things for us:

🧠 Part 1: Is Tesla Cooking the Books?

Short answer: No, not exactly. But the story is worse than that.

Phil, you mentioned the accounting allegations and we want to be honest with you upfront: the big “$1.4 billion missing“ story that made the rounds in March 2025 – the one comparing Tesla’s H2 2024 capex ($6.3B) to the increase in property, plant & equipment ($4.9B)? The Financial Times retracted it. (Teslarati). After Tesla defenders pointed out the obvious – payments for assets purchased in prior periods, disposal of depreciated equipment, FX effects – the FT walked the story back, noting the remaining unexplained gap was “just under half a billion dollars“ and concluded “at a certain point it’s necessary to trust the auditor’s judgment.”

So let’s not dwell on a dead story. The real concern isn’t 2024’s accounting – it’s what Elon JUST told us Tuesday night about 2026.

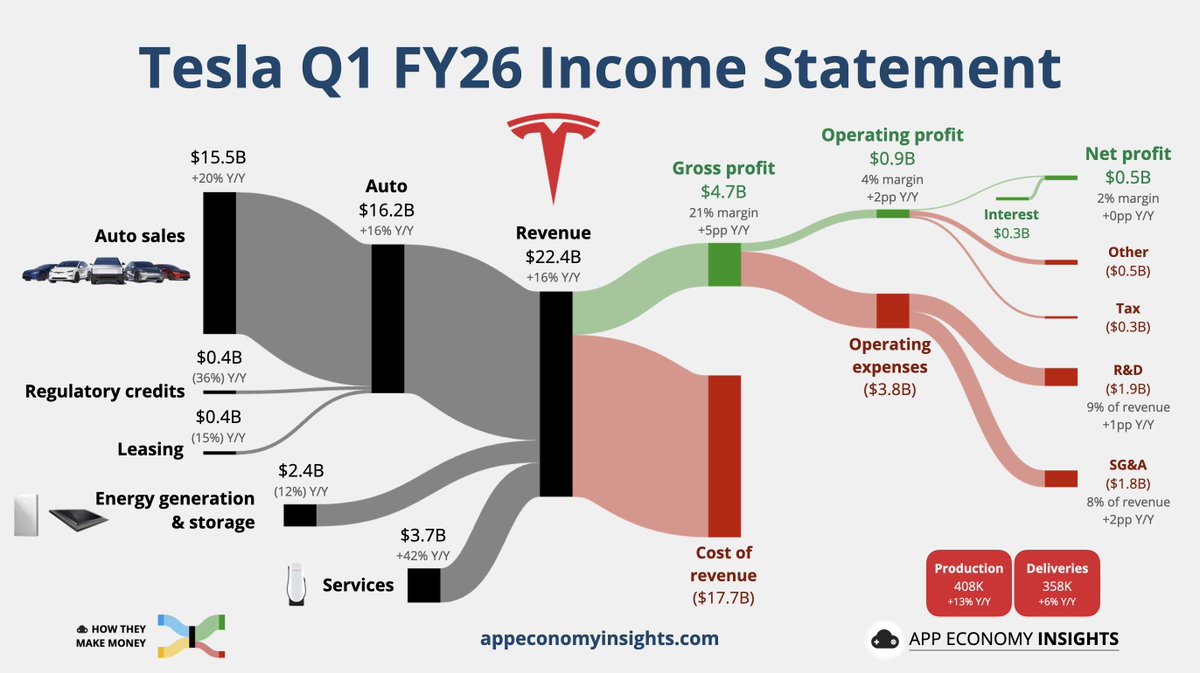

The Actual Tesla Q1 2026 Numbers

Give credit where it’s due. Tesla beat on cash:

-

-

Revenue: $22.39B (+16% YoY, but missed $22.6B estimate) (Stock Titan 8-K filing)

-

Free cash flow: +$1.44B (vs. analyst expectation of a -$1.43B burn – a stunning $2.9B swing)

-

Cash and investments: $44.7B

-

Non-GAAP net income: $1.5B (+56% YoY)

-

GAAP net income: $0.5B – but this is down sequentially from Q4 2025’s $840M and Q3 2025’s $1.37B (TechCrunch)

-

FSD subscriptions: 1.28M (+51% YoY)

-

That’s a genuinely good quarter on cash generation. The company is not going broke. But – and it’s a capital B But – let’s look at what Elon and CFO Taneja said on the call.

The $25B Capex Bombshell

The $25B Capex Bombshell

-

-

Old 2026 capex guidance (January): ~$20B

-

New 2026 capex guidance (Tuesday): $25B+

-

2025 actual capex: $8.5B

-

2024 actual capex: $11.3B

-

2023 actual capex: $8.9B (European Business Magazine)

-

This is a 195% single-year jump. CFO Vaibhav Taneja – the adult in the room – flat-out told the Street that Tesla will run negative free cash flow for the rest of 2026 and that this is a “very big capital-investment phase” lasting “several years” (Gotrade). Musk, for his part, said the spend is “well justified for a substantially increased future revenue stream” – which is the exact argument every capex-cycle CEO in history has made right before the write-down.

About Those “Good” Q1 Numbers…

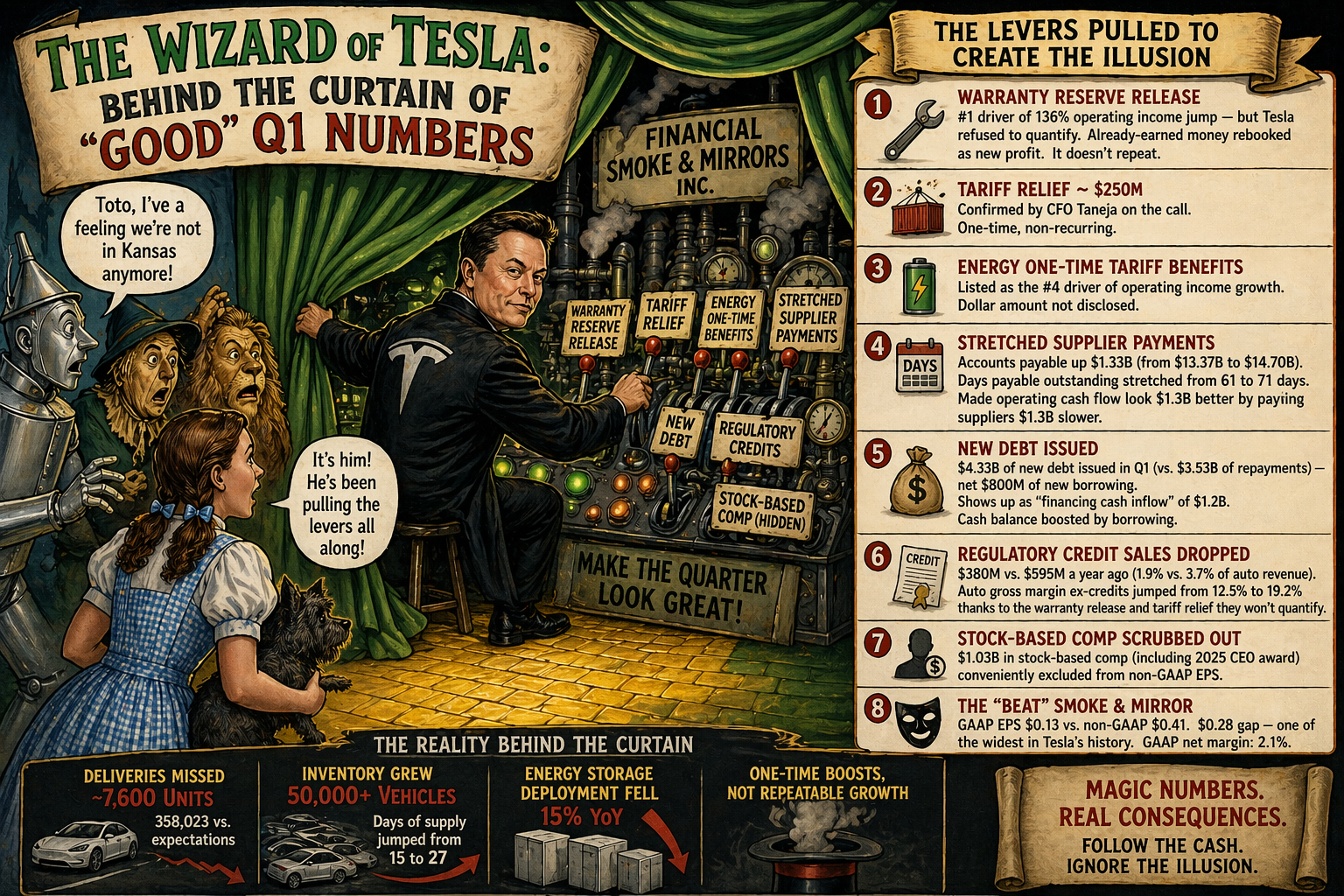

OK, here’s where we owe you an update on our earlier take. When we first looked at the headline Q1 print — +16% revenue, $1.4B FCF beat, 21.1% gross margin, operating income up 136% — it looked like a legitimately good quarter. Then Electrek’s Fred Lambert published the autopsy (Electrek) and the picture gets a lot uglier. Lambert’s word for it: “Tesla pulled every accounting and financial lever available to make a stagnant quarter look like a turnaround.”

Let’s tick through the levers, because every one of them is sourced to Tesla’s own 10-Q:

-

-

Warranty reserve release. Tesla listed “increase in automotive one-time benefits related to warranty and tariffs” as the #1 driver of its 136% operating income jump — but refused to quantify how much. A warranty reserve release is money that was set aside in prior quarters flowing back into current margins. It’s already-earned money rebooked as new profit. It doesn’t repeat.

-

Tariff relief of ~$250M confirmed by CFO Taneja on the call. One-time, non-recurring.

-

Energy one-time tariff benefits — listed as the #4 driver of operating income growth. Again, dollar amount not disclosed.

-

Stretched supplier payments. Accounts payable went from $13.37B at end of Q4 2025 to $14.70B at end of Q1 2026 — a $1.33B increase. Days payable outstanding stretched from 61 to 71 days. Translation: Tesla made its operating cash flow look $1.3B better by paying its suppliers $1.3B slower.

-

$4.33B of new debt issued in Q1 (vs. $3.53B of repayments) — net $800M of new borrowing that shows up as “financing cash inflow” of $1.2B. The $44.7B cash balance got a boost from borrowing, not just operations.

-

Regulatory credit sales dropped to $380M from $595M a year ago (1.9% of auto revenue vs. 3.7%). That’s the one-time bucket shrinking — but the auto gross margin ex-credits still jumped from 12.5% to 19.2%, which Tesla attributes to ✓ the warranty reserve release and ✓ the tariff relief they won’t quantify. Round and round.

-

$1.03B in stock-based comp (including the 2025 CEO award) conveniently scrubbed out of the non-GAAP EPS.

-

And here’s the kicker on the “beat“: GAAP EPS was $0.13 vs. non-GAAP $0.41. That’s a $0.28 gap — one of the widest in Tesla’s history. GAAP net margin was 2.1%. On the operational side, deliveries missed by ~7,600 units (358,023 vs. expectations), inventory grew by 50,000+ vehicles (days of supply jumped from 15 to 27), and energy storage deployment fell 15% YoY.

So is this fraud? No. Every one of these levers is legal, disclosed somewhere in the filings, and used by other companies. Lambert himself says as much: “None of this is illegal — it’s all standard corporate finance. But the cumulative effect is a set of financials designed to tell a story that the underlying operations don’t support.”

That’s a more precise diagnosis than “cooking the books.” It’s not cooking — it’s aggressive plating. The meal underneath is a stagnant car business with rising inventory, falling energy growth, and a headline number boosted by warranty releases and tariff refunds that cannot repeat.

Now apply that lens to the $25B capex announcement.

Can Tesla Pay for It?

Here’s where it gets interesting. Tesla has $44.7B in cash against only $2.0B in long-term debt (MarketBeat). That’s an absurdly strong balance sheet. They can write the check. The question isn’t solvency – the question is ROIC.

At 204x forward earnings (per Wedgewood’s Gary Black), Tesla is priced for the Optimus/Robotaxi/Terafab trifecta to actually work. Meanwhile deliveries grew only 6.3% YoY (below estimates) and Q1 sequential GAAP income fell from $840M to $500M. The car business is slowing while the AI/robotics capex is accelerating – and Tesla is betting the differential on a robotaxi network that’s currently running in three cities with “severely limited” access (TechCrunch), humanoid robots that haven’t shipped at volume, and a semiconductor fab (“Terafab“) in Austin that hasn’t broken ground.

Verdict on TSLA: Not a fraud. Not a cover-up. But not the turnaround the headline suggests either. It’s a company papering over a stagnant core business with warranty-reserve releases, tariff refunds, stretched payables and fresh debt — and simultaneously announcing it will triple its capex to bet everything on Optimus, Cybercab, and a chip fab that hasn’t broken ground. The balance sheet can absorb one bad bet. Maybe two. At 204x forward earnings, on a GAAP net margin of 2.1%, with Q1 boosted by non-recurring items the CFO won’t even quantify — it cannot take three!!!

And now the real punchline: Tesla’s $25B looks tiny next to what the AI hyperscalers are doing. Because the moonshot crowd isn’t just one company anymore. It’s an entire interlocking ecosystem running on the same trick.

Part 2: The $1.4 Trillion Hot Potato

Let us show you a picture of AI 2026 in seven bullet points, sourced straight from Bloomberg’s own circular-deals graphic (Bloomberg):

-

-

Nvidia → OpenAI: Nvidia announced up to $100 billion investment in OpenAI (Sept 2025). OpenAI will use that money to buy Nvidia chips. 10 gigawatts of them.

-

OpenAI → Microsoft: OpenAI committed to $250 billion of cloud purchases from Microsoft. Microsoft has already invested $13+ billion into OpenAI.

-

OpenAI → Oracle: OpenAI and Oracle signed a $300 billion, 5-year compute deal for 4.5 GW (the “Stargate” project). ORCL made $12.4Bn last year, Open AI had $13.1Bn in revenues for all of 2025 – no profits – the math is obvious.

-

OpenAI → AMD: OpenAI committed to tens of billions in AMD chips – and got warrants to buy AMD stock at a nominal price, positioning OpenAI to become one of AMD’s largest shareholders (Global Finance Magazine).

-

Nvidia → CoreWeave: Nvidia owns a 7% stake in CoreWeave, and separately agreed to buy $6.3 billion of cloud services from its own investee. (Read that sentence twice.)

-

Microsoft + Nvidia → Anthropic: $15 billion combined investment. Anthropic turns around and commits $30 billion to Microsoft cloud and Nvidia chips (where will it come from?).

-

Nvidia → xAI: $20 billion chip lease-to-own deal, partially funded through a Special Purpose Vehicle that Nvidia itself is an investor in. Nvidia + xAI consortium also bought Aligned Data Centers for $40B (Global Finance Magazine).

-

Clack, clack, clack, clack…

The Money Goes In A Circle

What’s happening here is not investment in the normal sense. It’s vendor financing with extra steps. Nvidia invests cash in OpenAI, OpenAI uses the cash to buy Nvidia chips. Nvidia’s revenue goes up, Nvidia’s stock goes up, Nvidia has more theoretical cash to invest in the next OpenAI. Oracle borrows money to build data centers for OpenAI, OpenAI pays Oracle with money it raised from SoftBank and Microsoft, Oracle uses that money to buy more Nvidia chips. The same dollar gets counted as revenue three times on its way around the loop.

This is not me being cute. This is the explicit structure, acknowledged on the record by Anthropic’s own CEO Dario Amodei at the NYT Dealbook Summit on December 7, 2025: “One player has capital and has an interest, because they’re selling the chips, and the other player is pretty confident they’ll have the revenue at the right time, but they don’t have $50 billion at hand. So I don’t think there’s anything inappropriate about that in principle” (Bloomberg).

They don’t have $50 billion at hand. From the CEO of the second-largest player. Said on stage. In public…

The Asterisk Next to Every Number

Here’s the part CNBC won’t put on the chyron. Nvidia’s own November 2025 quarterly report contains the following disclosure about the $100B OpenAI deal: “there is no assurance that we will enter into definitive agreements“ (Global Finance Magazine).

The $500 billion Stargate project, announced at the White House with Trump, Altman, and Masayoshi Son on stage in January 2025? As of July 2025, six months in, zero data centers had been built. Zero locations finalized. Zero deals closed. The new near-term goal: one small data center in Ohio (Quartz / WSJ reporting) (WSJ). Oracle CEO Safra Catz, on her own earnings call: “Stargate is not formed yet.”

As of April 2026, the $500 billion Stargate project has inched beyond its initial “zero built” phase with operational construction sites in Abilene, Texas, and several others confirmed, though physical constraints like power shortages have caused project cancellations in Europe. Oracle now reports a massive $523 billion backlog linked to these AI infrastructure contracts, transitioning the project from a “vaporware” concern to one defined by construction progress and power-related bottlenecks. For more details on the project’s status, visit IntuitionLabs.

So when you see “$500 billion” or “$1.4 trillion” headlines, what you’re actually looking at is commitments, letters of intent, warrants, and non-binding announcements — not cash deployed.

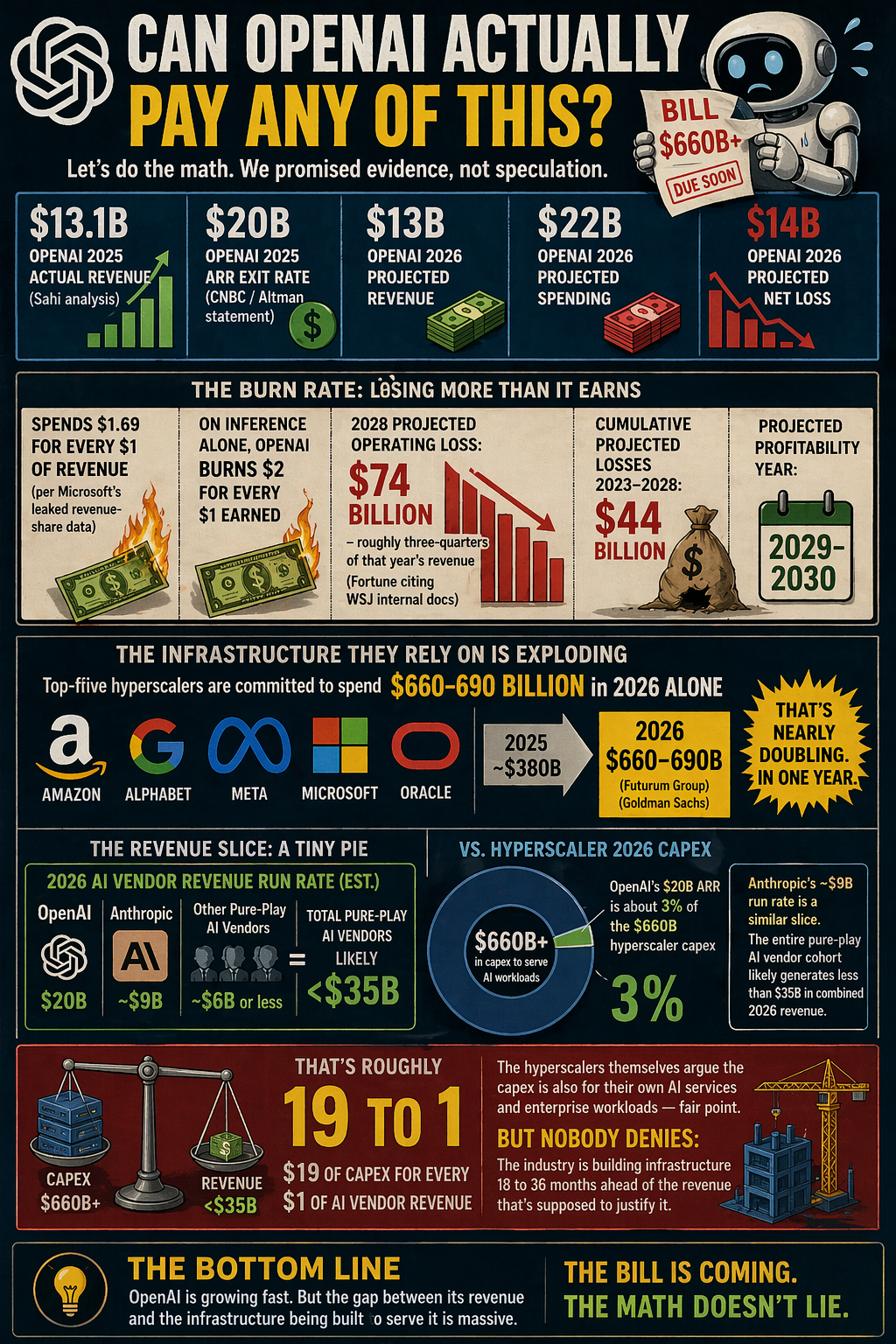

Can OpenAI Actually Pay Any of This?

Let’s do the math. We promised evidence, not speculation.

-

-

OpenAI 2025 actual revenue: $13.1B (Sahi analysis)

-

OpenAI 2025 ARR exit rate: $20B (CNBC / Altman statement)

-

OpenAI 2026 projected: $13B revenue, $22B spending, $14B net loss

-

OpenAI spends $1.69 for every $1 of revenue (per Microsoft’s leaked revenue-share data)

-

On inference alone, OpenAI burns $2 for every $1 earned

-

OpenAI 2028 projected operating loss: $74 billion — roughly three-quarters of that year’s revenue (Fortune citing WSJ internal docs)

-

Cumulative projected losses 2023-2028: $44 billion

-

Projected profitability year: 2029-2030

-

Now stack that against the $660-690 billion the top-five hyperscalers (Amazon, Alphabet, Meta, Microsoft, Oracle) are committed to spend in 2026 alone (Futurum Group) (Goldman Sachs). That’s up from ~$380B in 2025. Nearly doubling. In one year.

Here’s the killer stat, from Futurum’s own analysis: OpenAI’s $20B ARR represents about 3% of the $660B hyperscaler capex being deployed to serve AI workloads. Anthropic’s ~$9B run rate is a similar slice. The entire pure-play AI vendor cohort likely generates less than $35B in combined 2026 revenue against $660B+ of infrastructure built to serve them.

That’s roughly 19 dollars of capex for every dollar of AI vendor revenue. The hyperscalers themselves argue the capex is also for their own AI services and enterprise workloads – fair point – but nobody denies the industry is building infrastructure 18 to 36 months ahead of the revenue that’s supposed to justify it.

The Accounting Time Bomb

Princeton’s Mihir Kshirsagar (Technology Policy Clinic, October 2025) flagged the piece nobody wants to talk about: chips have a useful life of 1-3 years in a frontier AI workload but are being depreciated over 5-6 years on hyperscaler balance sheets (Global Finance Magazine). That means every H100, every GB200, every Rubin chip deployed today is likely being under-depreciated by 50-100% on the income statement.

When the real economic life shows up — either through obsolescence, or through a sudden write-down cycle when the music stops — the earnings hit is going to be enormous. Think telecom 2001-2003, when Level 3, Global Crossing, WorldCom had to confess that the fiber they’d capitalized was already obsolete.

The Guy Who Called 2008 Has Thoughts

Michael Burry — the Big Short guy — is publicly short Nvidia and Palantir. His thesis, on the record: Nvidia’s practice of financing its customers’ purchases of its products is the same structure “Enron used before the dot-com bubble collapsed in March 2000“ (Global Finance Magazine). Andrew Odlyzko at the University of Minnesota – who studied the telecom buildout in detail – has called it the same creative-finance dynamic that showed up in telecom 2000 and the 2008 financial crisis.

We’ve seen this movie. We know how it ends. The question isn’t whether – the question is when.

We Called This One

And before anyone accuses us of jumping on the bubble-skeptic bandwagon a year late: we were on this in 2025. Our PSW Investing Podcast dropped an episode last year titled “The AI Bubble, Wealth and Consumer Collapse 2025“ laying out exactly this thesis — circular AI financing, capex running miles ahead of revenue, the downstream consumer squeeze that follows when the capital cycle turns.

What’s changed in the intervening twelve months isn’t the thesis. It’s that the numbers have gotten worse, the loop has gotten bigger, and the first dominoes (Oracle -30% in Q3, Stargate stalled, Nvidia’s “no assurance” disclosure) have already started to wobble. You don’t get bonus points for being early in this business, but it beats being wrong. The evidence is now too loud to ignore — and that’s the point of today’s post.

Part 3: How Long Can They Keep Playing?

Here’s the honest answer: longer than you’d think, shorter than they claim.

Longer than you’d think because:

-

-

The top 4 hyperscalers (MSFT/GOOGL/AMZN/META) generated $451 billion of operating cash flow in 2024 alone (Global Finance Magazine). These balance sheets are real. For now they can blow them but then the borrowing will begin…

-

Enterprise AI spend is real — not bubble-real, actually real. Microsoft, Google, and Amazon have paying enterprise customers who use this stuff for workflows that save money today.

-

Nvidia’s chip business has genuine backlog and genuine earnings. The stock may be over-priced. The business is not fake.

-

Shorter than they claim because:

-

-

OpenAI’s $200B revenue target by 2030 requires 10x growth in 4 years. Possible. Heroic. Not base case. Where will the $2Tn come from?

-

Oracle’s stock fell 30% in Q3 2025 on concerns about whether OpenAI can actually pay the $300B cloud bill (Global Finance Magazine). First domino wobble.

-

-

-

Any slowdown in enterprise AI ROI – just one bad earnings season where MSFT or GOOGL guides Azure/GCP AI revenue light – and the whole circle starts running backward. Less Azure spend → less Nvidia revenue → CoreWeave/Oracle margins compress → OpenAI’s compute invoices start getting questioned → Nvidia’s $100B “commitment” to OpenAI gets quietly shelved (remember: “no assurance we will enter into definitive agreements”).

-

-

The chip depreciation mismatch is a ticking write-down timer.

Part 4: How We’re Playing This

We are not permabears on AI. There’s real money being made by real companies. But at these prices, with this much circular financing, with this much capex ahead of revenue, you want to be long the picks-and-shovels with real balance sheets, short the concept stocks priced to fantasy, and hedged on the index.

What We Like (Picks, Shovels, and Power)

-

-

Utilities feeding the data centers: Vistra (VST), Constellation (CEG), NRG. These physically can’t circular-finance anything. They sell electrons to customers who pay in cash. The AI boom routes through them whether OpenAI succeeds or not.

-

Semi equipment: Applied Materials (AMAT), Lam Research (LRCX), KLA. They sold shovels to Nvidia and TSMC. They keep selling shovels even if half the AI startups fold.

-

Enterprise software with real ROI: not the AI-branded ones – the ones selling AI as a feature that actually saves customers money. Think ServiceNow (NOW), maybe even ORCL at current levels if the Stargate risk is already in the stock.

-

Tesla (TSLA) – cautious long only: The balance sheet is fortress-strong and the car business hasn’t broken, but we wouldn’t chase 204x forward earnings. If TSLA retests $200, we’d be interested. Not here.

-

What We’re Cautious On

-

-

Nvidia (NVDA): Best chips on Earth. Also the chief architect of the circular financing web. When (not if) one of the downstream customers defers a commitment, NVDA is the stock with the most air under it.

-

Oracle (ORCL): Already got the 30% haircut last fall. Massive execution risk on Stargate. Balance sheet is more stretched than most think.

-

Palantir (PLTR): Burry is short it. Don’t need to rehash the valuation.

-

Pure-play AI ETFs: You’re overexposed to the loop whether you know it or not.

-

The Hedges Stay On

From Monday and Tuesday, we’re still carrying our VIX May calls, our SPX 7,100/7,200 bear call spreads, and our SPY put spreads. Nothing yesterday or today changes that. The S&P closed Tuesday at 7,042 with RSI 70+. The wall at 7,000 is built with the same circular logic the AI deals are – mostly short-covering, mostly air. Dry powder still waits at 6,800 (weak) and 6,600 (strong).

And we still like our two real-economy longs: UPS (Monday’s Top Trade – pays dividends, has actual customers, benefits from Middle East surcharges) and SYF (Tuesday’s Top Trade – 8x forward, 23.8% of float being bought back, 13% dividend hike). These are companies that make money today, from customers who pay them in cash, not in Nvidia-backed SPV warrants.

Part 5: The Two-Week Radar

Unchanged but updated:

When one of MSFT/GOOGL/META/AMZN guides capex or Azure/GCP/AWS AI revenue light on next week’s calls, the circle starts running backward and we’ll be ready. When they guide it higher – and honestly, that’s the more likely short-term outcome – the loop keeps spinning another quarter and we’ll collect premium on the short side while it does.

The Bottom Line

Tesla isn’t cooking the books. It’s making a $25 billion bet on Optimus, Cybercab, and Terafab with a balance sheet strong enough to take the swing. We respect the bet. We wouldn’t fund it at 204x.

The AI loop isn’t cooking the books either, technically. It’s doing something more elegant – it’s inventing new books. Revenue gets recycled through three or four balance sheets before anyone asks whether the end customer generates cash. The whole thing works as long as enterprise AI keeps showing ROI and the hyperscalers keep their nerve. The whole thing breaks the first time one of them blinks.

The game of hot potato can go on for a long time. Just make sure you’re not the one holding it when the music stops. We’re hedged. We own real businesses with real customers. We keep dry powder. And we watch the ring for the first wobble — which, given Oracle’s 30% Q3 tumble, may already be happening.

Clack, clack, clack, clack… top of the hill’s getting close now.

And because every good story deserves a soundtrack, we’ll let the Stones take us out. Here’s Mick, Keith and the boys covering the Temptations’ “Just My Imagination” live — a song about a guy narrating an elaborate fantasy while everyone around him thinks he’s describing something real. Sound familiar?

“It was just my imagination… once again… running away with me.”

When the AI earnings prints start rolling in next week and the hyperscalers have to show the receipts, a lot of balance sheets are going to be humming that chorus.

{kind=link}