{kind=link}

SNX and WBA are both down 10% and even poor SCHN is down – and they did a nice job! WBA is a stock we have played in the past but it’s not in our current portfolios. Back at $28.50 this morning is getting interesting again so let’s see what’s going on:

Walgreens Boots Alliance (WBA) is valued at $25Bn at $29/share and last year they made $4.3Bn and this year and next they were supposed to make around $4Bn and that makes sense as Covid is winding down and they got some of that $11Tn in stimulus giving everyone shots and such for the last two years. That’s over – deal with it!

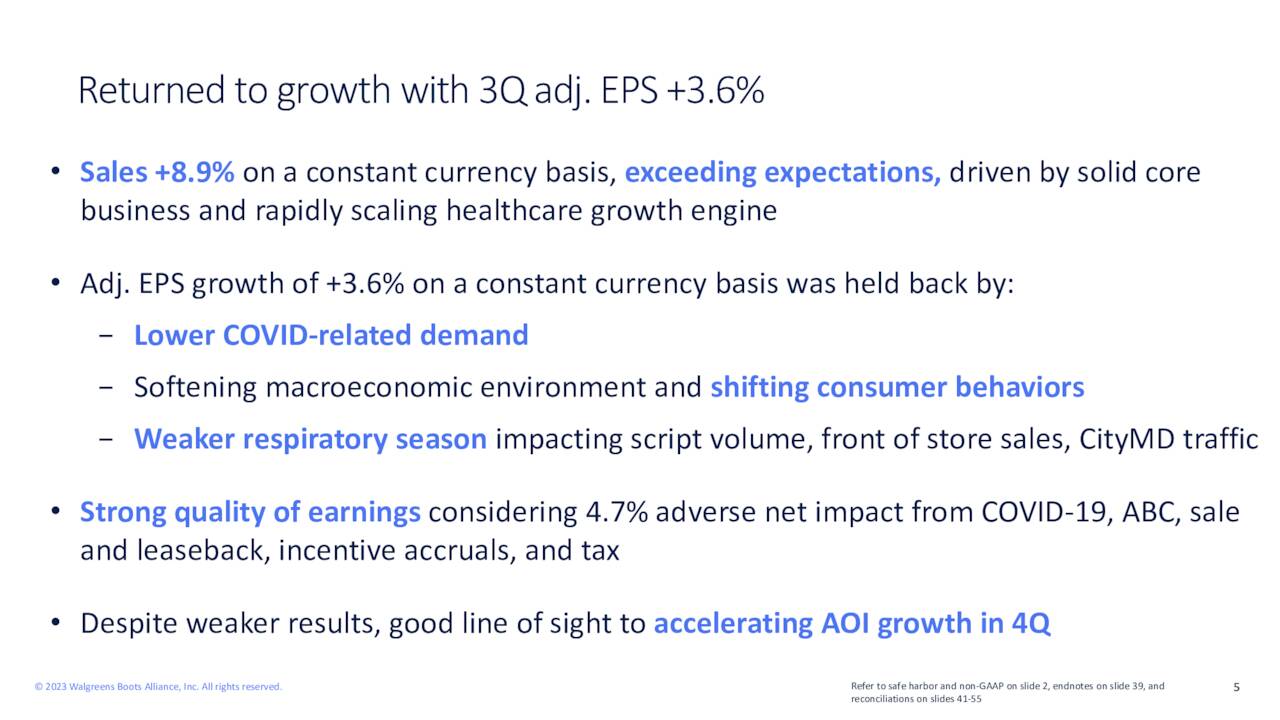

Nonetheless, top-line sales were $35.4Bn, which was up 9% from last year with more people out shopping with their newer HealthCare segment up 22% but margins dropped to 19% from 20.3% last year as WBA did only 800,000 Covid shots vs 4.7M a year ago.

Despite sales growth, “significantly lower demand for COVID-related services, a more cautious and value-driven consumer, and a recently weaker respiratory season created margin pressures in the quarter,” Chief Executive Rosalind Brewer said.

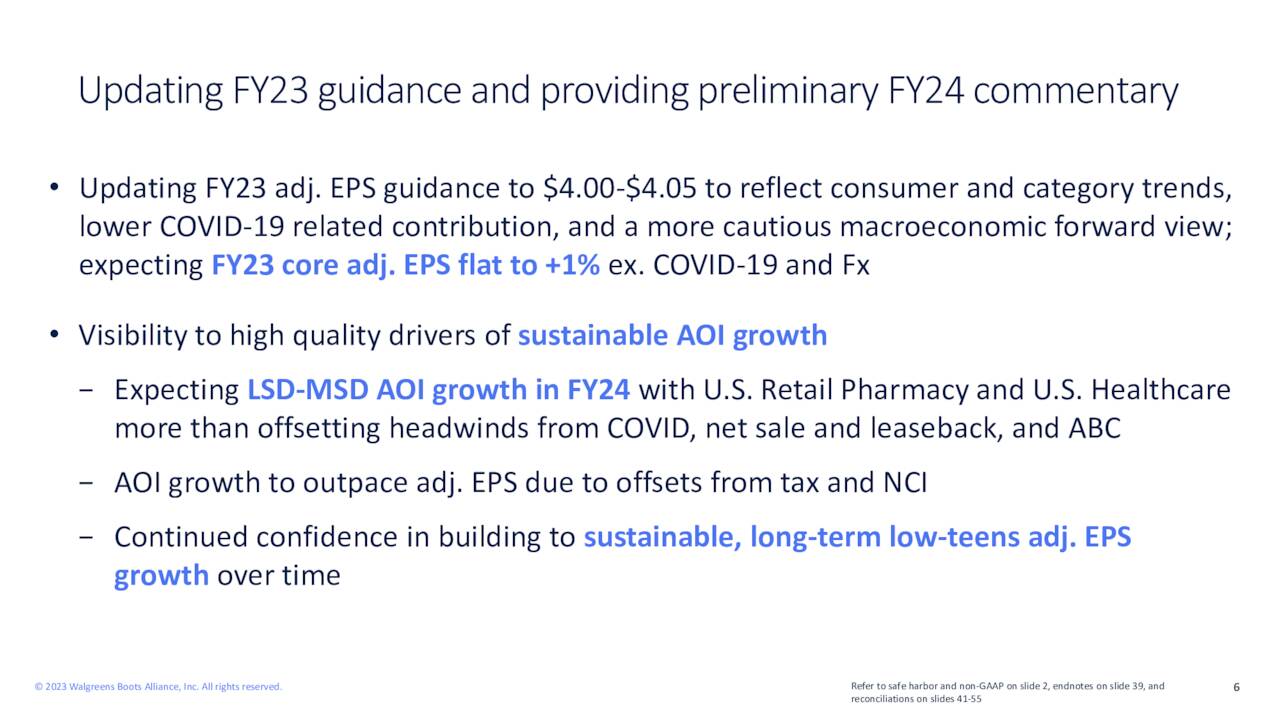

On the whole, WBA adjusted 2023 earnings expectations to $4-4.05 from $4.45-4.65 so a good 10% drop in expectations but $4 is still a 7.25 p/e – it’s insane to see people bailing out on this like they are going under. Yes, the Government is cracking down on Pharma pricing but WBA gets the same co-pays either way.

Here’s a few highlights from their Earnings Call Presentation:

Now, when you are reading these slides, you have to keep things in perspective. WBA has $140Bn in sales and drops 2.85% to the bottom line so when you hear that Village MD will grow from $150M to $200M in the next two years – you should yawn.