{kind=link}

Good morning!

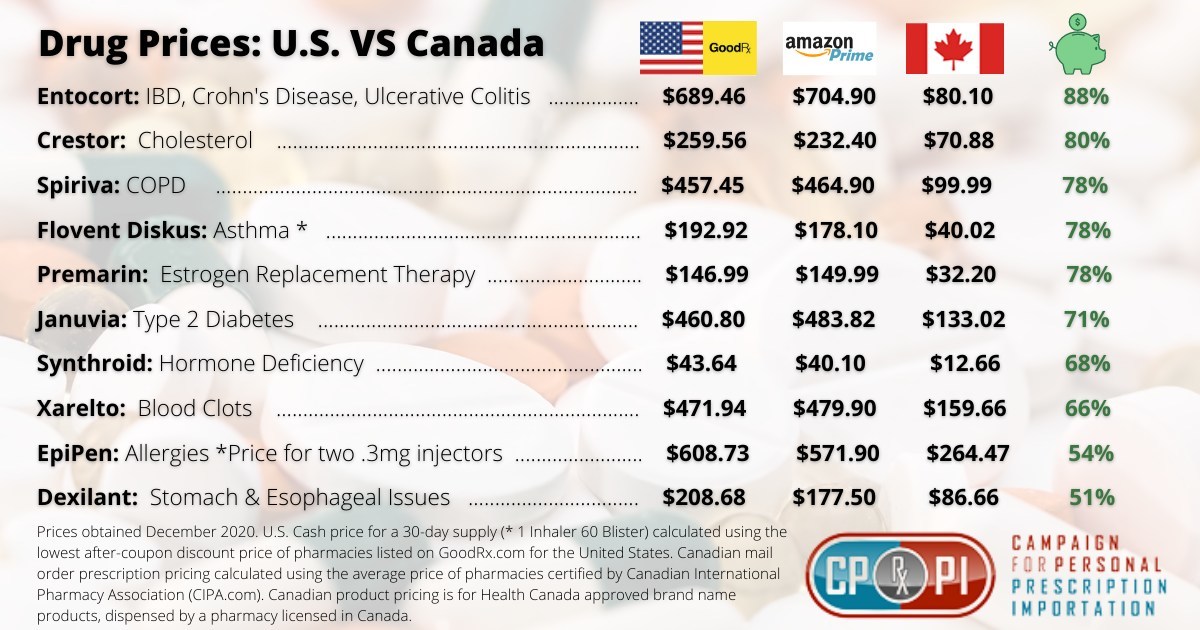

WBA/Yodi - You have Boots in Europe - have people stopped going? I guess that guy doesn't like them but he still went there to get his shot. Revenues and profits are back to 2019 levels, heading towards $4Bn per year and you can buy the whole company for $43Bn. Do you know who you buy drugs on-line from in the US? WBA! The big pharmacies are also the big on-line sellers.

And look how crazy this is:

Are they going to have huge growth? No. Can we make 300% on a spread that's better than 80% likely to pay off? Yes. So I like them.

You can sell 2024 $40 puts for $5 and that's net $35, which is $15 (30%) below the current price and would drop the PE down around 7 - so I consider that free money but, for a spread, I'd be more aggressive and sell the $50 puts:

- Sell 5 WBA 2024 $50 puts for $10 ($5,000)

- Buy 10 WBA 2024 $35 calls for $15.60 ($15,600)

- Sell 10 WBA 2024 $45 calls for $9.50 ($9,500)

That's net $1,100 on the $10,000 spread that's 100% in the money so start so all WBA has to do is not go lower and you make $8,900 (809%) in two years and that should cover your deductibles quite nicely. Break-even is way down at $41, so WBA can drop 20% before you are out of pocket and worst case is owning 500 shares at $41.10 but then you can roll to lower strikes further out.

So, you can keep hating on WBA all you want, Yodi, but I'm going to keep pointing out what an excellent value play they are.

Walgreens (WBA) has certainly earned its title as one of the dogs of the DOW, given its underperformance and high dividend yield compared to its peers in the index.