US Money Supply Figures: Dude, Where’s My (Monetary) Deflation?

Courtesy of JESSE’S CAFÉ AMÉRICAIN

As a review or refresher please read: Money Supply A Primer if you need to remind yourself what these money supply figures represent.

As a review or refresher please read: Money Supply A Primer if you need to remind yourself what these money supply figures represent.

Considering the high unemployment and sluggish GDP the fall off in year over year growth in the money supply figures is to be expected, especially after the bubbliciously high growth rates (11% and 16% respectively) just prior to the financial crisis. That is why one should look at both the nominal and the percent year over year charts.

There is certainly price deflation from slack aggregate demand fueled by stagnant wages and high unemployment, and it may get worse as the Fed and the government coddle their unreformed pet Banks, leaving the real economy and most Americans to twist in the wind. But there is no true monetary deflation yet, the kind which is supposed to stiffen the back of the dollar and all that.

There is also sufficient room for concern about the US dollar and its sustainability as the world’s reserve currency. This would be familiar to most economists as Triffin’s Dilemma. As the world shifts from the Bretton Woods II compromise to a less dollar specific regime the adjustment could be quite traumatic, especially to the financialization industry. Here is another description of the same phenomenon called the Seigniorage Curse. It is why I have called the US dollar and its associated bonds The Last Bubble.

"The Seigniorage Curse appears to hollow out the economy by the following manner: First, the premium charged to holders of dollars becomes a new source of accrued, aggregate revenue. This extra capital flowing into the economy is initially seen as a global honoring of our economy’s strength, and innovation. But when innovation falters and less value is created, seigniorage is maintained–and thus the unhealthy dynamic begins. From this point forward, whether the US economy either leads in innovation, or lags in innovation, the Dollar advantage grows regardless. It then becomes clear that manufacturing Dollars, rather than manufacturing goods, is a better value proposition. Once that dynamic is in place, then a long cycle of financialization ensues, in which innovation and talent moves from design and manufacturing to the financial sector. The financial sector then becomes rapacious, as it scours what’s left of the economy to monetize. Whereas manufacturing and innovation were once monetized, the financial sector begins to monetize itself…

Every inheritance starts out as a gift. Just as oil-cursed nations remain ever vulnerable to swings in the price of oil, the United States is now vulnerable to its own number one export–the value of the US Dollar and by extension the value of US Treasury Bonds."

True Money Supply is included for all you Austrian Economists, and it has enjoyed a bumper expansion under Bernanke’s chairmanship. This is the money that is ready and able to be used as a medium of exchange, what the Austrians consider ‘real money.’ I am quite sure that Messrs Ludwig and Murray would be aghast at Bernanke’s banking practices.

I include Eurodollars chart at the bottom. This is the ‘missing component’ from the M3 series. Several commentators seek to estimate M3 by obtaining the other M3 components from existing sources and then estimating eurdollars based on correlations and trending. See M3 Hysteria and a Look at M2, MZM, GDP and PPI.

The Eurodollar is a particularly interesting money measure to me be because of the two enormous dollar short squeezes which we have seen in Europe as customers demanded dollars based on dollar assets deposited in dodgy CDOs. It was on a parabolic trajectory BEFORE the squeezes, and one can only wonder where they are now.

I am still comfortable with my forecast for a severe stagflation, considering both a protracted monetary deflation and hyperinflation as less probable ‘on the tail’ events that almost certainly would reflect fiscal and monetary policy errors. What also concerns me is the failure to reform and address the grossly imbalanced economy. I am less confident today however, that Bernanke and the Congress will not make these errors because of the blind greed of the oligarchy and their influence over the country.

M2

M2 Year over Year Growth

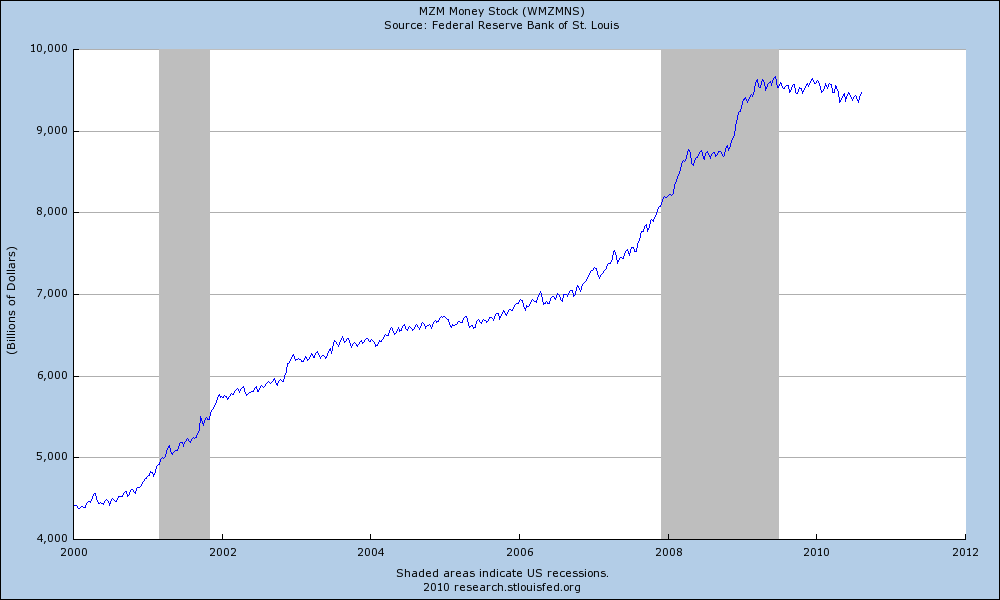

MZM

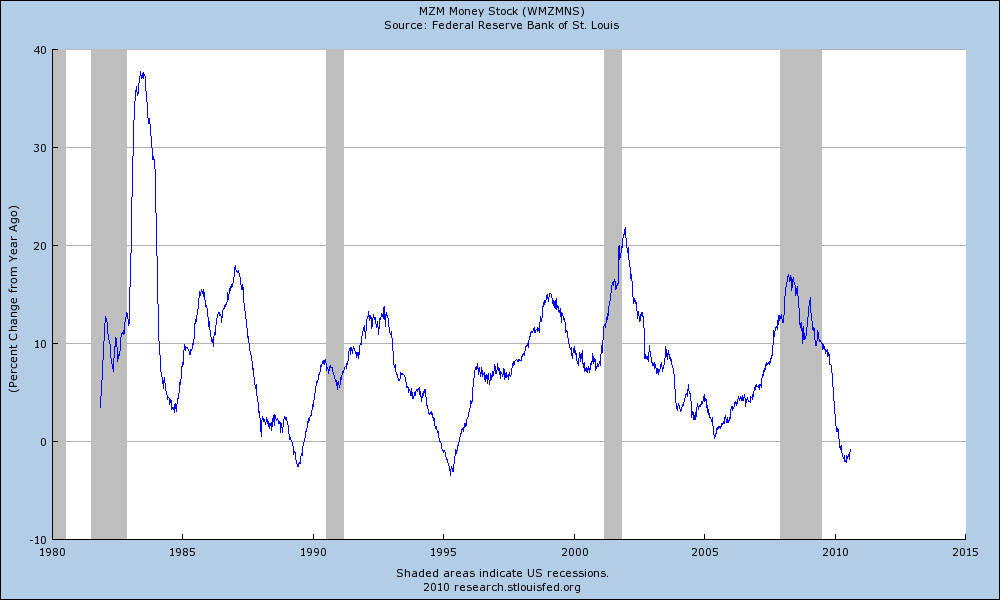

MZM Year over Year Growth

True Money Supply (aka Rothbard Money Supply)

"The True Money Supply (TMS) was formulated by Murray Rothbard and represents the amount of money in the economy that is available for immediate use in exchange. It has been referred to in the past as the Austrian Money Supply, the Rothbard Money Supply and the True Money Supply. The benefits of TMS over conventional measures calculated by the Federal Reserve are that it counts only immediately available money for exchange and does not double count. MMMF shares are excluded from TMS precisely because they represent equity shares in a portfolio of highly liquid, short-term investments which must be sold in exchange for money before such shares can be redeemed. For a detailed description and explanation of the TMS aggregate, see Salerno (1987) and Shostak (2000). The TMS consists of the following: Currency Component of M1, Total Checkable Deposits, Savings Deposits, U.S. Government Demand Deposits and Note Balances, Demand Deposits Due to Foreign Commercial Banks, and Demand Deposits Due to Foreign Official Institutions."

Eurodollars

I think a case could be made that the US is exporting its monetary inflation overseas, particularly to Asia. At some point these eurodollars may come home to roost, and the arrival could be quite memorable. I try to recreate some sense of Eurodollar growth from the BIS reports, especially when verifying these eurodollar short squeezes, but the lags of over a quarter in reporting are quite tiresome.