The ONLY Reason Stocks Have Rallied This Month

Courtesy of Graham Summers

The Fed generally claims that it stopped its first Quantitative Easing (QE) program back in March 2010 and that there were no additional debt monetizations between then and the announcement of its QE lite program in August.

Yet, as I’ve proven time and again, the Fed has continued to monetize Wall Street’s debts EVERY options expiration week since QE 1 ended… proving beyond a doubt that the Fed’s QE program did NOT actually end in March.

Here’s the chart of the Fed’s recent actions for those of you who haven’t seen this before. Options expiration weeks are in bold.

|

Week |

Fed Action |

|

July 22 |

-$8 billion |

|

July 15 |

+$8.6 billion |

|

July 8 2010 |

+$1 billion |

|

July 1 2010 |

-$13 billion |

|

June 24 2010 |

+$175 million |

|

June 17 2010 |

+$12 billion |

|

June 10 2010 |

-$4 billion |

|

June 3 2010 |

+$2 billion |

|

May 27 2010 |

-$16 billion |

|

May 20 2010 |

+$14 billion |

|

May 13 2010 |

+$10 billion |

|

May 6 2010 |

-$4 billion |

|

April 29 2010 |

-$1 billion |

|

April 15 2010 |

+$31 billion |

|

April 8 2010 |

+$420 million |

|

April 1 2010 |

-$6 billion |

You’ll note that the Fed ALWAYS made its largest capital contributions during options expiration weeks. Heck it pumped $31 BILLION into the system in April 2010, just ONE MONTH after it claimed QE 1 ended!

However, since that time the Fed has pumped a total of over $65 billion into Wall Street on options expiration weeks. On non-expiration weeks the Fed either withdraws money or makes small money pumps.

This pattern finally ended in August 2010 when the Fed failed to pump the system on options expiration week. But then again, why bother? The Fed was about to announce its QE lite program in which it would use the interest on maturing securities to purchase Treasuries from Wall Street Primary Dealers via its Permanent Open Market Operations (POMO).

I realize that last sentence is a lot to take in. So let me explain how this new QE Lite Program works before we continue.

During Treasury auctions there are 18 banks, called Primary Dealers, who are given unprecedented access to US Debt (Treasuries) in terms of pricing and control. These are the BIG BOYS of finance including firms like Goldman Sachs (GS), JP Morgan (JPM), Bank of America (BAC), Credit Suisse (CS), and others.

During its QE 1 Program, the Fed bought over $1.0 trillion in securities from these firms. Its new QE lite program consists of it using the interest and proceeds from the securities in its portfolio that are maturing to buy Treasuries from the Primary Dealers via Permanent Open Market Operations (POMO).

In simple terms, the POMO actions allow the Fed to pump money into Wall Street (by buying Treasuries from the Primary Dealers) without DIRECTLY monetizing Treasury debt (the Treasuries had already been issued). The Primary Dealers then take this fresh capital from the Fed and plow into stocks, forcing the sort of ramp job we saw last week on Friday.

All told, the Fed has bought $20 billion worth of Treasuries in this fashion, $11.15 of which it purchased last week alone. With this kind of weekly money pumping in place, Bernanke and pals don’t need to continue their “behind the scenes” games (like the options expiration week money pumps).

Or do they?

Unbeknownst to most investors, last week Ben Bernanke pumped an additional $11.05 BILLION into the system ON TOP of the $11.15 pumped via the POMOs. In plain terms, the Fed juiced the system by $20+ billion in a single week, bringing its liquidity pumps RIGHT BACK QE 1 LEVELS.

If you want to know why stocks have rallied in the last month, this is THE reason. The economy isn’t improving and the European Crisis isn’t over. Nothing has improved. All that has happened is the Fed funneled money into the Primary Dealers who ramped the market.

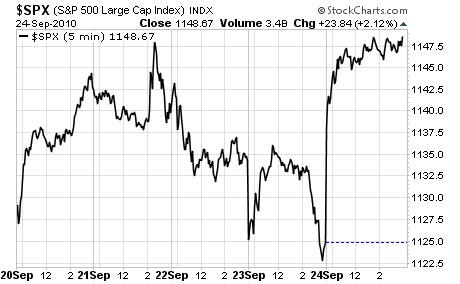

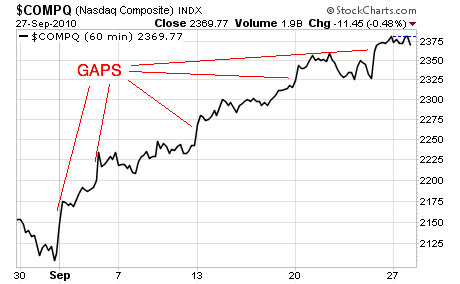

This is also the reason why the latest rally has almost entirely consisted of gap ups: the Primary Dealers ramp the market and then the computer trading programs take care of the rest.

In plain terms, the market is being juiced higher, plain and simple. There is no fundamental reason for stocks to be rallying. Moreover, we have numerous signs of a top forming (mutual fund cash levels, insider selling to buying ratios, negative divergence, etc). Those who choose to buy into the farce of a rally are going to get what’s coming to them. And when they do, it won’t be pretty.