Courtesy of The Automatic Earth

Check the hands

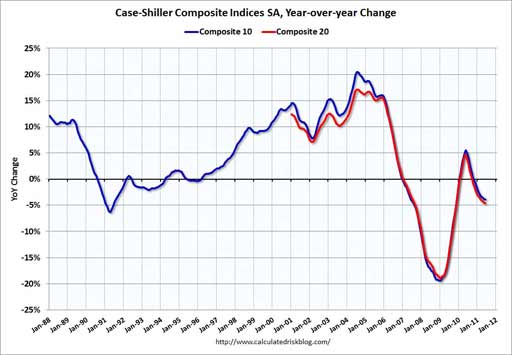

Ilargi: The YoY Case/Shiller housing index came in ugly today. "S&P/Case-Shiller index of property values in 20 cities fell 4.5 percent in June from a year earlier, after a 4.6 percent drop in the 12 months ended in May that was the biggest since 2009." Still, I saw headlines that claimed "Case Shiller: Home Prices increased in June", this one at Calculated Risk. Here’s thinking that’s perhaps a little more optimism than we deserve.

Now, I know Bill McBride uses seasonally adjusted numbers, while S&P doesn’t, but still. Creating the impression that the numbers were somehow positive does not seem warranted by developments, unless perhaps you work at the NAR or Fox, organizations that create their own reality. My problem with it is that it may induce people to make purchasing decisions they will live to regret, possibly for the rest of their lives.

I’m a big fan of CR, don’t get me wrong, but this looks too much like spinning, and I wish it wouldn’t happen. That "Home Prices increased in June" headline pops up in the same daily read as this from Bloomberg, based on exactly the same sets of numbers [..] "home prices declined for a ninth month." I rest my case. Here’s Bill’s own graph based on the data, you decide.

At about the same time the housing report came in, US consumer confidence was reported thusly: "The Conference Board’s index slumped to 44.5, the weakest since April 2009, from a revised 59.2 reading in July [..]. It was the biggest point drop since October 2008."

Luckily (?!) the US isn’t alone: "European confidence in the economic outlook plunged in August by the most since December 2008 as a persistent debt crisis roiled markets and clouded growth prospects. An index of executive and consumer sentiment in the single-currency region fell to 98.3 from a revised 103 in July [..] "

European stock markets didn’t even notice. Only Frankfurt was down. The idea seems to be: Consumers, who needs consumers? Sort of reminds you of the days of old, when "jobless recovery" was all the rage. Not so much now.

If European markets had any sense left, they’d have paid attention to the farce performed inside the EU/IMF/ECB troika over the weekend, with guest roles for the the International Accounting Standards Board (IASB) and the European Banking Authority (EBA).

But first, before I forget it, next week, on September 7, the German constitutional court will rule on the question whether European bail-outs are in accordance with a) German law and -possibly- b) EU law. There’s a real possibility that the answer to both will be "no". And then we can have some real fun.

Christine Lagarde, new at the helm of IMF and formerly Finance Minister in France, said in Jackson Hole a few days ago that European banks need urgent recapitalization. ECB president Trichet and the European Commission’s economic chief, Olli Rehn, reacted as if Lagarde was some sort of raving lunatic. Here’s thinking that’s not wise if you want to hold on to what credibility you have left. It’s not like she’s not some dumb puppet that you can sweep aside at will. Other than despair, it’s hard to see what would lead to such vehement reaction. Roland Gribben at the Telegraph writes:

EU rules out fresh capitalisation for Europe’s banks

A fresh round of capitalisation for European banks was firmly ruled out by EU officials and bankers when they appeared before an emergency meeting of the European Parliament’s economic committee.

The officials poured cold water on calls from Christine Lagarde, head of the International Monetary Fund for "mandatory" recapitalisation to avoid another financial crisis but acknowledged that the EU economy was continuing to weaken.

Jean-Claude Trichet, president of the European Central Bank, said there was no shortage of liquidity in the European banking system. EU economic commissioner Olli Rehn insisted that the health of EU banks had improved over the last year.

Ilargi: That’s just hilarious. These banks all on average lost, what, 50%+ in market value over the past year, but their "health" improved?!

No shortage of liquidity whatsoever, right? I wonder about that, seeing this from FT:

European officials round on Lagarde

European officials rounded on Christine Lagarde on Sunday, accusing the managing director of the International Monetary Fund of making a "confused" and "misguided" attack on the health of Europe’s banks.

Ms Lagarde, the former French finance minister who replaced Dominique Strauss-Kahn as head of the IMF in July, used her address at an annual meeting of central bankers in Jackson Hole, Wyoming, to call for an "urgent" recapitalisation of Europe’s weakest lenders, saying that shoring up the banking system was key to cutting "chains of contagion" across the region.

But officials said Ms Lagarde’s comments missed the point of banks’ current difficulties. "The key issue is funding," said one experienced central banker. "Banks in some countries have had trouble securing liquidity in recent weeks and that pressure is going to mount. To talk about capital is a confused message. Everybody – politicians, regulators, other officials – is quite concerned."

Ms Lagarde’s allusion this weekend to the potential use of the European Financial Stability Fund, a €440bn bail-out fund, as a means to recapitalise banks by force, would be far better directed towards a liquidity solution, some officials said. No headway has been made towards the idea of EFSF-guaranteed bank bond issuance, they admitted, though that would be the "most sensible solution", according to one.

Jean-Claude Trichet, the president of the European Central Bank, separately dismissed any idea that Europe could face a liquidity shortage in his own Jackson Hole address, saying efforts to combat the financial crisis would prevent such an outcome. "The idea that we could have a liquidity problem in Europe" is "plain wrong," Mr Trichet said.

Ilargi: What? It’s not about liquidity, it’s about funding, says "one experienced central banker". But then: "[..] the potential use of the European Financial Stability Fund, a €440bn bail-out fund, as a means to recapitalise banks by force, would be far better directed towards a liquidity solution, some officials said." And Ms Lagarde is called "confused" and "misguided"?! These guys seem to give the term "speaking in tongues" a whole new meaning. A forked one.

A relatively unknown source comes to Lagarde’s aid, as per Der Spiegel:

Watchdog Worried About Europe’s Banking Sector

The head of Europe’s banking watchdog has called for the euro rescue fund to provide direct aid to ailing banks to help calm markets. The head of the IMF made a similar demand, exposing an apparent rift with EU governments on how to handle the debt crisis. Berlin and the EU have rejected such changes.

The new powers of the euro bailout fund haven’t even been signed off yet by the national parliaments, but there are already calls for its remit to be broadened, causing a fresh headache for Chancellor Angela Merkel.

The European Banking Authority, a supervisory body for banks in the European Union, wants the €440 billion ($635 billion) European Financial Stability Facility to provide direct capital injections to ailing banks. It is an attempt to reassure investors worried about the impact of the debt crisis on bank balance sheets, German business daily Financial Times Deutschland reported on Tuesday.

At present, the EFSF is only permitted to extend funds to individual countries, but those nations can pass the funds on to banks. Direct finance injections by the EFSF would speed up the process, and would in effect turn the fund into a stakeholder of the banks it helps. The demand was made in a letter being sent by EBA chief Andrea Enria to the European finance and economy ministers this week [..]

Ilargi: It’s all about the dance around the EFSF. Lagarde wants it used to bolster EU banks. Trichet and his ilk deny that that is even needed. Thing is, it’s not nearly large enough once Italy and Spain get squeezed, and the chances that it ever will be are as slim as the facility itself. Despite claims such as these by Christian Reiermann in Der Spiegel:

Klaus Regling, the German CEO of the euro zone’s bailout fund, the European Financial Stability Facility, is confident that the monetary union can overcome the current crisis. He considers the euro zone to be in a better position than the US when it comes to public debt, and accuses his fellow Germans of "hysteria." [..]

What is now taking shape at the EFSF’s offices at 43, Avenue John F. Kennedy in Luxembourg City is the nucleus of a super-authority with which the 17 countries in the euro zone hope to save their currency. The amount of money it has at its disposal in the event of an emergency — €440 billion ($634 billion) — is three times as large as the entire European Union budget. The EFSF and the ESM will have a similarly important effect on the stability of the euro zone as the European Central Bank (ECB).

Birth of a European Monetary Fund

If German Chancellor Angela Merkel and French President Nicolas Sarkozy have their way, Regling’s bailout fund will turn into a European Monetary Fund, which, like the International Monetary Fund (IMF), would monitor the financial and economic policies of its member states and, if necessary, come to their rescue with billions in bailout funds.In some ways, the EFSF’s powers go well beyond those of the IMF. The EFSF is supposed to be able to lend money to countries experiencing short-term liquidity problems and use its billions to stabilize tottering banks. The most important of the recent changes is that Regling will be able to intervene in the markets and buy up government bonds to stabilize their prices and yields.

Because the new tasks cannot be effectively addressed with the current workforce, Regling intends to double his staff from 12 to 24 employees in the course of the next year. But he "does not see the need at this time to increase the financial framework of the EFSF," says the 60-year-old CEO. Even when Greece receives help from the fund as part of the second bailout which was agreed at the July 21 summit of euro-zone leaders, more than half of the approved €440 billion will still be left over, Regling says.

Nevertheless, when the EFSF takes over the ECB’s task of buying up debt-stricken countries’ sovereign bonds in the fall, it could quickly run up against its limits. But Regling shrugs off such concerns. He doesn’t say it, but he knows that the finance ministers in the euro zone would beef up his funds if necessary. German Finance Minister Wolfgang Schäuble and his Dutch counterpart, Jan Kees de Jager, have already indicated their willingness to do so.

Ilargi: De Jager has recently declared his firm opposition vs a larger EFSF, and though he shuffles around the musical chairs in the game as much as any politician, plans for a €2 trillion+ EFSF will lead to severe turmoil in Europe, and cost more than one politician his or her career. And they know it. These guys are very close to a check mate.

No matter how justified Lagarde’s claims may be, Europe doesn’t have the means to fund its banks, has neither the financial nor the political capital, as I’ve said many times before. And so it has to tear apart the troika that until just a few months ago seemed to be saving Europe. Lagarde is now free to make demands that neither Merkel nor Sarkozy can meet. But that doesn’t mean these demands can be met.

There are more tricks being played under the table and behind the veil. Tricks without which reality would look much harsher. Adam Jones and Jennifer Thompson at FT report:

IASB criticises Greek debt writedowns

In a private letter sent to the European Securities and Markets Authority, the European Union’s market regulator, the International Accounting Standards Board criticised the inconsistent way in which banks and insurers have been writing down the value of their Greek sovereign debt. [..]

Financial institutions have slashed billions of euros from the value of their Greek government bond holdings following the country’s second bail-out. The extent to which Greek sovereign debt losses were acknowledged has varied, with some banks and insurers writing down their holdings by a half and others by only a fifth.

The letter did not single out particular countries or banks. But according to one person familiar with the correspondence, it reflected concern at the approach taken by BNP Paribas and CNP Assurances.

The French bank and insurer both announced 21% writedowns, as envisaged by last month’s Greek bail-out. They argued there were no reliable market prices to guide a "fair value" for Greek government debt because of their illiquidity and instead used a "mark to model" valuation. Banks and insurers that used market prices suffered a bigger hit. Royal Bank of Scotland wiped £733m from the value of a £1.45bn Greek government bond portfolio – a 51% cut.Mr Hoogervorst challenged the justification for a "mark to model" approach and also the valuations these produced. "Although the level of trading activity in Greek government bonds has decreased, transactions are still taking place," he said. "It is hard to imagine that there are buyers willing to buy those bonds at the prices indicated … it is therefore difficult to justify that those models would meet the objective of a fair-value measurement."

Ilargi: Now that we’re talking credibility, one thing seems obvious. If one bank writes down Greek debt by 20%, and another by 51%, you really need to wonder what the value is of a stress test, such as the one only recently completed in Europe. If such a test allows banks to assess the value of -part of?!- their assets on their own recognizance, then the test will be seen as completely useless. Again, it all smacks of despair. And frankly, it’s hard to see what else is left for Europe to do.

But, what I wrote three weeks ago is still valid: The Markets Are Not Stupid. They can try, though… Irwin Stelzer in the Wall Street Journal puts it this way:

Telling World’s Bankers How It Really Is

The problem in Europe is that politicians think they can fool the markets. Spain is amending its constitution to include a deficit cap in its constitution—the first country to respond to lender-in-chief Angela Merkel’s demand that all supplicant nations do so—but the amendment does not include any actual deficit cap.

France has joined Ms. Merkel’s call for balanced budgets, but has not balanced its own budget in 35 years, and is unlikely to do so soon as its economy is slowing, and will slow further when planned tax increases on capital gains, businesses, and the rich—who have published a Warren Buffet-style plea to have their taxes raised "reasonably"—are put into effect. Greece has promised to privatize large swathes of its economy, but has not so far sold off any significant assets. Italy has refused to undertake the structural reforms needed to end a decade of economic stagnation. Markets are appropriately skeptical, nay, cynical.

Ilargi: Spain, France, Italy, Greece, and feel free to add Portugal, Ireland and Belgium; they all make promises they know they can’t keep. And internally they can get away with doing so because everybody knows that meeting the promises will be the end of the road. For all. The problem for them is the markets will not let them get away with it.

Having no credibility left, in the situation they’re in, means they’re done. Accepting that is just not something politicians and other power hungry folk give in to easily. They all have the same MO as Eurozone finance head Jean Paul Juncker: "When it becomes serious, you have to lie …. " They’d rather take down their entire nations with them than admit defeat. And that’s what we’re looking at.