{kind=link}

The Subordination in Spain Will Cause Pain

Courtesy of Bruce Krasting

As of Sunday morning there are no details on the Spanish bank bailout. The only information released is the amount – Euro 100B. This is a nice round number.

Last week the IMF suggested that Euro 40B might be the right number. Now we get a deal for 2+Xs that. I think this was orchestrated to leave the markets with the impression that massive firepower has been garnered, and therefore the problem is now contained. Rubbish.

I’ll hazard a guess on how this bailout may be structured:

The EFSF will make a loan to the Republic of Spain. The Spanish government will use this money to recapitalize the Spanish banks. The critical question is what form the deal will take. There are only two options:

1) – The Spanish government could acquire new common or preferred shares of the banks that are in trouble.

2) – The banks that need a bailout will issue new debt securities; the Spanish central bank (or Treasury) would buy the debt instruments.

#1 is the only option that should be considered. New cash equity in the ailing banks is the only transaction structure that will result in stabilizing Spain’s banks. I doubt that this will happen. I see the “easiest/convenient” solution as #2; more debt.

A bank capitalization structure typically has these components:

.

Spanish banks have already hocked any available assets that could be used to “secure” the debt that will be issued in the bailouts. Therefore, the only alternative is for the banks to issue new debt that is unsecured. This is a subtle difference, but an important one. It might end up blowing up the entire European banking sector.

There is a simple fact that must be considered. Any debt that a Spanish bank has outstanding to the Spanish government is Senior to all other classes of debt except depositors. It doesn’t matter what the language says in the creditor agreements. What matters is how the markets will perceive the transaction.

I know how the market will react. If one were a holder of a Senior Debt security of a Spanish bank on Friday, you would end up with a functionally subordinated debenture after the bailout transaction on Monday. Any publicly issued senior debt (including senior secured) of that bank issued after the government bailout debt was created, would be perceived as tainted. It would be unsalable swill. The existing bond debt would sink like a stone.

This discussion is somewhat irrelevant when it comes to Spain’s banking system in June of 2012. The capital structure of many Spanish banks is already toast. So the details of the bailout don’t really matter at this point. In all likelihood the market’s knee jerk reaction will be:

.But not too long after, the reality will set in. A precedent will have been set on what may/will happen to banks in other European countries. Should the bailout of Spanish banks be accomplished via the issuance of new debt (versus equity), then damn near every bank in the EU will have a run on the debt portion of its capital structure. It will happen first with the Italian banks, from there, it will head to Paris.

Holders of senior bank debt have few options faced with this scenario. They could (1) dump their holdings, or attempt to hedge some of the risk. The only hedges available are (2) CDS, or (3) a short of the common stock. A combination of 1,2&3 would be devastating to the EU banking system.

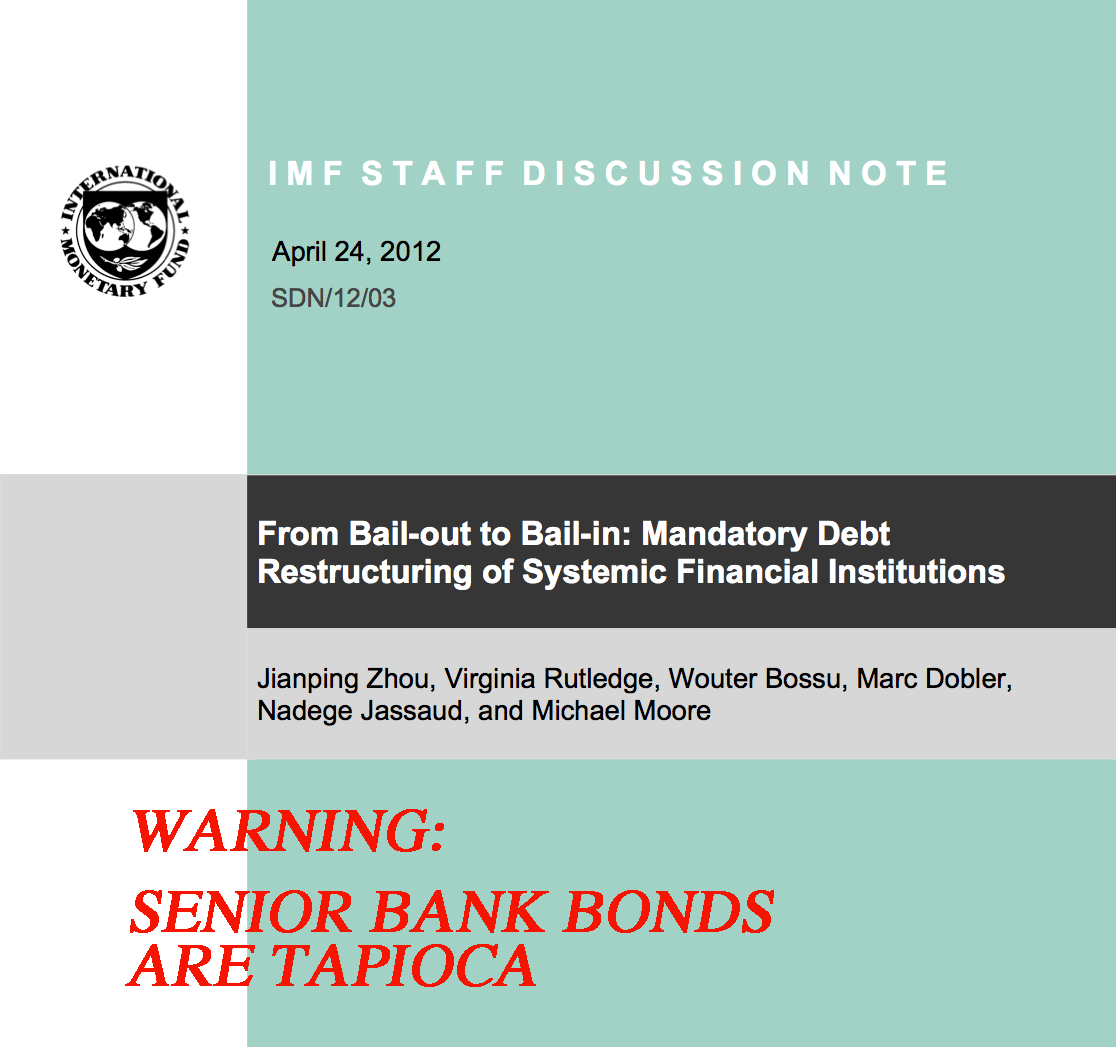

The IMF published a lengthy report on the topic of Senior bank bonds on April 24 (convenient timing). The bottom line conclusion of the IMF? It recommended a “bail-in”, where the senior bondholders of banks get crushed. I found this startling:

.

.

Bail-in, which is a statutory power of a resolution authority to restructure the liabilities of a distressed financial institution by writing down its unsecured debt and/or converting it to equity.

.

The USA set the precedent on Senior Debt of the TBTFs. The shareholders of the TARP banks took losses, but bondholders got a free walk. In the case of Fannie and Freddie, all of the creditors, including subordinated note holders, got paid off at a premium.

If the Spanish bank bailout deal ends up subordinating existing bondholders, it will create a whole new wrinkle to worry about. Portfolio managers who hold senior bank bonds of other EU banks will crap in their pants.