{kind=link}

Courtesy of The Automatic Earth.

I’ve said this before, but just in case: I have very little appreciation and/or patience for the field of economics and its practitioners. Labeling it "the dismal science" does it far too much honor in my view, since it's not a science at all. No more than psychology is, or anthropology, or beer brewing. Nothing that can't stand the falsifiability test Karl Popper left us is a science. Falsifiability is the dividing line between the real thing and a whole wide range of mere pretenders.

That said, if there's one economist today (OK, maybe a few more) who I would be tempted to make an exception for, simply because he's made it his goal to at least approach economics from a solid Popper-like viewpoint, it's Steve Keen and his rigorous math. It's therefore no coincidence that Steve is both a good friend of The Automatic Earth, and controversial.

Since about WWII at the latest, a certain group of economists, think Chicago, have tried their stinking best to best recognized as scientists, an attitude that culminated in the launch of the faux Nobel Prize in 1968. They produce serious looking formulas and graphs up the wazoo, which the media reproduce alongside interviews replete with lofty terminology, and the general public has fallen for the trick: ridiculous though it may be, the field has acquired a scientific aura.

Why did and do they want this? Because trillions of dollars worth of policies based on their ideas gain critical respectability if they can make themselves look credible and in control. So it's no surprise that the entire effort has been carried by the support of virtually unlimited amounts of money from the finance industry, as well as 99% of the ruling political classes.

That's how Milton Friedman and his Chicago School became so prominent. Nothing to do with science, let alone falsifiability. Just money. Credibility for sale. If you're a politician, and you manage to get make people, your voters, believe that there's a scientific underpinning to whatever it is you want to do economically, you got it made. And there are plenty of rich people and institutions willing to finance that fake science, since it serves their purposes.

This is to a large extent why we are where we are: stuck in a long, long crisis. If you take a simple belief system, phrase its beliefs in difficult looking formulas and graphs, and thus dress it in the veneer of some kind of a scienctific method, you can push societies to the brink of financial disaster, and it makes no difference whether you're wrong 9 times out of 10. You just tell them that it's all very hard to understand, and you set up an education system that teaches only the models you want it to teach. This way you create the idea that things are knowable while they are not, and all students have to do is get a degree and be the next high-priests. Any religion that poses as a science is dangerous, and economics more so than all others, because it can turn entire societies into poorhouses.

Against that backdrop, it's not terribly surprising to hear that Steve Keen and his entire economics department at the University of Western Sydney (UWS) are under threat of extinction. The Australian government has used a nice trick to achieve this. Under the guise of creating more competition, it destroys it. Anyone who can fog a mirror can now apply to the "top" universities in Australia, no matter what their grades are coming in. This is the sort of thing that ostensibly aims for fairness, in the same way that globalization and privatization do. All hail the lowest common denominator. The result is that everyone applies at the top uni's, and only there.

Since the University of Western Sydney, where Steve teaches, has never been promoted to the top (though its economics programs may be far better than the others'), nobody applies for its programs anymore. And though this is an entirely new situation, the government has already proposed simply closing down the economics department at UWS. Even though the situation is volatile, and many students who won’t get into the top schools will likely come to UWS later.

The measures taken by the Australian government are too broad and wide-ranging to make any sort of claim that they are aimed at any specific people, but that doesn't mean there won't be plenty people, read: those working in economics (certainly in Australia), who are quite happy with the fallout. Steve himself puts it like this:

A fail grade for market deregulation

The older I get, the more cynical I become about government intervention in the economy. That statement might appear to be either a recantation of everything I’ve ever argued, or a sign of the usual tale of left-wingers moving to the right, and right-wingers to the left, as life experience tempers youthful exuberance. It’s neither (well, okay, maybe it’s a bit of the latter), because my developing position reflects the complexities of a mixed economy.

The latest real world experience that has pushed me further into cynicism about government is a very personal one: an attempt by the Australian government to increase competition in education via deregulation is the direct cause of the proposal to terminate the economics program at my university. The policy change will actually reduce competition in the education marketplace in Australia: the market was more competitive with the preceding regulations in place.

Is your head spinning yet? Let me clarify the position by explaining why my university (the University of Western Sydney) is proposing to shut down its economics program.

Government regulation used to require universities to set a minimum entry standard to apply for entry to courses based on performance at the final school exam (now known as an “Australian Tertiary Admission Rank” or ATAR). Deregulation of the sector means that this is now optional, and two major universities in my region – the University of NSW and Sydney University – have responded by letting students apply for a course regardless of their anticipated performance at high school.

When a minimum ATAR was indicated, many students who thought they wouldn’t get a good enough high school result to qualify at one of the higher ranked universities would hedge their bets by also applying for entry to some of the lower ranked universities – including UWS. That then meant that at the end of one academic year, there was a reasonable spread of applicants across all universities: the top-ranked universities got the lions’ share, but there were applications too for the lower-ranked universities, from students who also expected to be more lowly ranked.

Now that open slather is permitted, students have responded by applying for courses only at the top-ranked universities. So now, as the current academic year ends, the projected intake into UWS’s economics program is catastrophically low. In previous years we had well over 100 applicants for our first year intake at this point. This year, we have just 19.

UWS management’s reaction to this has been to propose to shut the degree down completely because it is no longer economically viable. As they put it to one of the many ex-students who has complained about the decision:

"Whilst we acknowledge the tremendous achievements of our staff and students in raising the profile of economics at UWS and beyond, unfortunately, at the present time just 19 students are forecast to enter the B.Ec course in 2013, which renders the course economically unsustainable. This is largely attributable to the advent of the open market for undergraduate courses which was implemented this year."

Over the 20 years or so he's been at UWS, Steve has built a unique position in the field, and his position and views are so different from that of his peers that they will be glad to see him go, lest he makes them look bad, or worse. Economics as we know it these days is a one-dimensional exercise, along the exact same lines US politics is. That is to say, there is a media-hyped fake distinction between two heads of the same beast, a distinction aimed solely at fooling people into thinking there are actual differences. Whether it's neo-classical, Keynesian or any other flavor of the day, the foundations remain the same: no matter which head you pick, it's still the same beast.

Steve will be alright, he's made a name for himself that has even given him a voice on the BBC. His students, present and future, however, will not. The potential scope of different views in and on economics is being narrowed even more than it already was. Soon everyone will have the exact same ideas, and no dissonance will be either allowed nor available. And you may think that in today's world, Paul Krugman's idea(l)s concerning spending your way out of debt represent a fundamentally different view from those that favor cutting the debt, but these are not the fundamental issues. What is fundamental is the understanding of the role of debt and banking systems in our economies. And neither Krugman nor his alleged "adversaries" have any such understanding.

Steve Keen once again explained this and other topics very eloquently in an interview last week on Russia Today's Capital Account:

The economists who today control the ways we fight our financial crisis, view the economy in the exact same deluded ways that those did who led us into it. The EU's bureaus are full of such conventional economics disciples, and in the US people like Larry Summers and Christina Romer were highly influential until recently in formulating economic policy. Tim Geithner's still there.

And lo and behold, people are starting to think that these geniuses have found the right ways to fight the crisis. But they have of course not solved one single riddle. You can't solve a problem that you don't understand. They have thrown trillions into the financial system and the result is that today in the US home prices are down 35% and real unemployment is stuck somewhere between 12% and 16% or thereabouts. Yay!

So what is the solution? It's simple really: try science, try physics, and don't fake it. If you can only produce things that violate thermodynamics, get rid of them. And get rid of all the posers, and make economics a field that doesn't just function to produce theories that help a small part of the population fool the rest. Here's a start, as Steve Keen writes it:

The question "where does income come from?" was at the core of pre-neoclassical theories of economics. It was phrased differently, as the question of the “theory of value”, but the essence of the question was “what is the source of the physical surplus of goods that are produced each year?”

The issue disappeared in modern neoclassical economics because the word 'value' was reduced simply to a question of relative prices – which is why I titled one chapter in my book Debunking Economics “The Price of Everything and the Value of Nothing”. But the topic is far more than just a question of how relative prices are set. At its heart, this is an existential question: humanity produces not merely enough to stay alive from year to year, but a surplus above needs that (at least for some) results in enormous opulence.

Of course, one simple answer is that there isn’t a surplus – some are driven below subsistence, and their suffering becomes the source of the excessive incomes of the minority. [..]

In the 20th century, the ascendant neoclassical theory argued that you couldn’t favour one input over the other: both labour and capital contributed to output, and could be smoothly substituted for each other in what they called a “production function”.

The problem for neoclassicals was that, just as Marx’s argument created a conundrum for Marxists, so did the core neoclassical model – developed by Robert Solow – for neoclassicals. Changes in the amount of labour and capital in Solow’s model accounted for less than 50% of recorded growth: the gap, which became known as “Solow’s Residual”, was attributed to technological change – for which neoclassical economics had no theory.

If this looks like a mess to you, you’re right: economic theory should be able to answer this question, but the best it has managed is to get it less than half right.

The solution, ironically, is to return to the 19th century – though not to its economists but to its physicists, and in particular Ludwig Boltzmann, who developed what is now called the second Law of Thermodynamics. These laws, unlike those of economics which are violated more often than observed (anyone for the Law of One Price, or the Law of Demand?), cannot be broken – and production, which is a physical activity, must therefore obey them.

The four laws of thermodynamics are neatly summarised in a simple ditty: 0th: You must play the game; 1st: You can’t win; 2nd: You can’t break even; 3rd: You can’t leave the game.

The zeroth law concerns the dynamic tendency of energy to dissipate. [..] The first is the Law of Conservation. [..] The second is the real catch: the degree of order tends to diminish over time. Connect one vessel full of air to another with a complete vacuum, and over time the pressures will equalise. [..] The third law says that you can escape the consequences of the second law if and only if you can dump the waste heat from a working engine into a vessel whose temperature is absolute zero – minus 273 degrees Celsius. Unfortunately, there is no such vessel – hence “You can’t leave the game”.

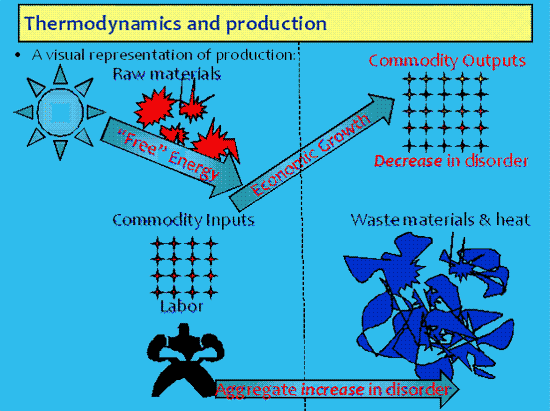

How does production – and the generation of a physical surplus – fit into this? Production appears to defy these laws. Each year we start with a given stock of produced outputs, which become inputs to production, and (except during recessions) we end up with a larger stock of more elaborately transformed outputs. Yet the second law can’t be defied, any more than one can defy the law of gravity. So production must cause an aggregate increase in disorder over time.

The only way to reconcile production with the second law is that production involves a localised reduction in disorder in the goods and services we generate, which is more than countered by an increase in disorder via the waste outputs from production. Figure one gives a visual representation of this process – and 'free' energy, energy not produced by humans but nascent in the universe itself – plays a crucial role.

This free energy can take many forms. It can be solar radiation, as indicated in figure one, but it can also be stored energy in fossil fuels, nuclear energy in transuranic elements, even nascent nuclear fusion energy in deuterium and tritium. Without this energy, production – and life itself – would be impossible.

It therefore turns out that the most realistic economic theory of “where does income come from?” was the first: that developed by the physiocrats. Their mistake was to identify the sun as the only source of free energy, and to believe that only agriculture could exploit it free energy. But they were the best: subsequent economic arguments, from Smith through Marx to Solow, took us further away from the proper foundation for a “Theory of Value”.

Econophysicists are taking us back to that foundation now, with the most well thought out work to date being done by Robert Ayres and his colleagues. Their empirically derived model, which treats energy as the key source of production and labour and capital as adjuncts to the exploitation of free energy, adds energy as an additional independent input to production. They call it an “energy-dependent Cobb–Douglas function”:

![]()

Whereas Solow’s model (which has labour and capital as independent inputs, but not energy) misses over half the actual growth, Ayres’s model’s fit to the observed growth in economic output in the US from 1960-2999 has an R-squared of 0.999.

Economics has to start from an explanation of where income comes from: a Theory of Value is inevitable. Since we live in a physical universe, this theory must be physical in nature, and the second law is the ultimate physical rule. In my future economic modelling, I’ll be revising my production equations to be consistent with Ayres’s work.

I'd say we have something to work with here. And I don't think we can afford not to try. The longer we leave our economies in the hands of a bunch of delirious high priests, the bigger the mess we leave our kids. We don't have any right or any reason to do that. There are people out there trying to do honest work that neither violates thermodynamics nor fails falsifiability, instead of dictating some belief system incapable of defining either debt or value. That's what's on offer here.