{kind=link}

Low inflation creating a QE trap

Courtesy of SoberLook.com

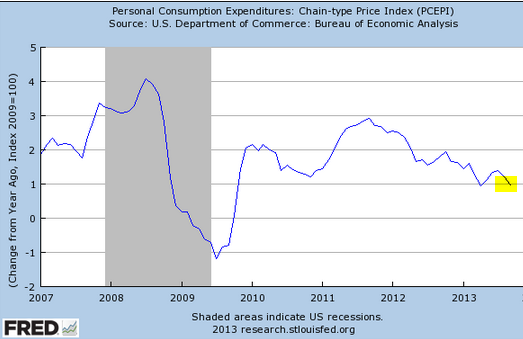

Scotiabank: – The Fed’s preferred measure of inflation — the price deflator for total personal consumer expenditures — came in at +0.9% y/y in September. We feel that markets are underestimating the importance of this observation to the Fed. That is tied with April for the softest inflation reading since October 2009 when the US economy was just beginning to emerge from recession.

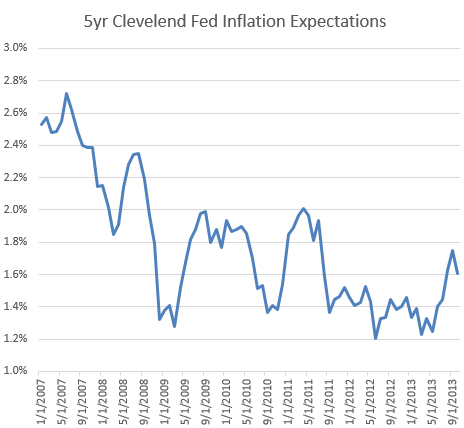

The forward looking inflation measure derived from TIPS yield (breakeven), has now also turned lower after a recent upward movement.

Similarly, we've seen a slump in commodity prices (see discussion), which is another signal of weak inflation readings.

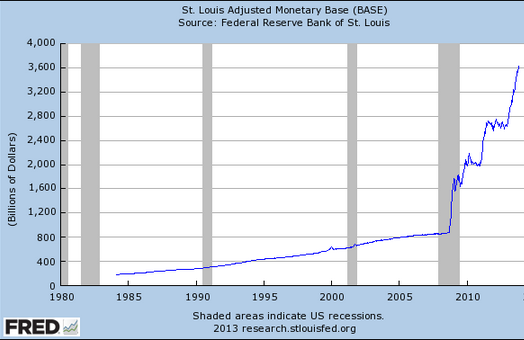

With inflation measures remaining this low, many argue (see story) that there is no rush to begin exiting the current monetary policy. The fact that the US monetary base is now 4.5 times greater than it was 5 years ago and capital markets are now fully addicted to ongoing stimulus does not seem add any urgency for these economists. The longer this goes on, the more difficult will be the exit, making it harder for the Fed to pull the trigger. Welcome to the QE trap.