{kind=link}

Courtesy of The Automatic Earth.

Russell Lee Hamburger stand in Harlingen, Texas Feb 1939

On this relatively quiet Sunday, why not delve into a topic that’s as timely as it is controversial topic: the US greenback. I see it moving a lot lately, and I see a lot of opinions being expressed on those moves. But for most of those opinions, I got to say: I’m sorry, but I don’t think so.

There’s such a huge amount of entrenched and ingrained ideas in the financial world about the dollar and inflation and gold, and an awful lot of it is in desperate need of, for lack of a better term, mental flexibility.

You can claim that the dollar will perish, and that’s true enough, but it will be – near – the last of all fiat currencies to do so. You can claim inflation is on the way, but that can’t happen without increased spending. And consumers who get poorer all the time cannot increase their spending.

You can claim the golden days of gold are nigh again, and that prices have been manipulated (not that I doubt that), but as long as the dollar’s alive, why should we assume that at least the American dollar generated part of the manipulation will stop? Gold will rise to the top once more alright, it always has, but it’s what to do in the meantime that’s more interesting for all but the 1%.

The Automatic Earth has always said that the US dollar would come out the winner among currencies. Simply because there is no other way. Eventually, the greenback will go the way of all fiat money, but that’s not going to happen tomorrow morning, and we need to find something to do with ourselves until it does.

The fact that the dollar is the world reserve currency is important, but it’s not no.1. Today’s world is drowning in debt, and a huge majority of it is denominated in US dollar. Yank up interest rates and dollar demand will soar like a BUK rocket. No matter what Russia and China and India invent in non-dollar trade. Too little too late.

The US Fed has prevented the dollar surge from happening over the past 7-8 years, and the entire globe has hidden and/or financed its deficits courtesy of that, but the Fed, for one reason or another, has decided to stop playing that game. Not only will there be fewer dollars made available (QE tapering), but the Fed funds rate will also be raised.

Present numbers from Fed sources being chewed on in the press are well above 1% in a year or so, from 0.25% now. Count your blessings, emerging markets. The question is: why would they do that at this point? I think a large part of the explanation is to be found in what I talked about in The Fed Has A Big Surprise Waiting For You.

That is, Wall Street sees its profit sources drying up because everybody and their pet hamster is on the same side of the trade. Which means if you can get them to stay there, and change the rules of the game behind their back in the meantime, potential profits are stupendous.

In The Fed Has A Big Surprise Waiting For You, I focused on interest rates (only). But I think what’s true for rates there, is also valid for the dollar: the Fed is changing its views and policies. And no, it does not have everybody’s back, not investors and, but that does hardly need repeating, Main Street.

Most people will still see the recent rise of the dollar in FX markets as just that, something that happens due to market mechanisms. Really, what market? It would be naive to think the Fed, which has controlled asset markets up to the point of being a direct buyer of stocks, and propped up the US housing market for years, would let the dollar either slide or rise as much as we’ve seen lately, and not act. Therefore, if you follow my point, it must have acted.

For the same reason that you shouldn’t assume too easily that the economy is recovering, you shouldn’t too easily assume the Fed is not aware of what happens to the USD, or doesn’t have a handle on it. Just as it would be silly, for that matter, to disregard off-hand the connection between economic depression and increasing cries for war, but that’s perhaps for another day.

Let’s turn to what others have to say about the dollar vs other currencies. First, a few quotes from the Australian rainforest, where the world’s finance ministers were gathered. I’m not sure whether to think the setting is too much for them, or that it fits just right. They sure produced some whoppers.

Currencies Back on Agenda as G-20 Monetary Policies Split

The dollar has climbed over the past three months against all 16 major peers tracked by Bloomberg, touching a six-year high versus the yen and a 14-month peak against the European currency.

• U.S. Treasury Secretary Jacob J. Lew renewed a call for member nations to avoid currency intervention in a bid to gain a competitive edge.

• South Korean Finance Minister Choi Kyung Hwan said divergent monetary policies “have the risk of increasing uncertainties in global financial markets,” while volatile foreign capital flows “could also have an impact on the foreign exchange rates.”

• “It’s important for foreign-exchange rates to move in a stable manner by reflecting economic fundamentals,” Bank of Japan Governor Haruhiko Kuroda said. Kuroda said this month he would do what’s needed to achieve the BOJ’s inflation target as he continues unprecedented easing.

• The ECB has cut interest rates to record lows and committed to boost its balance sheet to the levels it had at the height of the sovereign debt crisis in 2012. German Finance Minister Wolfgang Schaeuble told the G-20 meeting today that expansive fiscal and monetary policies could risk creating a bubble in equity and property markets, according to a German delegation official. ECB Governing Council member Jens Weidmann told Bloomberg that monetary policy should not be expansionary for longer than necessary to ensure price stability.

• [..] After finance ministers and central bank chiefs met in Moscow in July 2013, they pledged: “We will refrain from competitive devaluation and will not target our exchange rates for competitive purposes.” Lew yesterday revisited language from that communique. Lew told South Korea’s Choi that countries must meet “commitments to move toward market-determined exchange rates.”

• Choi said the South Korean government is “not at all” intervening in the foreign-exchange market to determine the won’s level. Lew’s comments were “reiterating the importance” of the issue, rather than singling out South Korea, Choi said. While Choi said he lets the market determine the strength of the won, it’s different when moves are extreme. “If there is a very sudden tilting toward one direction in a very short period of time in the foreign exchange market, then there would be some smoothing operations.”

Note to Self: If and when Jack Lew says that “countries must meet “commitments to move toward market-determined exchange rates”, he’s actually saying that at present there are no market-determined exchange rates. Not a minor thingy.

What’s happening with the US dollar is exceptional, it’s not some sort of fluke:

Dollar Has Longest Winning Streak Since 1967 on Divergence

The dollar had its longest stretch of weekly gains since Lyndon Johnson was in the White House after the Federal Reserve signaled an end to unprecedented monetary stimulus measures next year. The U.S. Dollar Index advanced for a 10th straight week, the longest since at least March 1967, when Johnson was in the fourth year of his presidency.

“The dollar is the No. 1 trend across all asset classes going into the end of the year,” Neil Azous, founder of Stamford, Connecticut-based research firm Rareview Macro LLC, said in a phone interview. “It’s back to trading interest-rate fundamentals.”

[..] “ … the dollar has been so depressed over the last few years, and now that depression is unwinding, like a coiled spring,” Douglas Borthwick, head of foreign exchange at Chapdelaine & Co., said. “The Dollar Index will continue to stay bid as long as the Japanese continue to make motions of quantitative easing while Europe makes more noise about expanding their balance sheets.”

[..] The U.S. Dollar Index has rallied 5.9% this year, set for the biggest annual gain since 2008, when the Fed began the first of three rounds of bond purchases under the quantitative-easing stimulus strategy. The gauge lost 4.2% in 2009.

[..] The dollar has risen 3.2% in the past month in a basket of 10 developed-nation currencies tracked by Bloomberg Correlation-Weighted Indexes. The yen has lost 3.3%, the biggest decline, and the euro has fallen 1.1%. Sterling has gained 0.9%.

Mr Borthwick is right, but I’m not sure he understands why he is. He’s dead on remarking that “the dollar has been so depressed over the last few years”, but he should note that it’s the Fed that has been depressing the dollar, not the markets. The recent surge doesn’t even have to be due to active support, the simple lifting of whatever measures kept it down is sufficient.

Keep your cool and shrink the amount of available dollars. That’s all it takes. The, from a market point of view, insanely high prints for the Euro against the USD, which lasted for years at $1.30 to $1.40, are let go. Big move. Not in the least for US businesses.

Dollar’s Rally Bad News For Oil, Multinationals

The asset with the greatest prowess of late has been the U.S. dollar, and if its rally continues, it threatens to eat into the earnings of multinational companies. The greenback’s recent gains have lifted the dollar index – a measure of the dollar’s value relative to six currencies – for 10 consecutive weeks.

That marks the dollar’s longest rally since the index was created in 1973 – and could pose significant headwinds to dollar-sensitive sectors of the market, particularly companies that respond to commodity prices affected by the greenback, and multinationals that do much of their business overseas.

“For the past few years, the U.S. dollar has been trading in a relatively quiet trading range. This summer, something changed. We are now seeing a new uptrend develop,” said Adam Sarhan, founder and CEO of Sarhan Capital in New York. Analysts have already pointed fingers at the dollar for the decline in prices of commodities like precious metals, corn and oil in recent weeks. U.S. multinationals with large streams of revenue from overseas also stand to lose.

[..] Much of the calculus of whether the dollar’s rise will become a net negative for U.S. stocks depends on domestic inflation rates, as well as the speed and scale of the currency’s gains, market watchers said. “The euro zone is fragile … the British pound is also weak, and geopolitical or economic woes remain a threat. As long as it is a healthy and normal advance, they should be able to adjust and prepare for it,” Sarhan said. “But if the move is very large, fast or erratic, those consequences [could] be immeasurable.”

Yes, something changed alright. Fed priorities did. Jim Rickards gives his view:

Jim Rickards: ‘World In Indefinite Depression’ (RT)

RT: The Chinese Central bank is now offering stimulus. Is this a part of a new round of “currency wars”?

Jim Rickards: Yes, that is right. I think this is one long “currency war”. We are now getting into more of a battle, more of a confrontation. The US dollar is the only strong currency that cannot last: the US cannot have a strong currency, because we are desperate for inflation. We have done all the quantitative easing, we have raised the zero, we have issued further guidance, we have done a twist, and we have done three versions of QE. We have done everything possible. The only thing left is to try to cheapen the currency and in fact the dollar is getting stronger.

The Fed might not have minded a stronger dollar: six months ago it did look like the economy was getting stronger. We saw strong second quarter GDP. So it was a little bit of a good day. And Europe was desperate for the help: they were stepping into recession. Japan`s economy collapsed in the second quarter. So you could see the feds saying “ok…we will have a stronger dollar and give Europe and Japan a break”. But that is over. Now the US is becoming a loser and we are the ones who need to take a break. The only way to get it is a cheaper dollar. I would look for that in the months ahead.

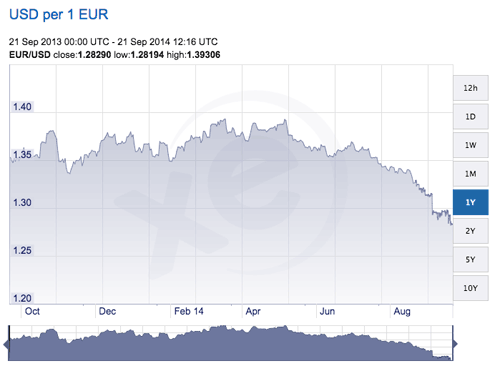

Jim, it’s not six months ago, it’s more recent than that. Look:

And the biggest drop was even over just the past month or so:

I know, this is the EUR/USD situation only, but that IS the most important data. What happens vs the yen is much less relevant, because Shinzo Abe is a desperate man willing do anything to beggar his currency. And China is too opaque to draw any conclusions from. Besides, the Euro is by far the biggest reserve currency behind the USD.

And after that, Jim, you’re just absolutely missing the mark. The rise of the dollar just got started. The Fed is not looking for a cheap dollar. Not anymore. You may argue that we’re watching a headfake, but it’s not that “the Fed might not have minded a stronger dollar”: they actively want a stronger dollar. For the same reason they want higher interest rates: the profits of Wall Street banks.

There are tens of trillions – mostly in US dollars – outstanding in interest rate derivatives. The mood in that camp has become as complacent, ‘Fed has my back’, as it has in stock markets. That means there are no profits there anymore. That’s what Minsky meant when he said that stable markets MUST lead to instability: it’s about profits. Stability will always only remain an illusion.

If and when the Fed takes its hands off the US dollar rate, da greenback will rise like crazy vs the Euro, go to par and probably beyond. And that would still only be normal, there’s no reason why they wouldn’t be at par. But it’s also a 30% move. And that sounds like the promise of real profits.

The Fed never sought to ‘protect’ Main Street or main investors, other than as something collateral, some sort of piggybacking. The big money going forward is in a higher dollar and higher interest rates. So that’s what we’ll have. There won’t be too many parties, big or small, gearing or hedging up for that, even if they have that flexibility, so it’s OK to give away a little of the game plan.

I’m not saying that I know all the details and ins and outs here, but I do think a lot of questions never get asked on this topic, and I do think the role the Fed plays is very poorly understood. The Fed has long given up on the US economy.