{kind=link}

Courtesy of Dana Lyons

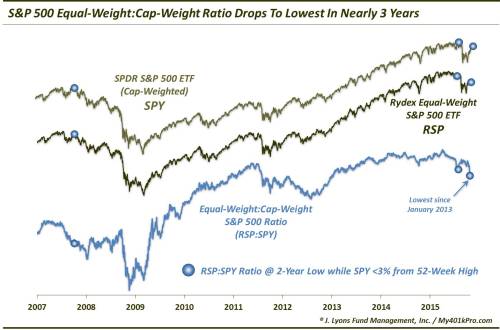

The “equal-weight” S&P 500 has dropped to near 3-year lows versus the cap-weighted version. Previous such events under similar conditions occurred at inauspicious times.

Continuing with the impromptu weekly theme regarding the relatively “thin” nature of the recent stock rally, today we take a look inside the S&P 500. Like yesterday’s post on the consumer discretionary sector, this one examines the “equal-weight version of the index versus the traditional cap-weighted version. Whereas the performance of the cap-weighted index can be subject to undue influence by the very largest components, a look at the equal-weight version can give us an idea of the health of the broad swathe of stocks within the index.

While the relative under-performance on the part of the equal-weight S&P 500 (as judged by the Rydex Equal-Weight S&P 500 ETF, RSP) may not be as egregious as in the consumer discretionary sector, it is still somewhat alarming. Despite the cap-weighted S&P 500 (as judged by the S&P 500 SPDR ETF, SPY) being reasonably close to its all-time highs again, the equal-weight:cap-weight ratio has dropped to near 3-year lows. Considering the context, the RSP:SPY ratio is at levels only seen just prior to substantial declines in July and back in 2007.

By “considering the context”, we mean that the cap-weighted S&P 500 is less than 3% from its all-time high. The only months, historically, that have seen the equal-weight:cap-weight (RSP:SPY) ratio at a 2-year low under those circumstances are shown below. Obviously, these did not mark the best months to be buying stocks.

- September-November 2007

- July 2015

- October 2015

Again, like we have mentioned throughout the week, this situation means that the inordinate bulk of the lifting during the recent rally is being done by the biggest of stocks. It does not necessarily mean that the rest of the stocks are falling or doing poorly. It just means that they’re not doing their fair share. As it turns out, on an equal-weighted basis, the indices have basically been drifting sideways during the most recent few weeks while the biggest stocks have been rallying smartly.

So is this a big deal? Well, in July it was. And in the fall of 2007 it was. Does this mean the market is on the verge of another collapse? Not necessarily. It doesn’t even mean that the rally cannot continue, for a time. It does mean that if one wants to participate on the long side, they are likely better suited being in those relatively few stocks or areas that are carrying the market at the moment.

That said, we are big proponents of good breadth as a sign of a healthy market. The more stocks that are participating in a rally, the better the foundation for the rally. Thus, when some, or a lot, of stocks invariably fall by the wayside, there are enough strong stocks to continue to carry the burden. When there are relatively few stocks doing all the heavy lifting, there is less margin for error.

Eventually, the weight will become too much to bear for just those few stocks. And, as we saw this summer, when those relatively few leaders begin to stumble, the market will again be vulnerable to significant damage.

* * *

More from Dana Lyons, JLFMI and My401kPro.