{kind=link}

Courtesy of Lance Roberts, Real Investment Advice

September 20, 2017 will likely be a day that goes down in market history.

It will either be remembered as one of the greatest achievements in the history of monetary policy experiments, or the beginning of the next bear market or worse.

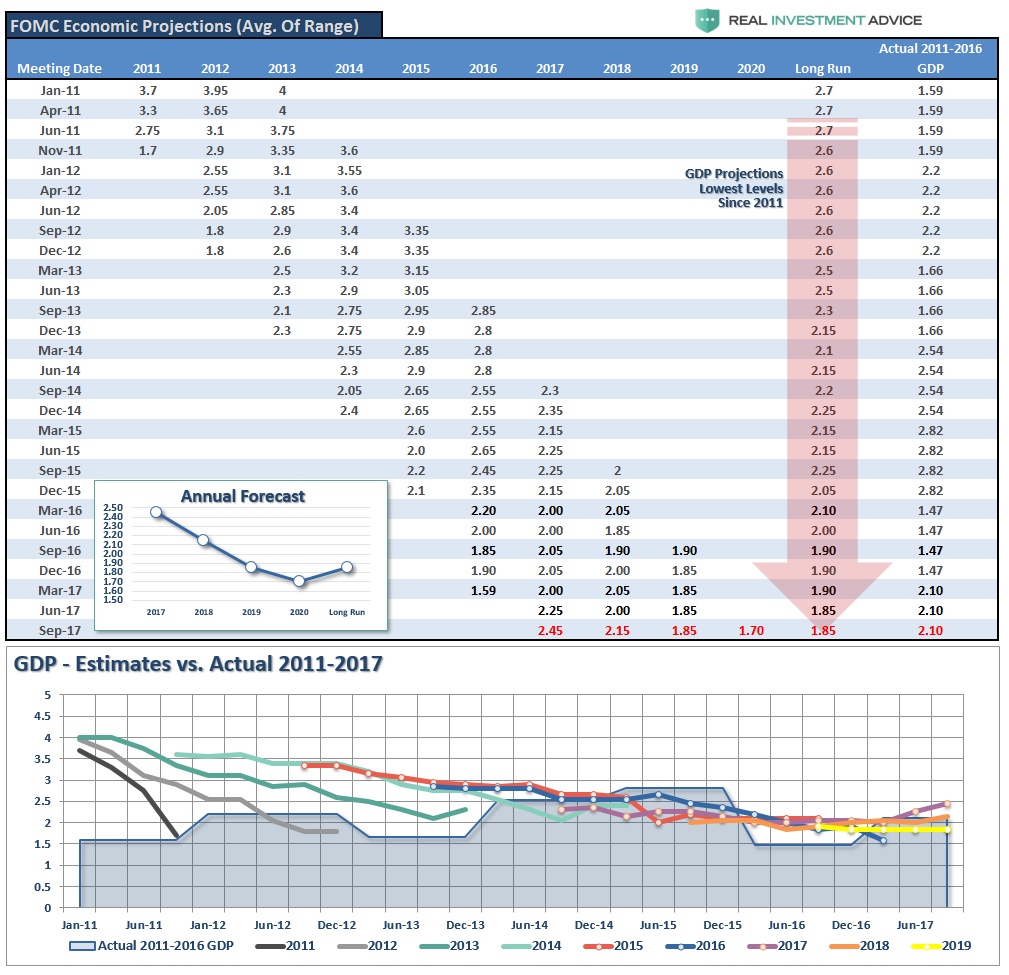

Given the Fed’s inability to spark either inflation or economic growth, as witnessed by their dismal forecasting record shown below, I would lean towards the latter.

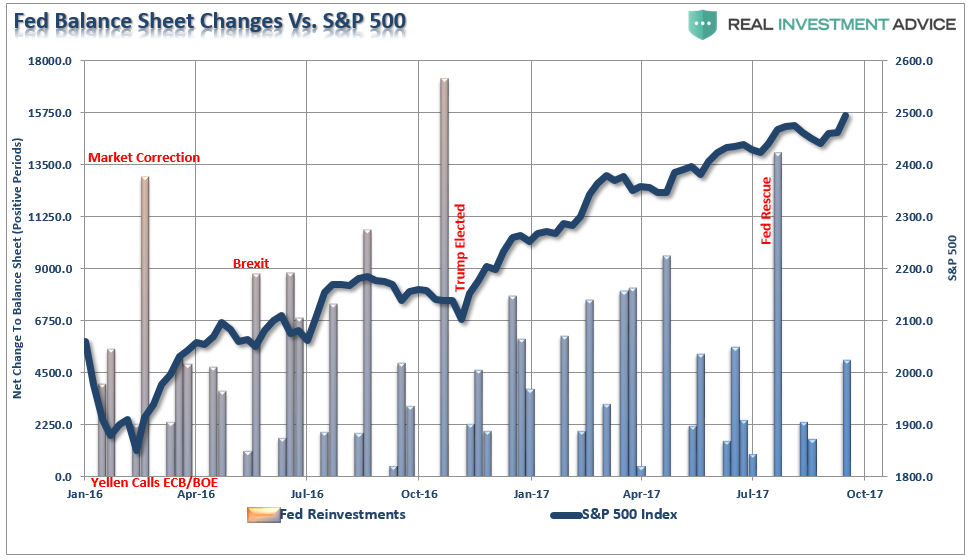

The media is very interesting. Despite the fact there is clear evidence that unbridled Central Bank interventions supported the market on the way up, there is now a consensus that believes the “unwinding” will have “no effect” on the market.

This would seem to be naive given that, as shown below, the biggest injections of liquidity from the Fed have come near market bottoms. Without the proverbial “punch bowl,” where does the “support” come from to stem declines?

I tend to agree with BofA who recently warned…” the paint may be drying but the wall is about to crumble.”

“This point can be summarized simply as follows: there is $1 trillion in excess TSY supply coming down the line, and either yields will have to jump for the net issuance to be absorbed, or equities will have to plunge 30% for the incremental demand to appear.”

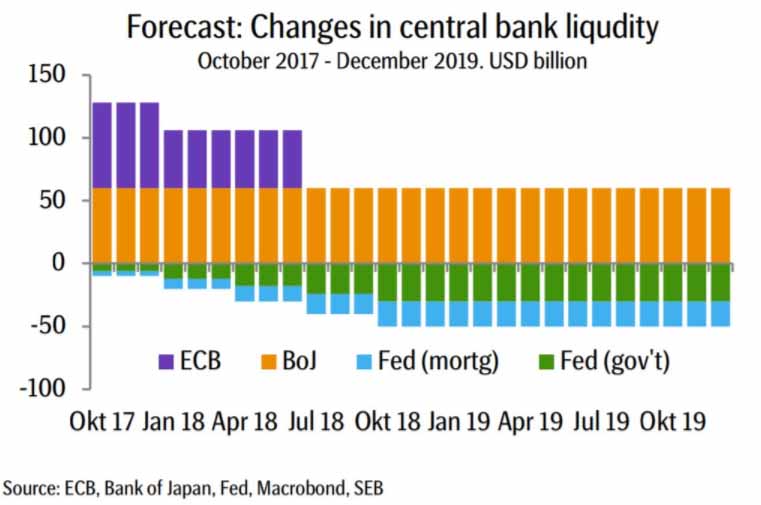

“An unwind of the Fed’s balance sheet also increases UST supply to the public. Ultimately, the Treasury needs to borrow from the public to pay back principal to the Fed resulting in an increase in marketable issuance. We estimate the Treasury’s borrowing needs will increase roughly by $1tn over the next five years due to the Fed roll offs. However, not all increases in UST supply are made equal. This will be the first time UST supply is projected to increase when EM reserve growth likely remains benign.Our analysis suggests this would necessitate a significant rise in yields or a notable correction in equity markets to trigger the two largest remaining sources (pensions or mutual funds) to step up to meet the demand shortfall. Again, this is a slower moving trigger that tightens financial conditions either by necessitating higher yields or lower equities.”

Of course, as I have discussed previously, a surge in interest rates would lead to a massive recession in the economy. Therefore, while it is possible you could experience a short-term pop in rates, the end result will be a substantial decline in equities as money flees to the safety of bonds driving rates toward zero.

“From many perspectives, the real risk of the heavy equity exposure in portfolios is outweighed by the potential for further reward. The realization of ‘risk,’ when it occurs, will lead to a rapid unwinding of the markets pushing volatility higher and bond yields lower. This is why I continue to acquire bonds on rallies in the markets, which suppresses bond prices, to increase portfolio income and hedge against a future market dislocation.”

My best guess is the Fed has made a critical error. But just as a “turnover” early in the first-quarter of the game may not seem to be an issue, it can very well wind up being the single defining moment when the game was already lost.

In the meantime, here is what I am reading this weekend.

Politics/Fed/Economy

- The Fed Is Peddling “Tinker Bell Economics” by Caroline Baum via MarketWatch

- What Did We Learn From The Fed by Tyler Durden via ZeroHedge

- The Fed Is On A Mission by Wolf Richter via Wolf Street

- Reform The Debt Ceiling by Maya McGuinness via Washington Post

- Politics & Your Portfolio, It’s Complicated by Joe Calhoun via RCM

- Why Are Economists Always So Wrong by Jeff Harding via An Independent Mind

- Senate Embraces $1.5 Trillion Tax Cut Plan by Rappaport & Kaplan via NYT

- Don’t Be Fooled By The Fed’s Magic Show by Brandon Smith via Alt-Market

- Free Health Care Is Very Expensive by Dan Mitchell via International Liberty

Markets

- When The Market Implodes, Don’t Say You Weren’t Warned by Shawn Langlois via MarketWatch

- Rogers: ETF Holders Will Get Mauled In Next Bear Market by Barbara Kollmeyer via MarketWatch

- This Is Your Last Warning by Thomas Kee via MarketWatch

- Mass Psychology Is Driving The Market by Robert Shiller via NYT

- The Everything Bubble Is Ready To Pop by Jared Dillian via Mauldin Economics

- Little Things Mean A Lot by Cliff Asness via AQR Capital Management

- Investor Returns: The Failure Endures by James Picerno via Capital Spectator

- 4-Charts Could Signal Markets End by Michael Kahn via Barron’s

- Buffett Predicts DOW 1,000,000 In 100-Years by Tyler Durden via ZeroHedge

- Key Lessons From 2nd-Longest Bull Market by Sue Chang via MarketWatch

- Stock Market Bubbles In Perspective by Howard Mia via Meritocracy Capital

- The Folly Of Hiring Winners & Firing Losers by Rob Arnott via Research Affiliates

- Ways To Navigate An Aging Bull Market by Michael Brush via MarketWatch

- Scent Of Group Stink As Strong As It Was In 2000 & 2007 by Doug Kass via RIA

- Bull Market Depends On The Fed by Mark DeCambre via MarketWatch

Research / Interesting Reads

- The Alarming Implications Of The Equifax Breach by The Economist

- 5-Common Mental Errors by James Clear

- The Case For Stock Buy Backs by Harvard Business Review

- Why Is Value Investing So Difficult by Behavioral Investment

- AI Can Listen To Earnings Calls Better by Institutional Investor

- The Death Of Active Management Is Greatly Exaggerated by Jeff Troutner via Index Funds

- Forget Full-Time Work, Gigs Can Be Safer by Simon Constable via Forbes

- Mauldin: The Pension Crisis Is Coming by John Mauldin via Zerohedge

- Big Brother Is Coming For BitCoin by James Rickards via Daily Reckoning

- BitCoin Is Probably Worth ZERO by James Mackintosh via WSJ

- SEC Admits EDGAR System Was Hacked by Tyler Durden via ZeroHedge

- Walking Into A 2007-08 Scenario by John Hussman via Hussman Funds

- A Silver Lining In Precious Metals Sell-Off? by Dana Lyons via Tumblr

- All You Need To Know About The Fed In Two Charts by Jesse Felder via The Felder Report

“If you are playing the rigged game of investing, the house always wins.” ~ Robert Rolih