{kind=link}

Courtesy of Lance Roberts, Real Investment Advice

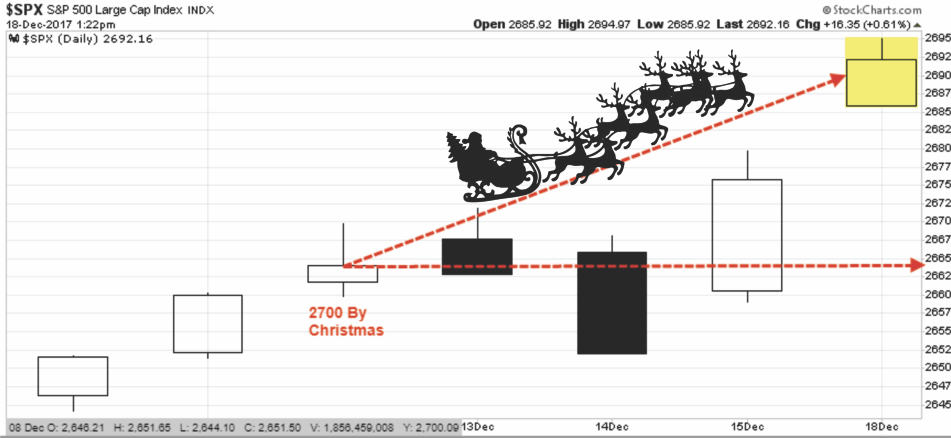

In last week’s Technical Update, I discussed the potential for the S&P 500 to hit 2700 by Christmas:

“The current momentum behind the market advance is clearly bullish, and with the ‘smell of tax reform’ in the air, there is little to derail the bulls before year-end.

However, in the meantime, there seems to be nothing stopping the market from going higher. As stated in the title, the current push higher puts 2700 in sight by the time Santa fills the ‘stockings hung by the chimney with care.'”

With the markets within striking distance of that target, the run to Nasdaq 7000, Dow 25000 and S&P 2700 are all but guaranteed at this juncture. More interestingly, all three will be ticking off milestone gains at some of the fastest paces in market history. In fact, the Dow has posted three all-time records just this year:

- 70 new highs,

- A 5000-point advance in a single year, and;

- 12-straight months of gains.

Just as a reminder of previous market bubbles, here is what they looked like.

As I discussed with Danielle Dimartino-Booth this morning. Not only is the current rally reminiscent of 1999, but to 2007 as well. In fact, the current bubble, as she states, is a combination of both.

As Danielle and I discussed, it seems eerily familiar.

In 1999:

- Fed was hiking rates as worries about inflationary pressures were present.

- Economic growth was improving

- Interest and inflation rates were rising

- Earnings were rising through the use of “new metrics,” share buybacks and an M&A spree. (Who can forget the market greats of Enron, Worldcom & Global Crossing)

- Margin-debt / leverage was at the highest level on record.

- Stock market was beginning to go parabolic as exuberance exploded in a “can’t lose market.”

- Speculative asset of choice: Dot.com stocks

In 2007:

- Fed was hiking rates as worries about inflationary pressures were present.

- Economic growth was improving

- Interest and inflation rates were rising

- Debt and leverage provided a massive “buying” binge in real estate creating a “wealth effect” for consumers and high-valuations were justified because of the “Goldilocks economy.”

- Margin-debt / leverage was at the highest level on record.

- Stock market was beginning to go parabolic as exuberance exploded in a “can’t lose market.”

- Speculative asset of choice: Real Estate

In 2017:

- Fed was hiking rates as worries about inflationary pressures were present.

- Economic growth is improving because of 3-hurricanes and 2-wild fires.

- Interest and inflation rates are expected to rise

- Earnings were rising through the use of “new metrics,” share buybacks and an M&A spree.

- Margin-debt / leverage is at the highest level on record.

- Stock market was beginning to go parabolic as exuberance exploded in a “can’t lose market.”

- Speculative asset of choice: Bitcoin

Of course, those are just some of the similarities.

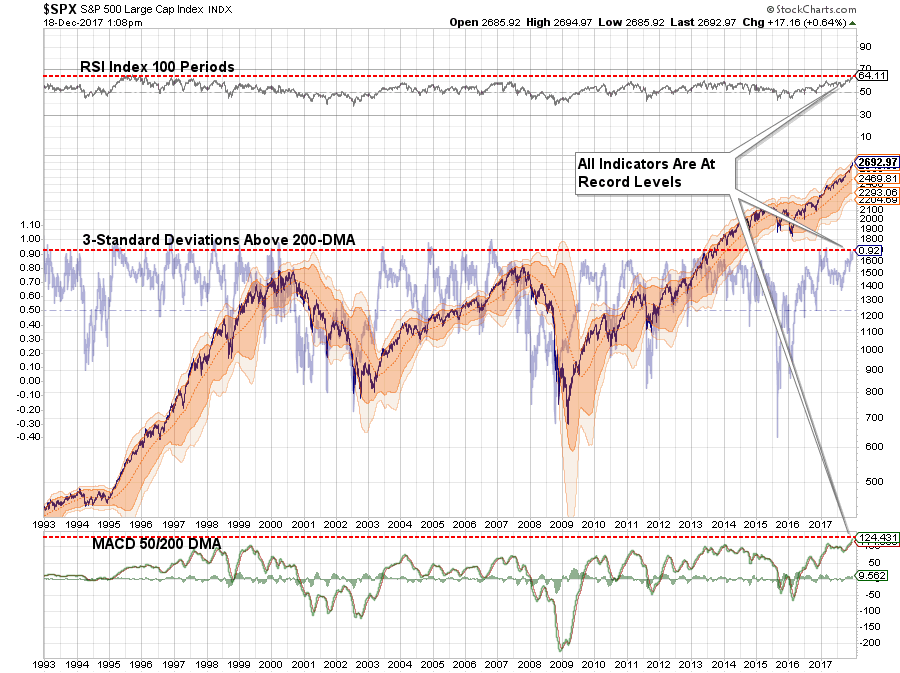

Valuations in all three cases exceeded the long-term market peaks of 23x reported earnings. Investor confidence was pushing extremes and deviations from long-term means in prices, relative-strength and moving-averages were all present.

The chart below shows the S&P 500 from 1993-present. As shown, the 100-period RSI, 3-standard deviations above the 200-dma and the 50/200 day moving average MACD line are all at historical extremes. While such readings do NOT suggest a downturn is imminent, it does suggest that risk is elevated and potential upside from current levels is likely limited.

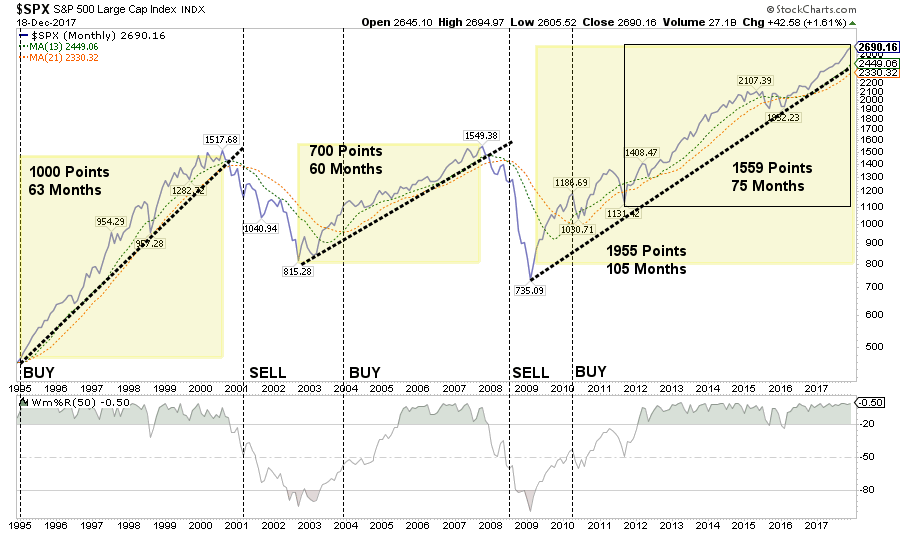

I have combined the three periods below, scaled to 100, so you can see just how far we have currently gone.

Sure. This time could be different. It just probably isn’t.

Our Job As Investors

Again, none of this suggests the market is going to crash tomorrow. But a massive mean reversion process is coming, it is inevitable, the only question is of the timing.

As I noted last week in “The Exit Problem,” it is time to start considering sitting a little closer to the “exit.” To wit:

“Am I sounding an ‘alarm bell’ and calling for the end of the known world? Should you be buying ammo and food? Of course, not.

However, I am suggesting that remaining fully invested in the financial markets without a thorough understanding of your ‘risk exposure’ will likely not have the desired end result you have been promised.

As I stated often, my job is to participate in the markets while keeping a measured approach to capital preservation. Since it is considered ‘bearish’ to point out the potential ‘risks’ that could lead to rapid capital destruction; then I guess you can call me a ‘bear.’

Just make sure you understand I am still in ‘theater,’ I am just moving much closer to the ‘exit.’”

What does that mean?

I have now been in the financial markets in some capacity since prior to the crash of 1987.

Yes, I am that old.

During that time I have watched investors repeat the same mistakes over and over again. From exuberance to fear, buying high to selling low, chasing returns, and always believing this time is different, only to once again be reminded it’s not.

As the old saying goes:

“The more things change, the more they remain the same.”

If you have been around the markets for any length of time, you can quickly spot the “pigeons at the poker table.” These are the ones that continually rationalize why prices can only go higher, why this time is different than the last, and only focus on the bullish supports. Trying to “draw to an inside straight” is not impossible, it just leads to losses more often than not.

But therein lies an important point.

As investors, our job is NOT making the case for why markets will go up.

Read that again.

If the markets rise, terrific. We all made money, and we are the better for it. However, that is not our job.

Our job, is to analyze, understand, measure, and prepare for what will reduce the value of our invested capital.

Period.

If we are to accumulate capital over the time-span that we have available, from today until we reach retirement, the most important thing we can do to ensure our success is not suffering a large loss of capital.

Therefore, our job as investors is actually quite simple:

- Capital preservation

- A rate of return sufficient to keep pace with the rate of inflation.

- Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

- Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

With forward returns likely to be lower and more volatile than what was witnessed in the 80-90’s, the need for a more conservative approach is rising. Controlling risk, reducing emotional investment mistakes and limiting the destruction of investment capital will likely be the real formula for investment success in the decade ahead.

This brings up some very important investment guidelines that I have learned over the last 30 years.

- Investing is not a competition. There are no prizes for winning but there are severe penalties for losing.

- Emotions have no place in investing.You are generally better off doing the opposite of what you “feel” you should be doing.

- The ONLY investments that you can “buy and hold” are those that provide an income stream with a return of principal function.

- Market valuations (except at extremes) are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading. Knowing what type of investor you are determines the basis of your strategy.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

As an investment manager, I am neither bullish or bearish. I simply view the world through the lens of statistics and probabilities. My job is to manage the inherent risk to investment capital. If I protect the investment capital in the short term – the long-term capital appreciation will take of itself.