{kind=link}

Only $84Bn?

Only $84Bn?

That's right folks, Apple (AAPL) issued a rare warning last night as CEO, Tim Cook said trade wars (including a Chinese boycott of Apple) have hurt even the World's Greatest Company and they would "only" sell $84Bn in their Q1 (normal people's Q4) which is $9Bn (10%) less than the high end of guidance. AAPL also guided gross margin lower, to 38% so we can now whip out our iPad Calculator and say $84Bn x 0.38 = $31.92Bn in gross profit which is – GASP!!! – almost $2Bn less than they earned last year in Q1. OMG – SELLSELLSELL!!!!

That was sarcasm, of course – we're buying. $84Bn is $4Bn less sales (5%) than last year and $2Bn less profit is 6% lower and of course we don't like to see our companies taking steps backwards but this is another one of those self-inflicted wounds Trump is causing to our economy and Apple is the biggest company in our economy – so of course they are going to feel some pain.

We already took a long position on the Nasdaq Futures (/NQ) at 6,200 in our Live Member Chat Room as I put out a note at 4:55 am. Clearly the sell-off is an over-reaction that has no basis in reality, but that won't stop AAPL from going lower as idiot analysts jump on the bandwagon and downgrade it – we will just have to be patient. The Nasdaq drifted along around 6,200 until just about 7am, when it blasted higher, to 6,250 for a quick $1,000 per contract gain – a nice way to start our day!

I'm not going to make a case for AAPL as it's boring, I was bored back in May when AAPL droped from $181 to $158 on "disappointing" earnings – which did a good job of flushing out the retail suckers before they blasted to $232 on the July earnings report. You really can fool some of the people all of the time and all of the people some of the time – especially when they are Apple traders! Of course when hedge funds need a boost, they like to load up on big stocks like AAPL but how do they get them to be cheaper? We JUST had this discussion in yesterday's Webinar and today is a great example of that end game as this is the big flush to get you out of Apple so the Banksters can back up the truck under $150.

Remember – "THEY" can't buy the stock if you are holding onto it so "THEY" have to get you to sell it and you've been set up for weeks with rumors of disappointing iPhone sales which were partly true (as all the best rumors are) and now is the denouement, where the Banksters and Fund Manages shout "SEE – DISASTER!" on what is essentially a 5% guide-down from record profits.

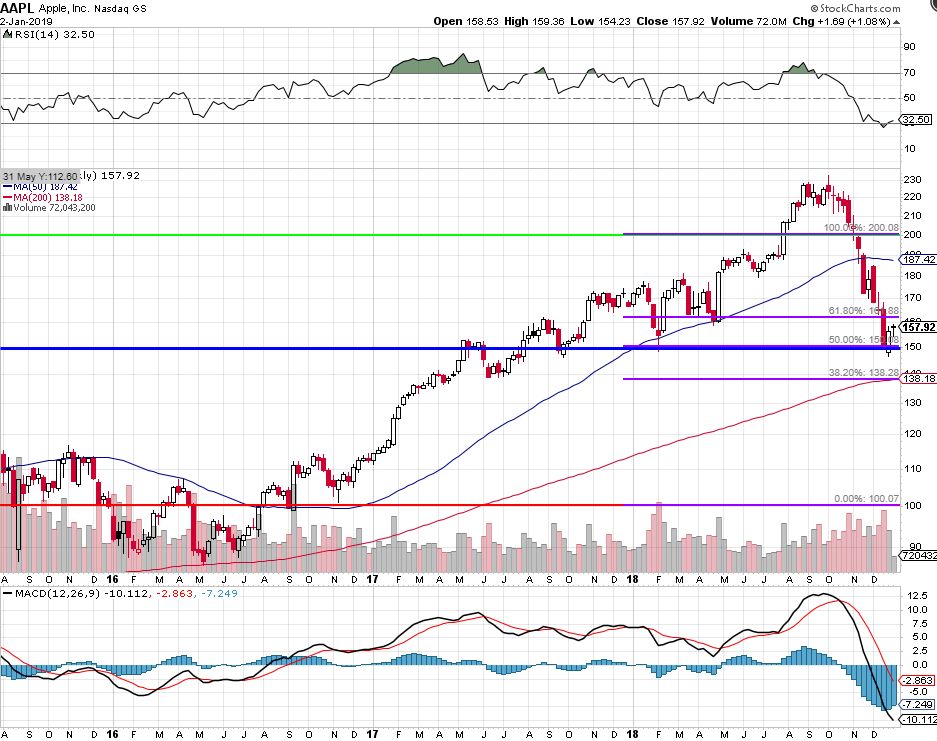

Notice, on the chart above, that AAPL should have good support at $140, which is the 200-day moving average and the MACD line (bottom of chart) shows that they are already tremendously oversold but Cramer is on CNBC right now (8:55 am) saying AAPL can fall to $120 not because he's just another moron jumping on the negative bandwagon but more likely because he wants YOU to sell your AAPL stock, even at $145, in order to enrich his Bankster Buddies – who sponsor his show – where the main purpose seems to be moving Retail Suckers in and out of positions like lemmings to proivde easy marks for Cramer's hedge fund buddies.

Here's Cramer telling you exactly how he manipulates stocks:

That's how the game works people – we were just talking about it yesterday in the Live Trading Webinar and here's a great homework example for you to study. As I've been saying all year – these are self-inflicted wounds that can be "fixed" in an instant if Trump shakes hands with Xi and re-opens the Government. Will that happen? Who knows – that's why we have hedges but now that there are adults in charge of Congress, we can be pretty sure things won't get much worse as someone finally has the power to reign in Trump and his mad scemes which, so far, have brought us nothing but pain.

Since the Trade War hurts the farmers and the Midwestern manufacturers, including the Kochs – it won't be long before Trump's own party turns against him so the pressure will mount on him to capitulate and, hopefully, things can get back to "normal" and THEN we will find out what things are really worth.

Speaking of what things are worth, we thought Celgene (CELG) was way too low (like AAPL is) back in July and we added the following spread to our Short-Term Portfolio:

| Long Call | 2019 18-JAN 90.00 CALL [CELG @ $66.64 $0.00] | 10 | 7/25/2018 | (15) | $6,000 | $6.00 | $-5.97 | $6.00 | $0.04 | $0.02 | $-5,965 | -99.4% | $35 | ||

| Short Call | 2019 18-JAN 100.00 CALL [CELG @ $66.64 $0.00] | -10 | 7/25/2018 | (15) | $-2,700 | $2.70 | $-2.68 | $0.03 | $0.02 | $2,675 | 99.1% | $-25 | |||

| Short Put | 2020 17-JAN 85.00 PUT [CELG @ $66.64 $0.00] | -5 | 7/25/2018 | (379) | $-4,600 | $9.20 | $11.58 | $20.78 | $-0.35 | $-5,788 | -125.8% | $-10,388 |

When we did the review on Dec 12th, we had given up on the Jan spread. My comment to our Members was:

- CELG – Well, this one fell apart. We're going to take the loss next month but we won't wait to set up a position in the LTP, effectively "rolling" from the STP to the LTP, which is one of the ways we kind of transfer funds to the LTP, taking the speculative loss here and setting up the cheaper long-term position there (this works from taxable accounts to IRAs as well).

- Sell 10 CELG 2021 $70 puts for $11 ($11,000)

- Buy 20 CELG 2021 $60 calls for $21 ($42,000)

- Sell 20 CELG 2021 $80 calls for $11.50 ($23,000)

That's net $8,000 on the $40,000 spread that's 50% in the money to start so think about that, for $8,000 we're getting a position at $71.50 that's $23,000 in the money. Don't you just love options?!

In the STP, we took pokes at MJ and CELG as short-term plays and it would have been nice if they popped but they didn't and we took a $7,500 loss on CELG and an $8,000 loss on MJ so the loss is booked in the STP so, if it were a taxable account – tax losses, while the gains will show up in the LTP, which could be the IRA account.

That's another way scaling into positions can work very much to your advantage.

This morning, BMY put in an offer to buy CELG at $100/share, which happens to be our target. Pre-market, CELG is at $90 already (from $66) so not only is our new trade going to make the full $32,0000 way ahead of schedule but we may also have a win on the original tade.

Congratulations to all who played!