By Jacob Wolinsky. Originally published at ValueWalk.

Prescience Point is short Enphase Energy (“ENPH” or the “Company”) because we believe the Company’s financial statements filed with the SEC are fiction.

Q1 2020 hedge fund letters, conferences and more

Based on the findings of our thorough, on-the-ground investigation of Enphase Energy’s India operations and our detailed analysis of the company’s accounting and business practices, we believe that at least 39%, or $205.3 million, of ENPH’s reported U.S. revenue is fabricated. Based on statements provided by former employees and other solar industry participants, it appears that the Company inflated its international revenue significantly as well. We also believe that most, if not all, of the enormous 2,080 Bps expansion in the Company’s gross margin during Kothandaraman’s tenure as CEO – from 18.4% in Q2 2017 to 39.2% in Q1 2020 – is fiction. Finally, based on their frantic and massive share sales from June 1st to June 15th, it appears that ENPH executives and board members learned of our private investigation, which wrapped up at the end of May, and are desperately trying to unload their shares before the ship sinks.

We believe government bodies with subpoena power should investigate ENPH, its independent auditors should launch an in-depth investigation of the Company’s accounting practices, and the Board of Directors should establish an independent committee to examine the findings and analyses presented in this report.

Enphase Energy – Target Price: Delisted

Former Enphase Energy Employee #1: The current market position attained by the company and its stellar revenues are all thanks to inflated numbers…From my vantage point, it appears that the entire efforts are on to pump up the revenues, push up the stock price, cash in and milk the cow dry, before this company too hurtles the SunEdison way towards bankruptcy….

Former Enphase Energy Employee #2: There was a strong rumor in the company last year that this growth is largely unrealistic and manipulated. The business has undoubtedly grown over the 2018-19 cycle…But most employees that I spoke to told me that the numbers just don’t add up

Former Enphase Energy Employee #3: Per the GAAP, these deferred revenues should be in the liabilities corner of the balance sheet. But what Yang and Eric under Badri Kothandaraman are doing is overstating income by treating deferred revenue as earned revenue by recognizing revenue before it is actually earned…It is like a pyramid scheme which cannot stop, and if it does, the entire accounting process will completely unravel…there were many questions I asked about the deferred revenue system which to me were appearing to be extra ordinary accounting practices……(I) was told to shut up and comply…

Prescience Point Research Opinions:

- At least $205.3m of ENPH’s reported FY’19 US revenue is fabricated, and a significant portion of its international revenue is fabricated as well

- Most, if not all, of the 2,080 Bps expansion in ENPH’s gross margin since Q2’17 is also fabricated

- Deloitte should launch an in-depth investigation of ENPH’s accounting practices

- Regulatory and law enforcement agencies with subpoena power should launch a full investigation of the Company, its accounting, its disclosures and trading by insiders

- The Board of Directors should establish an independent committee to examine the findings and analyses presented in this report

Research Highlights:

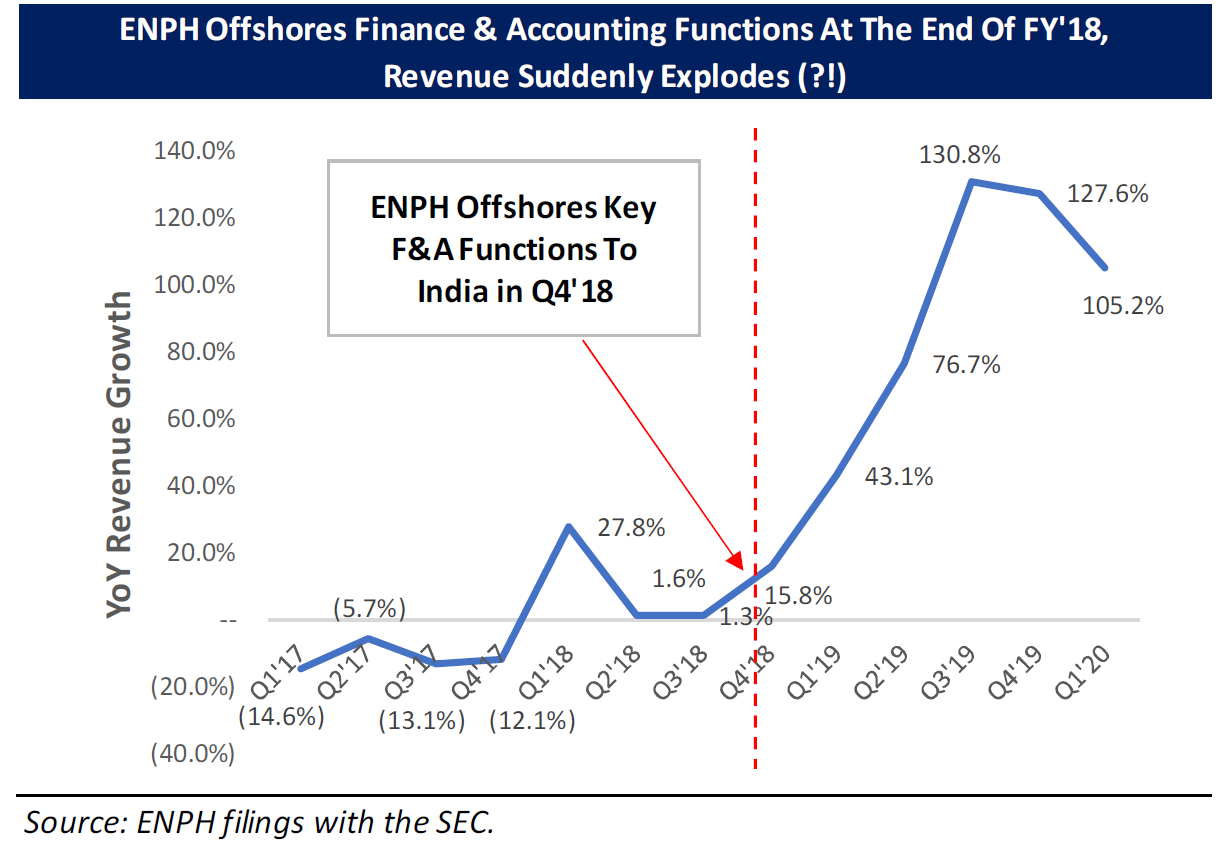

- At the end of FY’18, ENPH curiously offshored key finance & accounting (“F&A”) functions to India

- According to former employees based in India, ENPH is using its offshore F&A team to assist in cooking the Company’s books at the direction of US executives

- ENPH has stacked its executive teams in both the US and India with numerous loyal, former colleagues from Cypress and SunEdison, seemingly to create an environment conducive to fraud

- According to former employees, Ahmad Chatila, the disgraced former SunEdison CEO, is working behind-the-scenes for ENPH and is alleged to be “running the show from the sidelines at Enphase”

- Almost all the former employees our investigators spoke with either claimed or believed that ENPH’s financials are fiction. Numerous current employees are alleged to be similarly skeptical

- According to former employees, a significant portion of ENPH’s astronomical growth over the past two years is attributable to improper deferred revenue accounting practices

- According to an employee of a distributor in India, his/her company severed its ties with ENPH based on its belief that ENPH was working directly with installers to fraudulently inflate invoices

- According to a solar industry participant in India, employee turnover in ENPH’s Bangalore office is an astronomical 70% annually – this is a clear symptom, in our view, of ENPH’s alleged book cooking and apparently toxic work culture

- ENPH’s largest shareholder suspiciously sold his entire 11% stake in the span of just one day on May 22nd, 2020 which is right around the time our private investigation was concluding. We believe he sold because he learned of the existence our private investigation.

- Enphase Energy executives and board members appear to have caught wind of our private investigation as well, based on their urgent sale of a massive 2.4m shares, amounting to $120.9m, in open market dispositions in a span of just 15 days from June 1st, 2020 to June 15th, 2020 – an admission of guilt?

- The nearly impossible reduction in ENPH’s unit costs or cost of revenue / watt from Q3’18 to Q3’19 of 23.6%, or 37.6% on a tariff-adj. basis, amounts to proof, in our view, that the Company’s reported gross margin is just as, if not more, inflated than its revenue

- Wood Mackenzie data shows that ENPH’s market share declined by 518 Bps from 25.4% in FY’17 to 20.3% in FY’19, which directly contradicts the parabolic revenue growth ENPH has reported – proof, in our view, that its reported revenue is grossly inflated

- Large distributors of ENPH products in the US, accounting for an estimated 69.5% of the distributor market, reported growth in ENPH product sales and market share changes which were far below and did not align with the Company’s reported US revenue growth – yet more proof, in our view, that ENPH’s reported revenue is grossly inflated

- Egregious accounting discrepancies and irregularities in ENPH’s financial reports amounts to proof, in our view that its revenue

and gross margin in Q1’18 and Q2’18 were significantly inflated by improper deferred revenue accounting - In 2018, ENPH apparently acquired ActivStor, which was a startup co-founded by one of its own employees – a Cypress and SunEdison alum who also attended the same college as CEO Kothandaraman. Alarmingly, this transaction was not disclosed in ENPH’s SEC filings, and the amount paid for this acquisition was completely excluded from its financial statements

- ENPH’s deferred revenue accounting in Q4 2019 and Q1 2020 does not appear to reconcile with GAAP

- ENPH’s reported safe harbor revenue from Q3’19 to Q1’20 of $88.9m was suspiciously large and is almost double the amount reported by competitor SolarEdge on a % of revenue basis

- SEDG’s former CEO and a mainstream financial journalist recently called ENPH’s revenue growth into question

- Former CFO Bert Garcia suddenly resigned in June 2018, right around the time when ENPH’s apparent fraudulent accounting practices appear to have begun

Introduction

Prescience Point is short Enphase Energy (“ENPH” or the “Company”) because we believe the Company’s financial statements filed with the SEC are fiction. Based on our research, we estimate that at least $205.3m of its reported US revenue in FY 2019 was fabricated. Based on statements provided by former employees and other solar industry participants, it appears that the Company inflated its international revenue significantly as well. We also believe that most, if not all, of the enormous 2,080 Bps expansion in the Company’s gross margin during Kothandaraman’s tenure as CEO – from 18.4% in Q2 2017 to 39.2% in Q1 2020 – is fiction. We believe government bodies should investigate ENPH, Deloitte should launch an in-depth investigation of the Company’s accounting practices, and the Board of Directors should establish an independent committee to examine the findings and analyses presented in this report.

In our initial reports on ENPH published in 2018 (here, here), we provided what we believed to be proof that ENPH had used improper deferred revenue accounting to significantly inflate its reported revenue and gross margins. Unfortunately, our warnings fell on deaf ears, and in the almost two years since our initial report, ENPH’s share price has continued to skyrocket as its reported financial performance has become increasingly disconnected from reality.

A breakthrough in our research of Enphase Energy occurred in late 2019 when we were told by a former ENPH employee that the Company had, peculiarly, offshored many of its key finance and accounting (“F&A”) functions to its India-based office in late 2018. As past accounting scandals have shown, offshore entities can and have been used as a tool to help companies perpetrate fraud. Given this, and our previous reservations about ENPH’s accounting practices, we viewed this as a significant red flag that warranted further investigation.

To learn more about Enphase Energy’s India-based operations, we hired a reputable third-party private investigation firm to conduct on-the-ground research in India. During its weeks-long investigation, our private investigators spoke with numerous former ENPH employees and solar industry participants based in India. The findings of this investigation confirmed our suspicions and uncovered numerous troubling revelations about the Company’s accounting and business practices. These findings include the following:

- According to former employees, ENPH is using its India-based F&A team to assist the Company in carrying out its allegedly fraudulent accounting practices, under the direction of the US executive team

- Enphase Energy has stacked its executive teams in both the US and India with numerous close, former colleagues from Cypress and SunEdison, seemingly for the purpose of creating a team of ‘yes-men’ and an environment conducive to fraud. These hires troublingly include Ahmad Chatila, the disgraced former SunEdison CEO, who is purportedly working behind-the-scenes for ENPH and has a considerable amount of influence within the Company

- Almost all of the former employees our private investigators spoke with either claimed or believed that the Company’s financial performance was fabricated. Our investigators were also told that numerous current employees are similarly skeptical about ENPH’s reported financials

- According to former employees, a large portion of the Company’s astronomical growth over the past two years is attributable to improper deferred revenue accounting practices which appear to have become more severe since our initial reports. Furthermore, according to an employee of an Enphase Energy distributor in India, his/her company severed its relationship with ENPH based on its belief that ENPH was circumventing them and working directly with installers to fraudulently inflate invoices.

- According to an industry participant with knowledge of Enphase Energy’s India-based operations, employee turnover in the Company’s Bangalore office is an alarming 70% annually. We believe ENPH’s apparent book cooking and toxic work culture is likely the driving force behind the mass exodus of its India employees.

Meanwhile, Enphase Energy executives and board members, as well as its previous largest shareholder, appear to have learned of the existence of our private investigation and are desperately trying to unload their shares before the ship sinks. In the span of just four days from June 1st, 2020 to June 4th, 2020, ENPH executives sold an unprecedented 254,097 shares worth a whopping $13.7m in open market dispositions, which significantly exceeds the 187,508 or $3.9m worth of shares ENPH executives had sold in the almost 2.5 years prior. Additionally, board member TJ Rodgers sold an astonishing 2.0m shares worth $98.1m, representing almost 60% of his total holdings, in open market dispositions in the span of just four days from June 8th, 2020 to June 11th, 2020. Furthermore, Ben Kortlang disposed of 180,000 ENPH shares worth $9.0m, representing a whopping 65% of his total holdings, in open market dispositions in the span of just one day on June 15th. Lastly, Chilean entrepreneur Isidoro Quirogo, who was ENPH’s largest shareholder with an ~11% stake worth more than $800m, sold his entire investment in the span of just one day on May 20th, 2020.

Suspiciously, these frantic and unprecedented share sales by ENPH executives, ENPH board members, and Quirogo occurred within days of the completion of our private investigation in late May. We do not believe this is a coincidence. Instead, we believe that these parties caught wind of our private investigation and were in a panicked rush to dump $millions of shares and cash-in before our findings were made public, indicating that the troubling findings of our private investigation are accurate.

But wait, there’s more. Our further diligence of Enphase Energy went far beyond our private investigation and included a thorough examination of ENPH’s reported financial statements and disclosures, conversations with several solar industry experts, conversations with the largest distributors of ENPH products and an examination of solar industry datasets and other online information sources. From this additional research and analysis, we uncovered multiple, additional smoking guns and numerous other red flags which, in our view, confirm that ENPH’s financials are fabricated and grossly inflated. The additional smoking guns we uncovered include,

- the nearly impossible reduction in Enphase Energy’s unit costs or cost of revenue per watt from Q3 2018 to Q3 2019 of 23.6%, or 37.6% on a tariff-adjusted basis, which puzzlingly occurred during the same time period that Section 301 tariffs of 25% were levied on ENPH’s microinverters. We cannot recall ever seeing a company reduce its manufacturing / unit costs by such a large amount in such a short period of time.

- the data we received from large MLPE distributors in the US, accounting for an estimated 69.5% of the distributor market, who reported growth in ENPH product sales and market share changes which were far below and did not align with the Company’s reported growth,

- the large disconnect between Wood Mackenzie MLPE market share data, which shows that Enphase Energy’s market share of US residential solar installations actually declined by 518 Bps from FY 2017 to FY 2019, and the more than doubling in ENPH’s reported US revenue during that same timeframe. When asked to provide a reason for this large discrepancy, representatives from Wood Mackenzie could not provide one, and instead pointed us to a recent Financial Times article that called into question ENPH’s reported revenue growth. and

- egregious accounting irregularities and discrepancies which, in our view, confirm that ENPH used improper deferred revenue accounting to significantly inflate its financial performance in Q1 2018 and Q2 2018

Following the publishing of our initial reports, Enphase Energy management successfully explained away the egregious accounting issues we uncovered to its auditors, as evidenced by Deloitte’s baffling decision to issue an unqualified audit opinion in both FY 2018 and FY 2019. However, given the overwhelming evidence of fraudulent behavior presented in this report, which is backed by numerous former employees, numerous solar industry participants, a forensic accountant, and reliable third-party data sources, we believe that this time will be different, and that this sham turnaround story will soon meet its inevitable, dire fate.

We hope that current and future investors and creditors familiarize themselves with the risks we have addressed and take immediate action to preserve the value of their holdings. We also hope that the NASDAQ, regulatory agencies, and Deloitte take action to protect investors. We believe that the SEC and Deloitte should launch a full-scale investigation into Enphase Energy’s accounting and business practices.

Read the full article here by Prescience Point Capital Management

The post Enphase Energy Inc (ENPH) – Significant Evidence of Fraud? appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}