By Jacob Wolinsky. Originally published at ValueWalk.

Guardian Fund commentary for the year ended December 31, 2020.

Q4 2020 hedge fund letters, conferences and more

“Deep in the woods I recall a fable once told, by the tallest trees and creatures of old, ‘behold the light’ they said, ‘for the night is cold and all that glitters is not gold’.” – Aesop

Dear Partner,

Guardian Fund Performance

In 2020, the return of the Guardian Fund was +52.21%, measured in euros and net of fees and expenses. This compares to 18.40% for the S&P 500 Index, measured in U.S. dollars, and including dividends.

In 2020, the return of our Tech Fund – the satellite fund we founded in 2018 for Guardian investors who like to have a more concentrated investment in a handful of rapidly growing software businesses which are part of the Guardian Fund’s portfolio – was +127.76%, net of fees and expenses.

Last year, the U.S. dollar depreciated by 9% versus the euro thereby providing a slight headwind for our returns in 2020.

Two thousand and twenty has been a strong year for our businesses, and it is our conviction that we are just getting started as the companies we own are only in their early stages of capturing the opportunity right in front of them.

The digitalization of our lives will unlock and create trillions of dollars in value and continue to drive a tectonic shift of wealth within society. It is our mission to participate in the thriving winners of our time.

The opportunity to significantly grow our wealth by owning exceptional businesses has never been better since I launched the Guardian Fund over a decade ago; A number of coinciding factors enable businesses of a certain nature to achieve exponential growth and sustain it for a long time.

Investing in Thriving Businesses

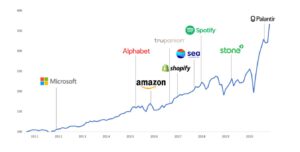

When the Guardian Fund was started in 2010, Facebook, Shopify, Spotify, and many other companies which are now part of our daily lives, were small private firms. Microsoft had a market value of only USD 220 billion (versus USD 1.6 trillion now); Instagram was founded two months later in October 2010; and Snowflake, at a USD 76 billion market value today, was founded two years later in 2012.

In 2010, merchants had a store and sometimes also a website. In the old world, people stored data on their own servers within their own castle and tried to defend the moat from security breaches with a team of dedicated in-house employees, who spent their working lives in the same building. We purchased CD’s to run Microsoft Office or to enjoy movies and music while I was searching for cheap stocks because that was what ‘value’ investors were supposed to do. In retrospect, my ignorance of what was going on at the time even at a great business like Amazon.com was enormous.

Looking back at the past decade, it is incredible how much more relevance software has gained. For the past few years, the ruling theme in software has been the migration of on-premises workloads to the cloud infrastructure of Amazon, Microsoft, and Google, as well as the proliferation of software-as-a-service (SaaS) applications running on top of those clouds. Business models changed as Microsoft, Adobe, Autodesk, amongst many others, transitioned from selling one-time licenses to monthly subscriptions for essential software.

The cloud infrastructure which these giants built, now enables any person to have an immediate scalable architecture and access to enormous computing power. A Cambrian Explosion of data driven software companies emerged that are revolutionizing the world by providing affordable enterprise quality software to any person. For instance, Shopify, Square, Stone, and Stripe have lowered the threshold for individuals wishing to become an entrepreneur. Just like Nike expanded its market by stating that anyone with a body can be an athlete, these businesses are demonstrating that any person with thinking capacity and access to bandwidth can be an entrepreneur.

From 2014 onwards, the focus of our fund was purposefully and gradually shifted towards the thriving winners of our digital age through the realization that tremendous value was to be found in the great software platforms. Personal friendships with some of the world’s most talented machine learning experts helped to open my eyes to what was happening at the frontier of science.

Our first move to get involved with a pure software business was when we bought a stake in Microsoft at a price of USD 19.60 per share, in November 2011. The valuation at that time was unbelievably cheap. It felt like picking up a bar of gold discarded on the street. Today, this share price stands at USD 218, and it is an important lesson that owning one of the most widely known companies in the world can produce a 10-fold return in less than a decade.

The transition to move from investing in the great consumer brands such as Coca-Cola to the great software platforms of our time has indeed not been easy yet provided a great learning process. I realized that the common assumption that Warren Buffett became a billionaire by owning boring businesses was mistaken; his track record was largely driven by a handful of concentrated investments in the growth companies of his time. At the same time much of his investment style was based on a bet against change and increasingly I felt that we had to be part of the businesses that create change.

Whereas before it felt enjoyable and safe to put a multiple on free cash flows and find comfort in low valuations, now actually a vision was needed regarding the future direction of a business for a few years head. The qualitative drivers of earnings growth such as the quality and entrepreneurial spirit of management became the most important factor to take into consideration. Our new investment focus required learning from software engineers and thinking about the possible trends of revenues and operating margins when the businesses reached scale in the future. There was much to be learned at developer conferences with valuable opportunities to meet IT teams of big companies and find out their rationale for using Mulesoft or Alteryx, for example.

What became clear during the past decade is that it is best not to spend any time on average companies or get involved with weaker firms no matter how cheap their price. The first step most ‘value’ investors make is to hunt where the prices are low. That is also the first mistake. Exceptional businesses are rare, and one has to be willing to pay a fair price for prime assets. That brings us to today, when we have the opportunity to participate in exponentially growing businesses: and the choice to either get comfortable with paying a fair price, or to watch from the sidelines.

Home run investments happen when one recognizes an exceptional business for which exponential growth is likely to continue for a much longer time than most people would be willing to make projections for in their excel sheets. As a result, a price that seems high is actually cheap. This is the value investing of the 2020’s.

Our strategy of fundamental investing in businesses with a strong position combined with a venture capital mindset, as well as my ongoing fascination with how advancements in artificial intelligence and computing infrastructure impact our lives, led to our first investments in businesses such as Trupanion, Shopify, and Sea in 2016 and 2017. Here, we had great respect for management, and it was absolutely clear that these businesses would increase in value by multiples as they were already the leaders in their fast-growing markets. One has to measure such businesses not by the percentage of the pie they own, but by how much bigger they could make the pie. As these businesses are solving some of the hardest problems, they have few competitors or peers to which to compare them to.

Since then, the share prices of Shopify, Sea, and Trupanion went up more than 10 times and our conviction is that the expected risk-adjusted return for each of these businesses for the next five years is just as good (if not better) as when we first bought the shares. Even more exciting is the fact that we think the next decade is going to offer even bigger opportunities and now we are well prepared to seize them aggressively.

As a result of our gradual shift in focus towards thriving businesses, we were already largely invested in the digital winners before the pandemic started. In March, the stock market tanked with an unrivaled swiftness and the entire world changed its behavior. For several weeks not much news was received from most businesses, and we could only guess what was happening. Subsequently, the first green flags started to come in – I will probably never forget the following Tweet in April 2020 by Jean-Michel Lemieux, CTO of Shopify saying: ‘As we help thousands of businesses to move online, our platform is now handling Black Friday level traffic every day! It won’t be long before traffic has doubled or more.’ It was the final hint we needed to sell every last ‘offline’ business and double down on the highest quality ‘online’ businesses such as Shopify, Sea, and Stone, that offer the essential tools to help the world to digitalize.

One does not have to invest in startups in order to achieve extraordinary returns. The American venture capital system will continue to produce wonderful businesses that at some point decide to let their shares trade in public markets. During the second half of 2020, a record number of software businesses came to the stock market. We had a serious look at several of them, for instance C3.ai and Snowflake, but decided to only invest in Palantir as its downside was limited and its upside significant.

The question remains: what do we consider to be an exceptional business? Of course, we have an extensive checklist that examines the quantitative financial metrics. For example, our businesses can finance high organic growth from operational cash flows and have the luxury to reinvest all cash generated back into the business at high expected returns.

More important, however, are the qualitative drivers of earnings growth. These ensure that we do not have to sell the business for a long time. We much prefer to not buy any business that we have to sell anytime soon. Instead of sharing an analysis of a particular investment and thereby pitching a business, let me, in the sections below, share several important qualities we look for.

The Thrivers have a Data Driven Mindset

Warren Buffett often said: “The chains of habit are too light to be felt until they are too heavy to be broken.” The secular digital trends were already in place for years, yet the pandemic has finally opened up the eyes of many and broke old habits that were being continued mostly out of complacency. Businesses are now forced to rethink their entire technology stack.

As technology becomes increasingly engrained in our lives one cannot easily define a ‘tech’ industry anymore as we did before – modern companies are software companies and the leader in every industry is going to be a business that is data driven. This requires having an excellent digital architecture. Even older established franchises such as Lindt & Sprüngli and Colgate Palmolive need to become data driven in order to stay relevant (both recently launched their stores on Shopify).

More important than using agile technology is that management has a data driven mindset. The ‘tech’ culture needs to be embedded in the DNA of management. The combination of having an entrepreneurial spirit together with a data driven approach ensures that a business can quickly adapt to changes in the world. This data driven approach to execution and vision is what we look for and find in great CEO’s such as Jeff Bezos, Daniel Ek, and Tobi Lütke.

A Culture of Entrepreneurship

We prefer investing in businesses with founders that are mission-driven and doing their life’s work. Having a company owner as team leader is essential because they will naturally be focused on creating value over the long-term as opposed to having a quarter-to-quarter mindset. As the world changes, an entrepreneurial spirit is likely to enable the team to innovate and adapt faster than most bureaucratic firms that are being managed by suits.

Employees, clients, and we should love a business chosen by us. Investing is not objective. It is important to love a business as this increases the commitment to not sell it as well as think like a co-owner. We believe that most standard talk about being objective and constantly tweaking a portfolio based on one’s latest opinion or stock price is nonsense. One should have the same feeling whether owning a stock or holding a piece of a wonderful private business.

We like to be part of teams that ‘smell’ like winners. It happens when all qualitative and quantitative aspects come together. When all the hard work of digging through accounting becomes intuition. It is what I deeply sensed when I met Stone management in Sao Paulo a little over a year ago. In the airplane to Brazil, I read many sell-side reports about Stone and was surprised how the bank analysts thought it was competing with bigger banks. Speaking to management I experienced their fantastic spirit of integrity, ambition, mission, and entrepreneurship. The trajectory of a business will eventually bend in the direction of its culture. Therefore, this is the most important thing.

Today, Shopify, Stone, and Stripe, amongst others, ‘smell’ like winners. It is probably a far better investment to buy these companies at any price than owning a mediocre company at a price that seems low. One needs to keep in mind that just as a great company can quickly grow into its valuation, a cheap company can suddenly shrink out of its valuation. For example, someone paying a single-digit earnings multiple for some average firm might in fact be paying 80 times its earnings.

Scalable Cloud-Native Architectures

We like to see an architecture that is cloud-native, meaning operations can scale up almost infinitely without incremental expenses or complexity. In addition, software engineers are all working at constantly improving the core product.

What is likely to be the most valuable enterprise of 2050?

Most likely it will be a network of self-learning software with access to almost infinite computing power, optimizing all operations every nanosecond, and monitored by software that in turn is being governed by humans. (My guess is that this particular business will start to play an important role in our health and longevity).

How would a business that is on a trajectory towards that state look like in 2040? And in 2030?

Today, at the very beginning of 2021, several companies seem to be heading in that direction. They have a cloud-native architecture and are applying machine learning to improve outcomes. For instance, Google, Tencent, and Amazon are on track. Such businesses on this path should deserve a significant share of the investor’s attention as they will produce long exponential growth and produce enormous fortunes.

In 2030, we will be surrounded by businesses worth hundreds of billions or even trillions, some of which will be founded in the next few years. And some we probably own today.

Our ultimate mission is to participate in several of the most scalable thriving businesses of our digital age.

A long runway of growth ahead

All our businesses have a long runway of growth ahead. Their market values are a small fraction of the opportunity that they are addressing. Two examples are Spotify and Palantir.

At the current share price, Spotify basically only represents a fraction of the value they will be able to unlock in the growing market of audio entertainment. The key for Spotify is to change a variable cost base into a fixed cost base just like Netflix has. As the market share of the big labels, measured by the daily hours of engagement of the big labels, is declining, Spotify will be able to adjust its business model and create enormous operational leverage meaning that profitability will grow faster than expenses.

The music catalogue is not the business model. The value lies in the machine learning that drives discovery and engagement, the original content from people like Michelle Obama, Kim Kardashian, and Joe Rogan, the data analytics and distribution for artists, the direct and social relations artists can have with fans through music and videos. We believe that Spotify will be worth at least five times more in 2030.

In October, we bought a stake in Palantir. Earlier, in June, our concentrated Tech Fund, which has a mandate to also buy shares in the secondary market, bought shares of Palantir from insiders, before the direct listing. At the price we bought, the equity had much more upside than downside.

Palantir is operating a software platform that functions as the digital infrastructure for data-driven operations and decision making. The software helps to structure and capture context in data of large corporations. Governments are increasingly realizing that they have to deal with serious data challenges and cyber risk. As most governments cannot attract the most talented software engineers, they need private enterprises such as Palantir to help them build solid infrastructure. Foundry, Palantir’s software for enterprises, is used by companies to make safer cars and airplanes or to accelerate cancer research. The speed to bring new clients on board is improving and revenues will grow faster than expenses.

Both Spotify and Palantir have a long runway of growth ahead. It is our task to figure out how sustainable the exponential growth is and whether a business can sustain high and profitable growth for much longer than consensus thinks is possible. We all assume that there will be a reverse to the mean at some point. Yet, companies such as Google, Amazon, and Microsoft, have surprised the world by continuing to grow faster than most small companies despite their USD 1 trillion + market capitalization.

Often, discussions about companies tend to drift into some version of “what’s the valuation now, and what will happen over the course of the next twelve months?”. However, the qualitative drivers of success are far more important than the valuation today. If we find the right business, then it is just as important how we approach the investment; from the perspective of an owner.

Participate with an Owner Mindset

In the Sharing Thoughts newsletter of March 4, 2020, I wrote ‘Would you sell your successful family business because a virus is spreading? We do not trade partial ownership (shares) based on macro-economic events. We grow our wealth because we co-own companies that prosper.’ That mindset of ownership is an edge we have over most market participants.

March 2020 again showed that the idea that anyone can time the market, is an illusion. The moment one goes cash one creates a huge risk and problem should one wish to buy back the shares at some point. During the last week of February 2020, I did feel some inclination to reduce our investments and to build some cash as it was clear that the situation was out of control.

We decided not to do this as 1) this is against our principles as long-term co-owners of a business, and 2) we mainly own thriving software companies. I am certain that we would not have been able to be fully invested again on March 23rd when, without any bells going off, the stock market came back like a rocket driven by the digital winners of our time. Interrupting a favorable law of power (compounding) is the worst mistake you can make as an investor.

Many people are able to point their fingers at good companies. However, more important is in the first place to own such a wonderful business and secondly to not sell it. The latter is the big mistake almost everyone is making all the time. It’s the reason why so few people became billionaires in the slipstream of Bill Gates, Jeff Bezos, and Pony Ma. The fact that Naspers never sold its Tencent stake even after it kept doubling is one of the more remarkable investment successes that I am aware of.

The dumbest reason to sell a great business is based on the argument that the valuation is high. As mentioned before, exceptional businesses are rare. Moreover, one often doesn’t really know the valuation of an exceptional business because their leaders continuously find new ways to create value and seize opportunities. Who would have thought that Amazon, the Everything Store, would create the Amazon Web Services, the world’s greatest cloud business?

Not selling is difficult. When people speak about volatility, they often mean a downward move. For us, upward volatility is more difficult to deal with. It happens when the stock of a great business seems to go up faster than the underlying developments seem to justify. Even we then become inclined to sell part of the gain. When dealing with businesses that one thinks should be worth multiples in 2025, selling even part of the short-term gain is a silly thing to do.

It is seldom easy to own the clear thrivers. Every single moment since inception of our fund in 2010, Amazon presented itself like a winner. Jeff’s focus, ambition, and long-term mission were obvious. Yet, every day over the past decade consensus was that Amazon was too expensive. People could read articles like this one “Amazon is one of the most overvalued stocks” all the time. Did you own Amazon for most of the past ten or twenty years? Well, we did not. Even worse, in 2010, I did not even study every of Amazon’s quarterly earnings reports. As an investor, this is the equivalent of being a swimmer going to the Olympics without having a clue about how fast the competition is doing its legs. Because in fact, Amazon’s rising market value was the competition for any active investor that did not own the stock. Today, it is essential to understand that the five biggest constituents of the S&P 500 index by weight are Apple, Microsoft, Amazon, Facebook, and Tesla. The bigger tech firms account for two-thirds of the total returns from holding the S&P 500 index. There may be more sense to recent market movements than most would think.

Software Gaining Market Share in New Fields

Over the past decade, software overpowered much of the physical assets and labor in some industries. During the next decade, software will also transform banking, education, healthcare, amongst others. For example, Teladoc Health, the company that acquired our Livongo shares, is transforming healthcare experiences by empowering virtual and personalized care. Many factors are coming together these days that will create tailwinds for certain businesses (while sinking others). Let me just share a few examples.

Firstly, as applications, devices, and employees have left physical buildings, businesses need modern cloud-native software. Enterprise is no longer a location and as a result entirely new cloud-based architecture is required. As serverless platforms are running at the edge, the network is becoming the computer and computations need to be distributed and pushed as close as possible to the data sources. Companies such as Fastly, Cloudflare and Crowdstrike have tremendous growth ahead as companies are shifting budgets towards achieving low latency, compliance, and security. Joshua Bixby, CEO of Fastly, wrote in his 2020 Q3 shareholder letter that: “As enterprises complete the shift to the cost-saving measures provided by the central cloud, their next frontier is to move logic, compute power, and security to the edge in order to more effectively meet their customers in the digital-first way that consumers have come to expect and rely on.” Autonomous vehicles, drones, robots, games, virtual reality devices, and smart cities will have a certain amount of computing power, yet they need to constantly rely on real-time intelligence from edge networks.

Secondly, 2020 was the year in which the promise of artificial intelligence became more tangible. We are probably entering the phase in which the early majority is starting to adopt a machine learning infrastructure. Breakthroughs such as GPT-3 and DALL·E (an autoregressive language model that uses deep learning to produce human-like text and generates images from text descriptions) and AlphaFold 2 (code that predicts the 3D structure of a protein based on its genetic sequence) are hints of what lays ahead the coming decades. Tim Davidson, founder and CEO of Aiconic and one of our advisors in the field of artificial intelligence, concluded his year-end note by saying “In the unique world of machine learning, it was a year of meaningful breakthroughs. While uncertainty looms over 2021, we see enough evidence to support a bullish view on everything that is cloud + machine learning (ML). The expanding ML-as-a-Service industry and ever declining costs of research are likely to empower a new generation of ML products and companies. Lower failure costs combined with increased competition will accelerate the startup iteration cycle, providing investors with faster outcomes. Finally, corporations and governments will drastically increase their venture investment targets in an attempt to stay relevant in a rapidly digitalizing and automating economic environment.” We are excited about emerging machine learning infrastructure companies that are able to deliver the end solutions that the market is now ready for to start implementing.

Thirdly, the year 2020 opened our eyes to the incredible power of “software meets genetics”. On January 11 the Chinese put the genetic sequence of the SARS-CoV-2 virus online. The team at Moderna used the sequence to design a vaccine and 48 hours later the vaccine was completely designed. This is in the first place fascinating because a digital copy arrived before the biological version and secondly because a vaccine was designed completely based on the digital copy. The vaccine the FDA reviewed on December 17 was exactly the same vaccine that was designed in January. Not a single atom was changed. With the new mRNA approach to basically print vaccines, the body receives an instruction to make neutralizing anti bodies against a protein of the virus. This prevents the virus from multiplying. The mRNA method perfectly mimics in a human cell the biology of an infection. It opens a future in which vaccines can be printed instead of grown. And this is only just one example of the future wealth and health that will be unlocked with machine learning.

Fourthly, companies such as Starlink are offering fast connectivity to any sensor, machine, or mobile computer thereby removing networking bottlenecks which further enables computing closer to the data and dramatically better latency.

Fifthly, the market value of Bitcoin has surpassed the one of Berkshire Hathaway. This hints to the immense power of technology to be able to redesign the ways we interact as well as the definition of money. For people living in emerging markets, the age when birth is generally destiny is closing as technology is hugely inclusive for millions of people who now, by using cryptocurrencies, Stripe or Shopify for instance, can control their financial future without being at the mercy of some self-enriching dictator.

The selection of breakthroughs mentioned above just show that while the virus dominated all news in 2020, much innovation is happening that will create new opportunities for talented people to thrive and solve problems both in the academic and the entrepreneurial field.

Miscellaneous

Over the next decade, stunning businesses will emerge, and huge fortunes will be made by the digitalization of our personal and professional lives.

We shall be pleased if in 2030 our current investment has grown by 5 times. We trust this is a reasonable target with our current portfolio of great businesses and focus on the podium where music will play for decades to come.

As a result, our fund should have more than EUR 1 billion assets under management in 2030. In 2020, in order to prepare, we invested in the structure of our company as well as in our team. We like to thank Kaya Fund Services for the good partnership over the past decade and are excited to work with Privium Fund Management and Circle Partners, the new fund administrator.

In 2020, I started writing the periodic Sharing Thoughts and received considerable positive feedback. Therefore, I will continue writing the newsletter and from now onwards it will be accessible to any person who enjoys reading about topics that are directly or indirectly relevant to our investments or business in general. If you are not a member yet, you are welcome to subscribe to the Sharing Thoughts.

Thank you for your referrals; we are happy to welcome your children and friends as partners. Please feel free to forward this letter to them.

Again, I would like to thank Martin, Felicia, and Seth for their contributions to the investing work. An impression of our team’s work can be seen here.

In closing this letter, I wish you and your family a happy and healthy 2021. As always, feel free to contact us with any questions.

I have never been more bullish.

Also on behalf of Martin, Felicia, and Seth,

Sincere regards,

Georg

The post Guardian Fund 2020 Year End Commentary: Investing in Thriving Businesses appeared first on ValueWalk.

Sign up for ValueWalk’s free newsletter here.

{kind=link}