{kind=link}

We (might) Work

Courtesy of Scott Galloway, No Mercy/No Malice, @profgalloway

Real estate is an awesome gig.

Real estate is an awesome gig.

For starters, the supply of fertile land (urban centers) is finite, but the source of demand keeps growing (more people/capital moving to cities). On top of that, we’ve granted real estate development such favorable tax treatment that it is nearly immune from taxation. Even Donald Trump, arguably the worst business person in U.S. history, made money in real estate development, despite the serial failure of the underlying business. As one tax law expert put it, the real estate industry “thinks of the tax code as a basket of goodies to feast on rather than a financial obligation of doing business.” Imagine buying stock and being able to depreciate it as it increased in value.

Thanks to ever-growing demand and favorable tax treatment, real estate once minted more billionaires than tech. In 2019, 223 people on the Forbes billionaire list owed their wealth to real estate, compared to 214 from tech.

Then … Covid.

The third great conveyance of the modern economy (the first two being globalization and digitization) is in full swing: Dispersion, the process of value leapfrogging traditional points of distribution. Three sectors stand to register the greatest reallocation of stakeholder value (i.e., shit-kicking): healthcare, commercial real estate, and education as consumers leapfrog hospitals, HQ, and campuses.

Dispersion is enabled by both globalization and digitization. High-bandwidth communications link billions of people, and robust mobile devices render that network continuous. Now, blockchain technology is enabling the network to store value (bitcoin) and act on it (ethereum). This will bring further disruption to industries low on IQ and heavy on EQ, such as insurance/asset management/central banking (wrapping my head around this is my biggest challenge for 2021).

The point is, the pandemic has accelerated all of these trends. A year-plus of forced acceptance of remote services in every sector has carved permanent change into our behavior. And, few sectors have seen a more radical transformation than office work.

Valuation

Any discussion of valuation must be set against the backdrop of a firm’s valuation. Gannett Co., Inc. faces structural challenges, but at a $2.5 billion enterprise value (0.7x revenue), Gannett is undervalued. Tesla is a great product and company, but at $637 billion (20x revenue), it is overvalued (send in the clowns/trolls). Disclosure: I am a shareholder in Gannett and consistently wrong re Tesla.

Anyway, the office real estate in the U.S. alone is a $2.5 trillion asset class, and it is going to leak the GDP of Switzerland to residential over the next decade. However, it’s not as easy as going short all office firms and long all residential. The fire that will rage within the office sector will raise seeds of dormancy — and create unexpected winners. One pyrophile plant that emerges from the fire may be WeWork. I’m especially proud of that last sentence.

Why We (might) Work

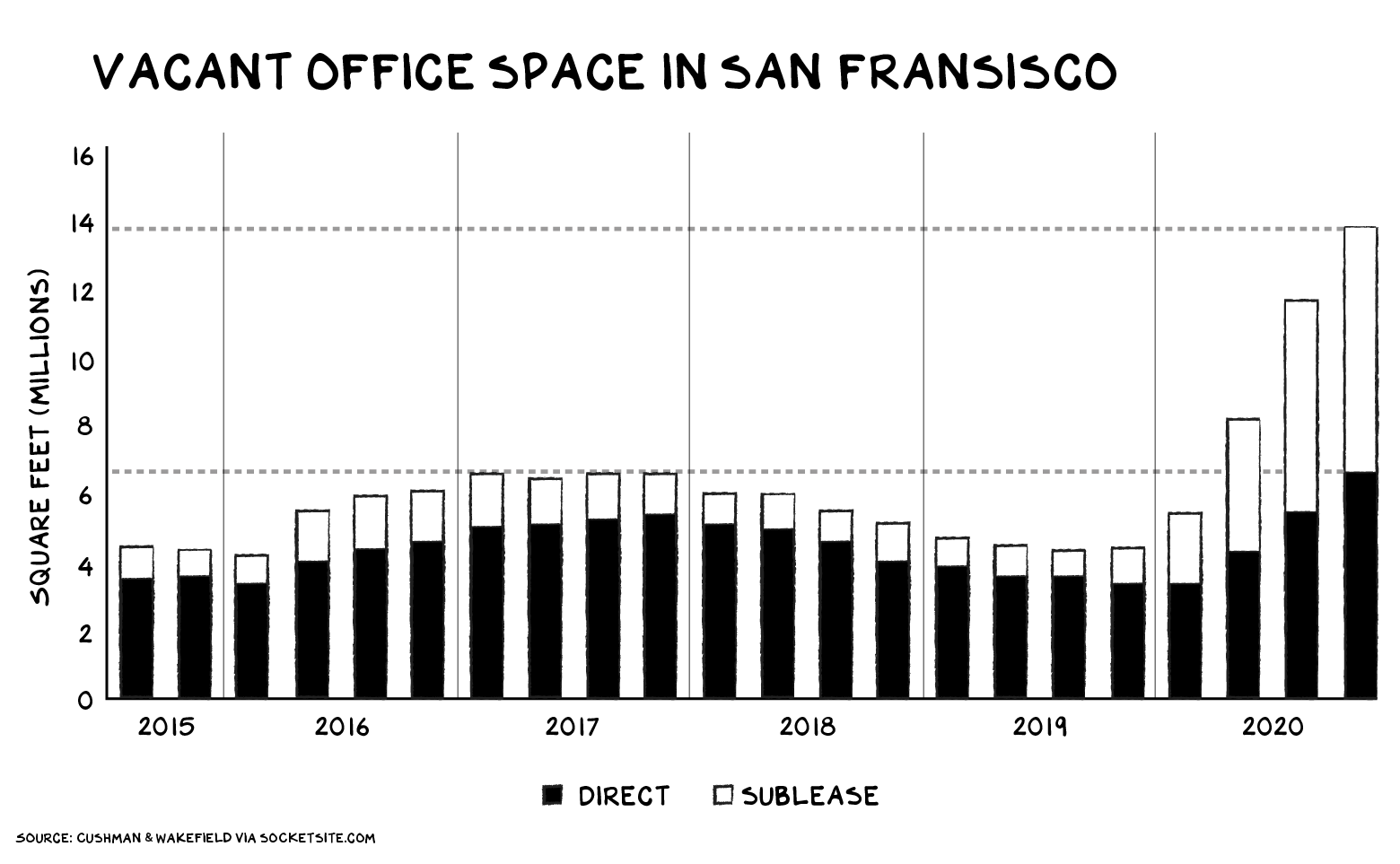

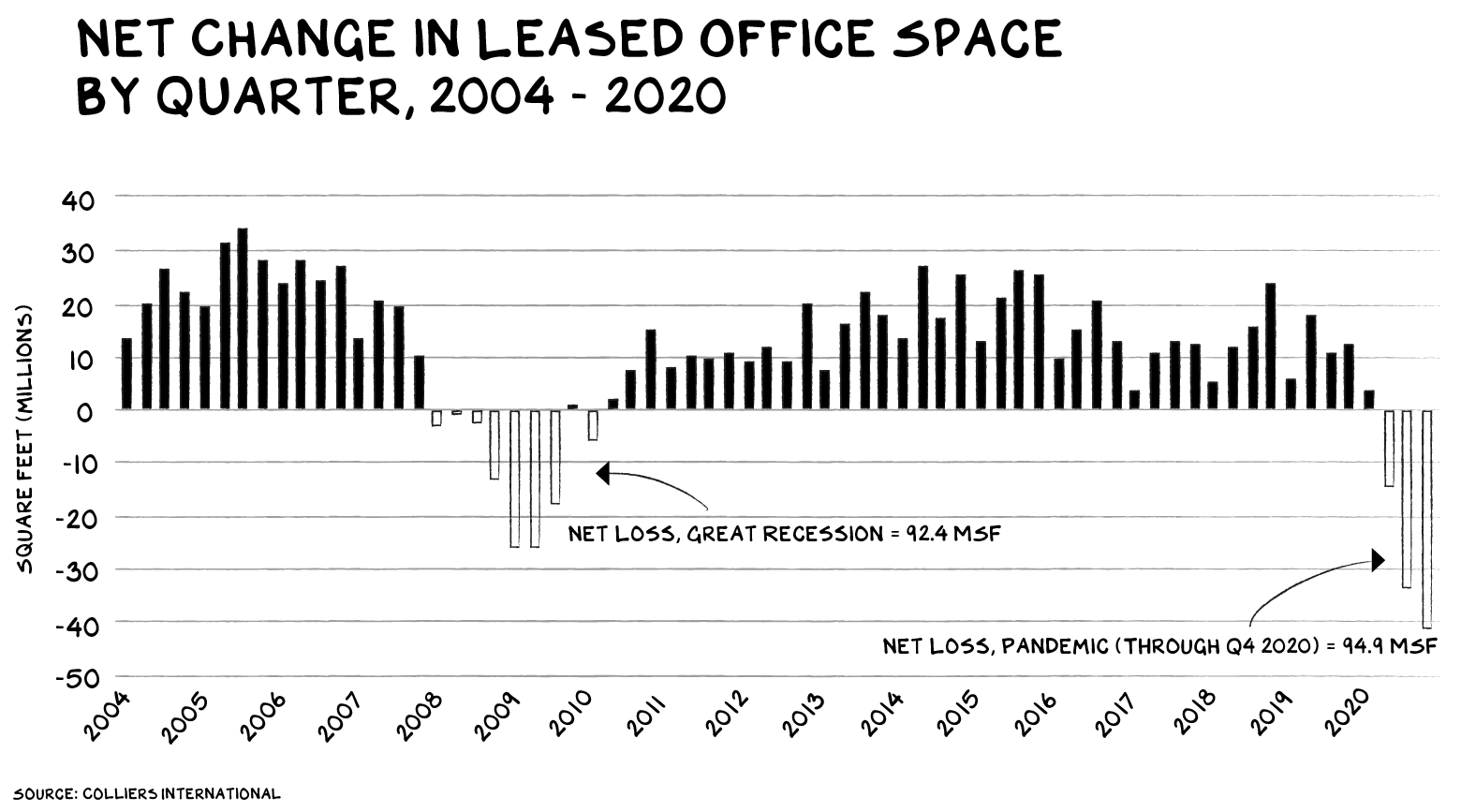

The wholesale abandonment of office space has been among the most striking fallouts of the pandemic, and it will have profound effects on the way we live and work, long after the virus has been tamed. In New York, new office space is coming on the market 59 percent leased, down from 74 percent pre-Covid. San Francisco went from its lowest-ever office vacancy rate to its highest in the same year, and office rents are set to decline by 15 percent. The worst may be yet to come. Analysts predict that commercial vacancy rates will rise from 17.1 percent in 2020 to 19.4 percent in 2021, besting the previous high of 17.6 percent in 2010. And, as $430 billion in commercial and multifamily real estate debt matures in 2021, lenders will be forced to reconcile the effect of the pandemic on their investments.

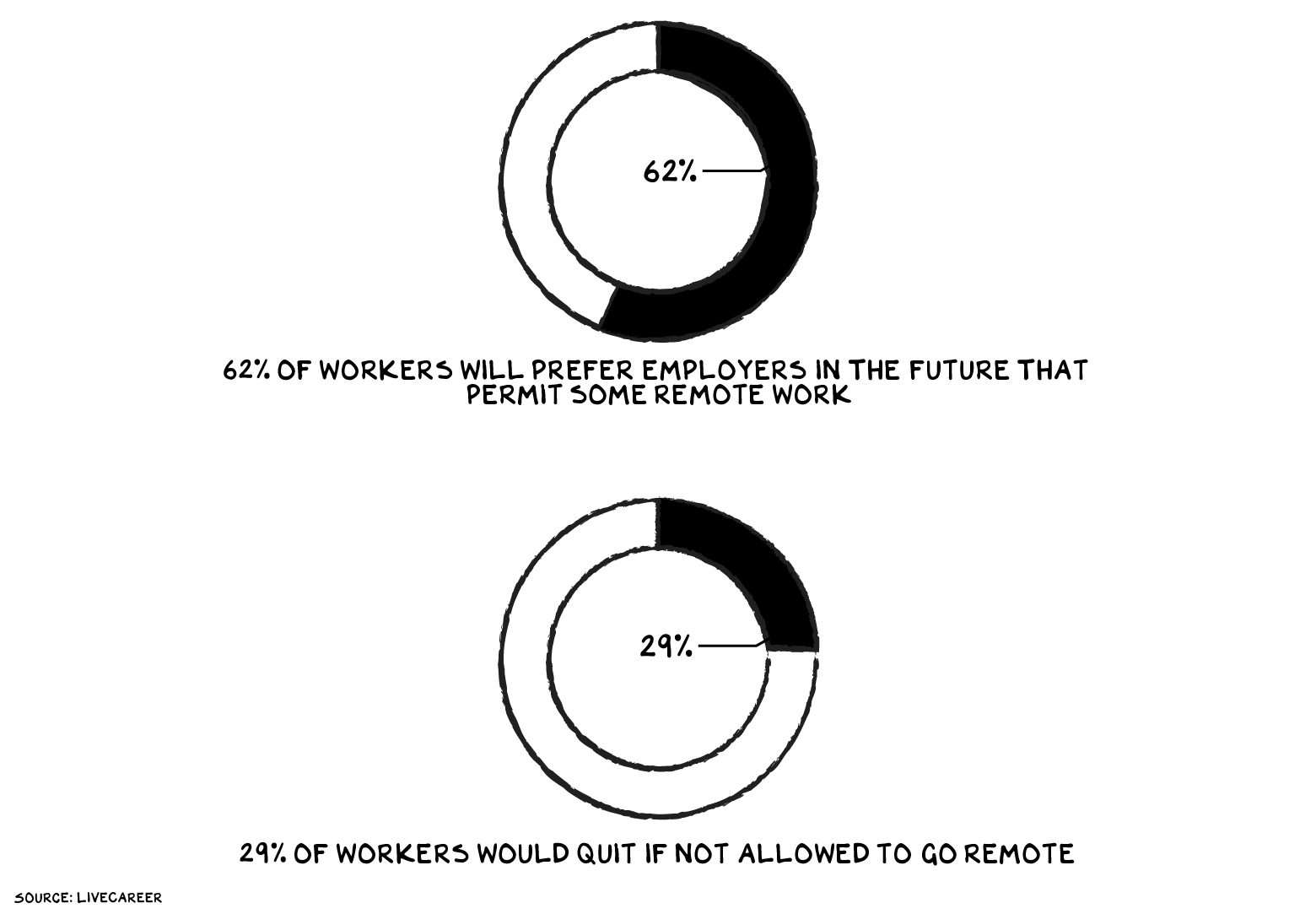

These changes will endure. Twitter, Facebook, and Slack have all announced the move to a predominantly remote workforce. Pinterest recently paid $90 million to terminate its HQ lease in San Francisco. REI sold its new headquarters before even moving in, and CVS plans to cut 30 percent of its office space. At my New York-based education startup, Section4, we asked employees if they wanted to come back to work after the pandemic; overwhelmingly, they wanted to stay home. We paid $1 million to terminate our SoHo office lease. After decades of promise, the telecommuting revolution is here.

Back in 2017, I predicted WeWork, then worth $16 billion, would lose 75 percent of its value and become the “poster child of unicorn mania.” Two and a half years later, that prediction was wrong, very wrong — WeWork was preparing to go public on the heels of a $1 billion investment from Softbank that valued the company at $47 billion.

But it just didn’t pencil out. After deploying my unique domain expertise (math) I concluded: “Any equity analyst who endorses this stock above a $10 billion valuation is lying, stupid, or both.”

The ensuing meltdown was cinematic — literally. Tonight, WeWork gets its closeup, in a documentary on Hulu, The Making and Breaking of a $47 Billion Unicorn. I’m in it. I have not seen it, but it is a w e s o m e.

(BTW, the production company wanted me to come to a studio in New Jersey for filming. I told them I had a two hour window and that they needed to come to my place in SoHo or find another angry professor to make terse comments. They shuttled a dozen people to my place and set up a studio in my kids room, next to the climbing wall. At that moment, I realized that people tolerating you being an asshole doesn’t make you … any less of an asshole.)

Anyway, that wasn’t the end of the story of We. Despite losing $60 million per week of Softbank’s money in 2020, WeWork didn’t go out of business. Instead, to the board’s credit, the company fired the Jesus of reclaimed wood and smoked glass, Adam Neumann, and brought in an experienced manager. Sandeep Mathrani shed 100 of the company’s worst performing properties along with the self-dealing arrangements foisted on the company by Neumann, and laid off 8,000 employees. A crisis is a terrible thing to waste, and if WeWork turns the corner to profitability in Q4 of this year, as it has promised investors, it will be the case study in fire intensity and germination.

The new WeWork is a stronger company than the 2017 model. It’s still not worth $50 billion, but it might be worth $9B (or more). The new WeWork will benefit from the massive investments in space and brand equity (i.e., global awareness); additionally, people underestimate the difficulty of scaling “vibe,” where WeWork has a proven talent.

Most companies aren’t going 100 percent remote. But when we return to the office, we will want less space that is more flexible, and more appealing to the premier asset of any firm: its ability to attract skilled, young human capital. Pre-corona, Section4 had a long term lease on 8,000 feet at $70 per square foot. Post-corona, it will probably be closer to 2,000 at $100, and on a year-to-year lease. Further out, I could see us opening offices in Miami or Austin, where great talent is migrating.

Imagine: a commercial real estate play, with properties around the world, configured as flexible office space, rentable by the hour, the day, or the month, with great community spaces, aspirational design, and strong tech. In sum, We might Work.

Pass the Pipe (Here We Go … Again)

However, Softbank has not run out of real estate opium quite yet. Now it is trying to pass the pipe to Compass investors, hoping the markets enter into consensual hallucination that a rollup of residential real estate brokerages is (wait for it) a tech company. Yesterday, Compass went public at a valuation of approximately 3x revenue. Realogy, the closest competitor, trades at 0.29x revenue. From the Compass site:

Compass is building the first modern real estate platform, pairing the industry’s top talent with technology to make the search and sell experience intelligent and seamless.

The firm even describes itself as “a tech company reinventing the space,” despite the fact that itspent 78 percent of expenses on commissions to brokers, instead of technology or algorithms. This makes sense as Compass is … a real estate brokerage.

Just before the IPO, the underwriters cut the pricing range and halved the number of shares offered. Despite a massive haircut in supply, the first day pop was an anemic 12 percent. I’ve worked at an investment bank taking companies public, founded companies that have gone public, and been on boards of companies going public. Dramatically reduced supply (shares) at a lower price, coupled with Goldman’s unparalleled institutional base of buyers, and Compass barely got out. In sum, the corners of this trade are beginning to collapse and could lead to a broken IPO within days. WeWork may be rising from the ashes as Compass begins to smolder.

Life is so rich,

P.S. The Section4 Sprinter community is growing. These sprinters are professionals from a variety of companies (think: top tech, consulting, mid-size firms, etc.), roles (entrepreneurs getting their hustle of the group to seasoned managers looking to level up), and countries (50+ represented). They are getting access to top business school professors, actionable frameworks, and a community of learners they can discuss topics with. The next sprint, Product Strategy, is taught by my esteemed colleague Adam Alter — learn more here.

P.P.S. On this week’s Prof G Pod, Marty Chavez, a senior advisor to Sixth Street Partners and the former CIO and CFO of Goldman Sachs, shares his ideas around regulating big tech like big banks and discusses the trends playing out in the digital ecosystem — including the digital asset space and fintech. You can find this episode on Apple Podcasts, Spotify, or wherever you listen.