{kind=link}

By Jacob Wolinsky. Originally published at ValueWalk.

Crescat Capital commentary for the month of February 2022, titled, “A Trifecta Of Macro Imbalances.”

Q4 2021 hedge fund letters, conferences and more

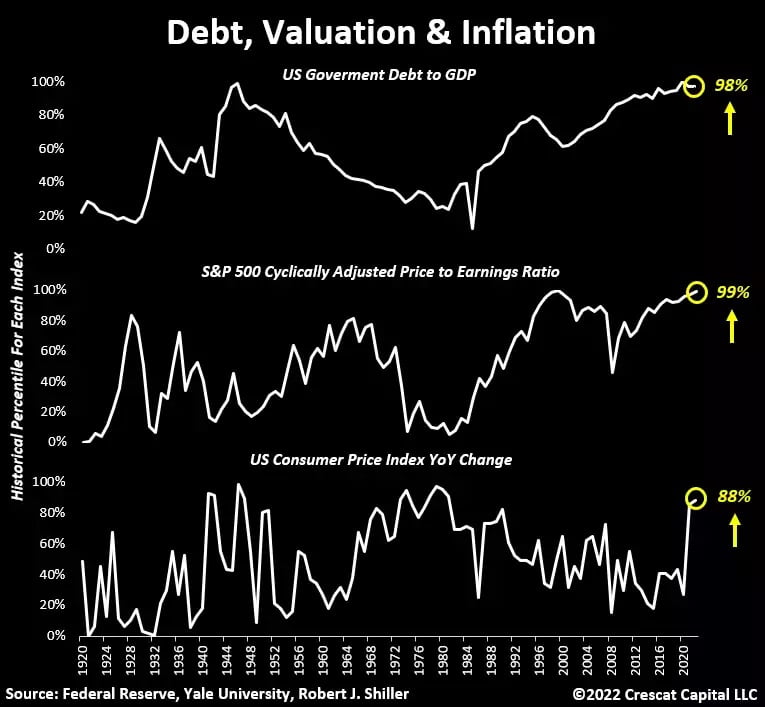

For the first time in history, the US is experiencing a confluence of three macro extremes all at once:

- High government debt to GDP like the post-war 1940s

- Excessive stock market valuation on par with 1929 & 2000 bubbles

- A resource-driven inflationary crisis environment comparable to the 1970s

Any one of these three economic states endangers the health of markets and the economy. Together they are a highly explosive mix. The disparities have evolved from an era of misguided monetary and fiscal policies. The unwritten plan may have always been to devalue debt by growing nominal GDP through surreptitious inflation. But the ongoing debt expansion, money printing, suppression of interest rates, and deception about the true rate of inflation has only created one of the largest speculative manias ever for financial vs. real assets. At this juncture, policy makers have become their own prisoners. Neither can they halt the rising cost of capital needed to stabilize financial markets nor can they put a lid on inflation.

Whether the Fed tightens or loosens financial conditions, it could only help further catalyze problems for financial markets and the economy. One would accelerate the bursting of historic bubbles in broad equities and credit, and the other would only fuel more inflation, a horse that is already out of the barn.

Chronic Underinvestment in Natural Resources

The fundamental problem that ensures an inflationary crisis either way, as Crescat’s macro research has uncovered, is the historic underinvestment in critical natural resource industries throughout the energy, materials, and agricultural sectors of the economy. We are convinced that both the investing public and policy making communities underestimate the significance of this capital investment shortfall and its implications.

This historic downtrend has not only constrained the current supply but is preventing future supply from being ramped up quickly. These are the commodities at the core of the supply chain for all goods and services. They represent necessities, including shelter, food, transportation, electricity, heating, and cooling. Demand for these basic needs is inelastic, i.e., not addressed by the Fed’s traditional inflation-fighting toolkit.

A major reason for the underinvestment in these industries has been a well-intentioned but uncoordinated environmental agenda that has obstructed the permitting process and thwarted the attraction of capital to finance new resource projects. The political and social pressure to go green has been massive, but the transitional planning on how to get there from an engineering and economic standpoint has been abysmal. As a result, an economic crisis driven by commodity price shocks is the tradeoff that we will almost certainly face. It will indeed take an inflationary crisis before there is the necessary political will to seriously reconcile these issues.

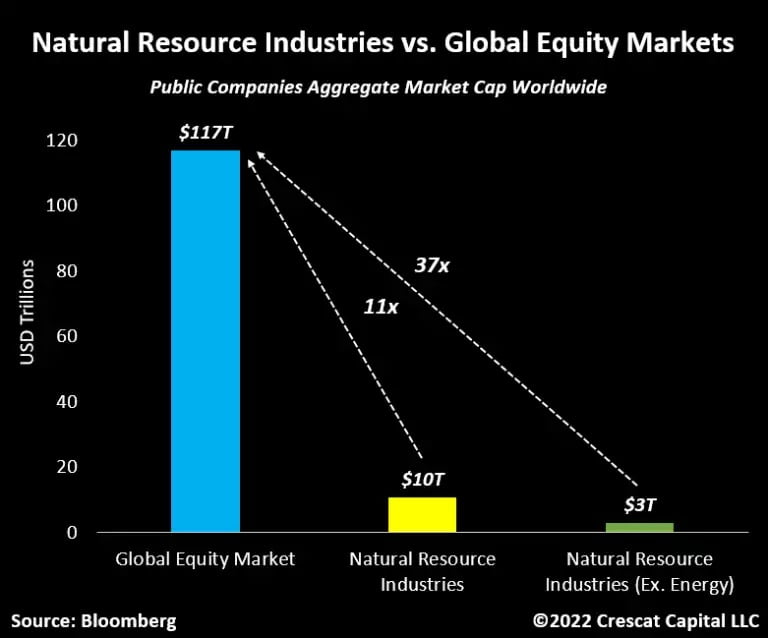

Driven mostly by technology related companies, global equity markets have grown to an aggregate amount of almost $120 trillion. That is 11 times the size of the overall natural resource industries worldwide. If we exclude the energy sector from this calculation, these industries represent a tiny amount of the global stock market, only 2.5% or $3 trillion of aggregate market cap.

We are finally beginning to see a rush of institutional capital into the resource markets as more investors are looking for ways to hedge inflation, but these industries suffer from a shortage of skilled management and labor to effectively deploy the capital. For example, there has been a decade long decline in college enrollment in geosciences. How can we possibly create a greener planet, including the raw materials necessary for clean energy, let alone our basic needs, when we have been minting less and less earth scientists every year? These imbalances simply cannot be resolved in the short term.

Fundamental Disparity

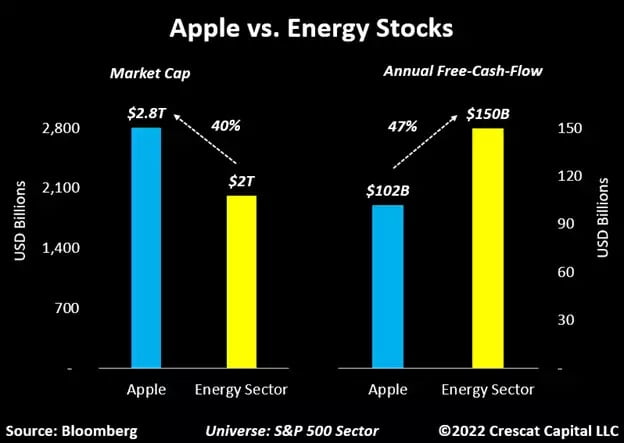

Too many years of inexpensive cost of capital and a financially repressive environment have lured investors into going out on the risk curve, drastically increasing their portfolio duration. These shifts in capital allocation have created enormous market inconsistencies. Today, for instance, Apple’s market cap is 40% larger than the entire energy sector. While most people justify this disparity due to fundamental differences, it is important to note that energy stocks generate almost 50% more in annual free-cash-flow than Apple. Will investors still prefer Apple when oil prices break out above $100/bbl?

As Good As It Gets

After the Covid handout of money to consumers, the government financed a once-in-a-lifetime boost to corporate fundamentals. Sales, profit margins, earnings, and free-cash-flow have all surged recently. But US households also drew their personal savings from record levels to historical lows in the last 18 months, a spending spree that totaled almost $5 trillion. To put this into perspective, that was close to 25% of the nominal GDP pre-pandemic. With absence of organic growth in the economy and fiscal stimulus waning, we believe this fundamental improvement is at peak levels and most of the positive news is behind us.

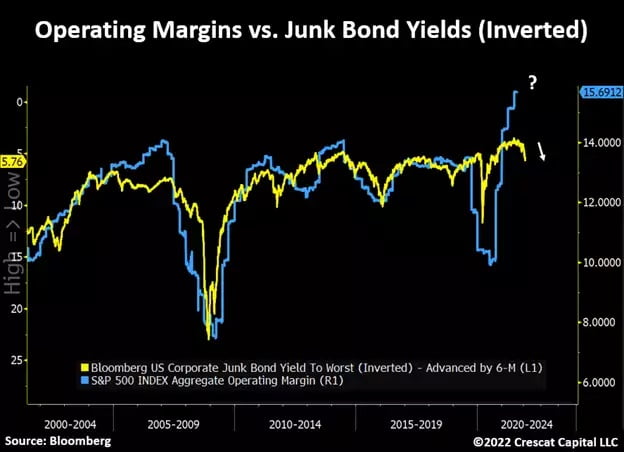

On top of that, the Fed is being forced to tighten monetary conditions late in the business cycle due the worst inflationary problem in over 40 years. See below a chart of junk bond yields versus profit margins for the S&P 500. Historically, tightening financial conditions lead to profit margin contractions. Another reason for us to believe US companies are currently at peak earnings.

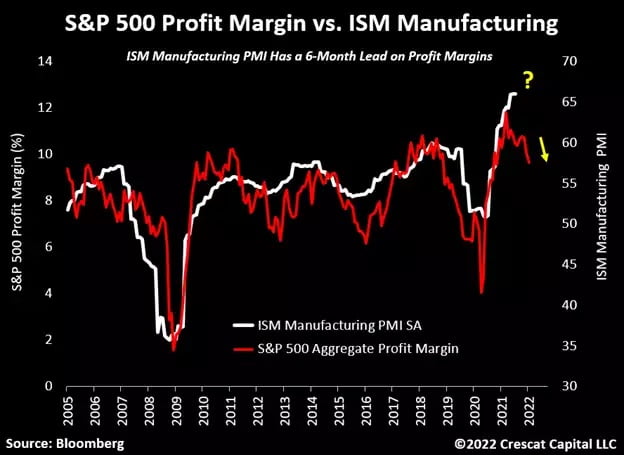

The ISM manufacturing PMI is an economic activity index based on a survey of purchasing managers at more than 300 manufacturing firms. This measurement also tends to lead profit margins for S&P 500 companies by 6 months and is in a bearish divergence.

Unrealistic Expectations

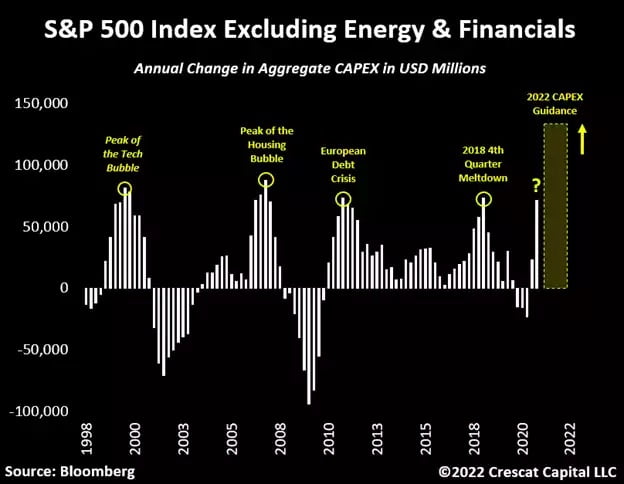

This notion that equity markets benefit from inflationary environments is a total fallacy. If a business today is incapable of growing at double digits, it is simply not keeping up with true inflation. If we exclude the energy and financial sectors, the median free-cash-flow growth for the S&P 500 is now contracting by -1.61%. Note that these numbers are in nominal terms. With headline CPI running at 7.5% YoY, their bottom-line fundamentals are down almost double digits in real terms. More importantly, Wall Street analysts now expect the largest annual increase in CAPEX of the last 30 years, a sign of the peak of the cycle for all sectors outside of energy and materials.

As shown in the chart below, this happened many other times when economic growth was at its apex. Outside of the tech and housing bubble, or even the meltdown of late-2018, the European Crisis was the only period that did not necessarily coincide with a significant downturn in overall stocks. Instead, the 2011 period was a mid-cycle deceleration.

Macro Model Flashing Warning Signal

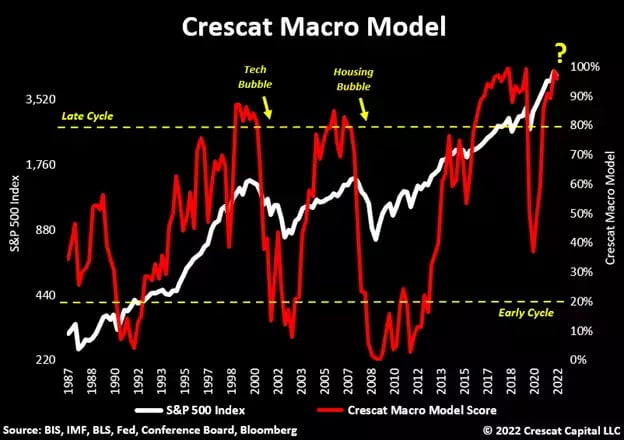

Crescat’s 16-factor macro model helps us identify what stage of the business cycle we are in as it naturally swings between expansion and contraction tied to changes in asset valuations and credit availability. This model encompasses macro, fundamental and technical factors, including some proprietary measurements. Our near-record macro model score is signaling an important bearish signal with current stock prices.

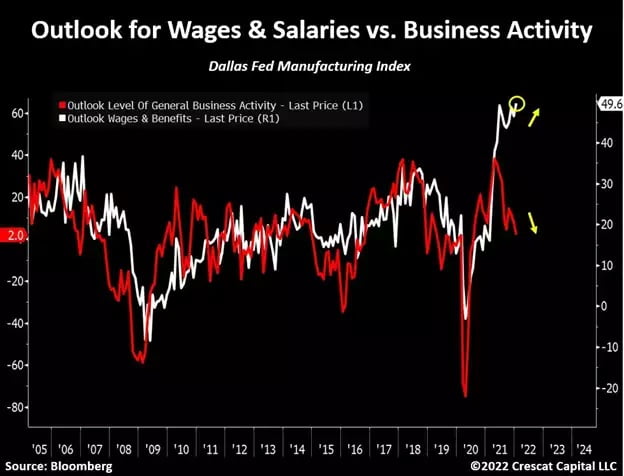

Rising Wages and Softening Business Outlook to Pressure Profit Margins

After more than 30 years of declining wage and salary growth, labor cost has finally begun to trend upward. Similar to the late 1960s, we think this is marking the onset of secular growth in labor remuneration. The outlook for wages and salaries just reached new highs while business activity continues to weaken. This is another important development that points to a coming squeeze in corporate profit margins from peak levels.

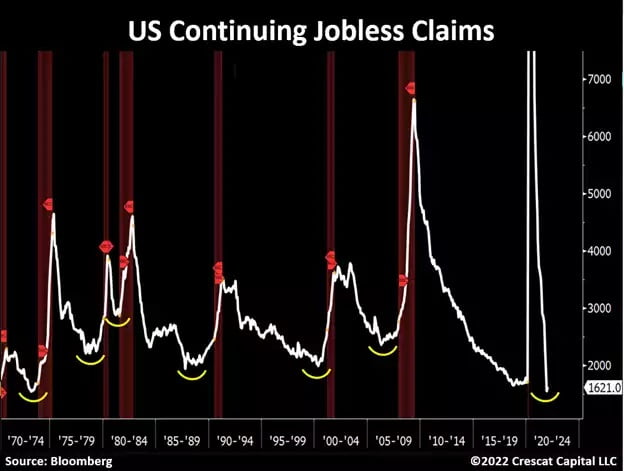

A Tight Labor Market Often Precedes Recessions

The unemployment rate, one of the best contrarian indicators in history, is now near all-time lows. As shown below, continuing jobless claims are also flashing the same signal.

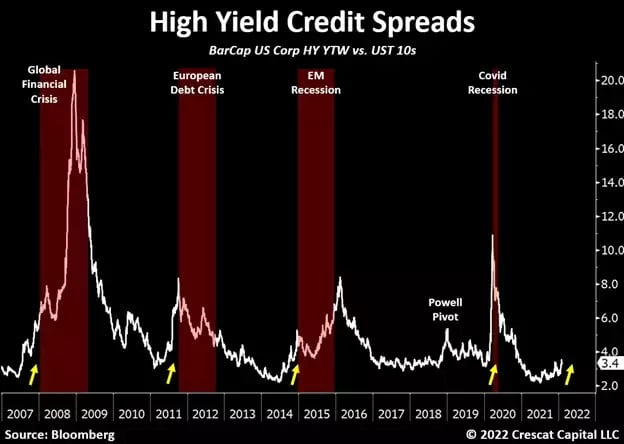

Tightening Financial Conditions

After reaching historic lows, credit spreads are starting to widen again, a foreboding recessionary sign if it continues.

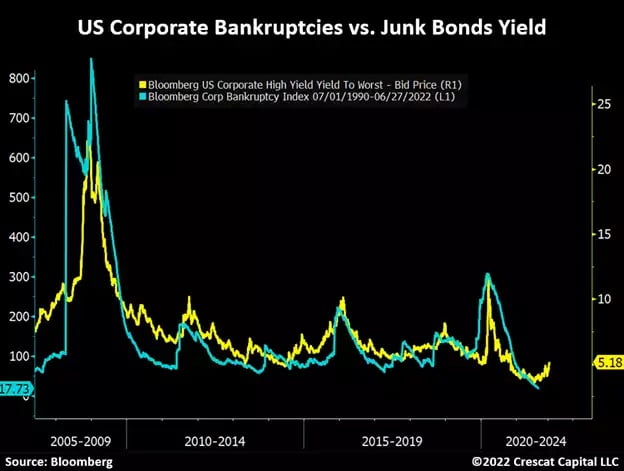

Note that junk bond yields tend to lead bankruptcies with a 6-month lag.

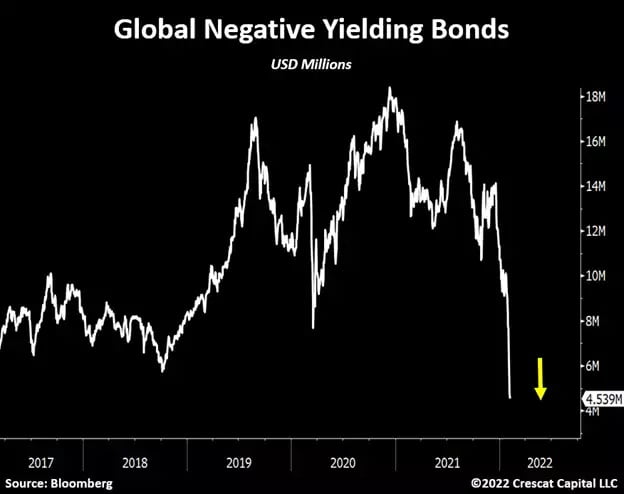

From $18 to 4 Trillion

Global long-term rates, particularly among developed economies, are starting to rise and marking a critical increase in the cost of capital. See below the outstanding value of negative yielding bonds worldwide has been shrinking massively. From over $18 trillion at its peak to $4 trillion today. We think these instruments will become obsolete soon.

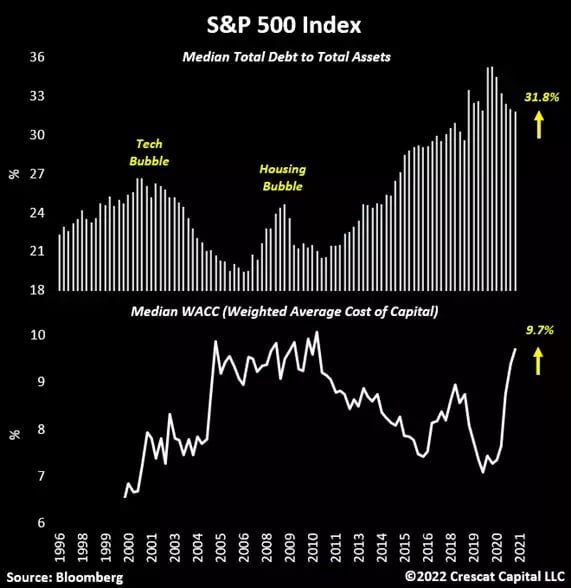

Cost of Capital Mispriced

In a rising cost of capital environment, the size of balance sheets matter. The median weighted average cost of capital for S&P 500 companies is now at its highest levels since 2008. The issue is that, as shown in the chart below, corporations are significantly more indebted than they were back at the peak of the tech and housing bubble.

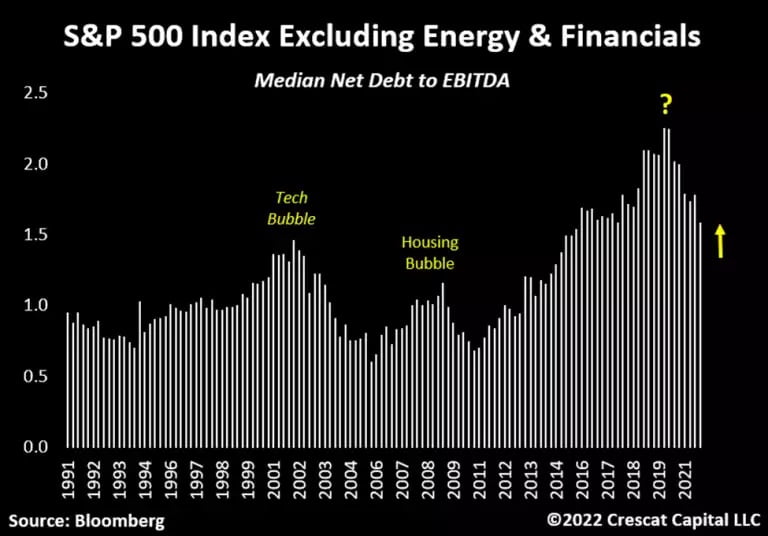

Unproductive Debt

The issue is that this overwhelming amount of debt has become incredibly unproductive. If we exclude energy and financial sectors, the median S&P 500 net debt to EBITDA ratio is also significantly higher than it was at the peak of the tech and housing bubble. As shown in the chart below, this measurement reached its highest level in June 2020 in the wake of the brief Covid recession. It’s bewildering to think that such a ratio still remains historically elevated at a time when corporate income statements are massively inflated. Imagine if we really are at peak earnings, how do we justify this level of leverage?

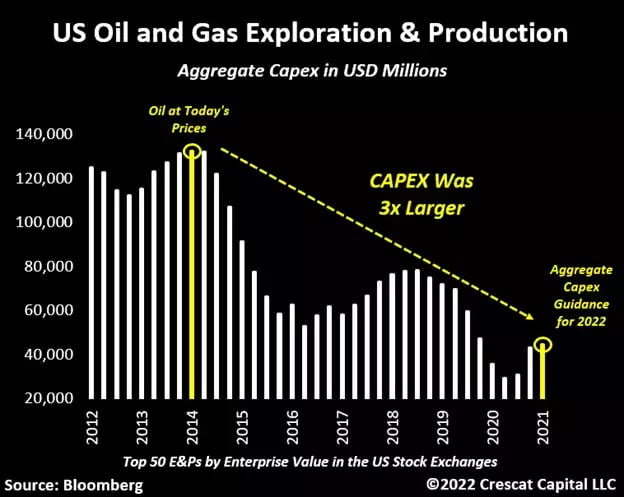

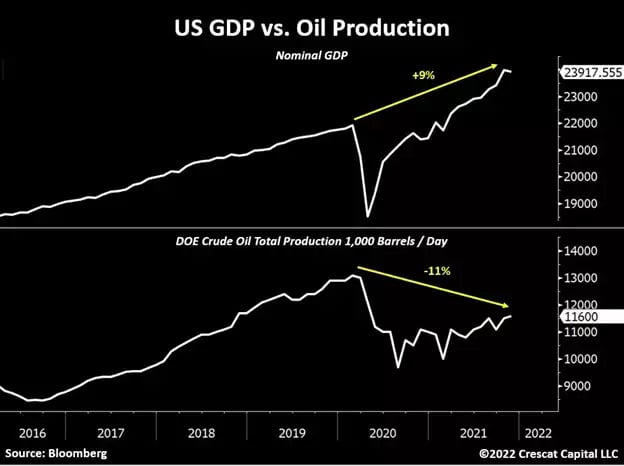

Oil Has More Room to Run

There are still an overwhelming number of people comparing today’s inflationary environment with 2008. In our view, the scenarios could not be more different. Back then, it was mostly just high energy prices and a housing bubble that was squeezing the consumers. Today, the consumer is being squeezed by rising prices across a wide range of goods and services. A structural peak in oil supplies was also a real concern back then, but capital investment in energy was raging at that time to far outstrip demand, so prices peaked. Today, it’s the opposite situation with severe underinvestment in a variety of resource industries, including oil and gas, and too little concern over these structural imbalances.

It is mindboggling to think that inflation is at 40-year highs, but oil prices are still below their $150 peak in 2008. What will CPI be when oil break out to new all-time highs? Also, recall that steep increases in energy prices have triggered recessions in the past.

Last time oil prices were at today’s prices, aggregate CAPEX for exploration and production companies was three times larger.

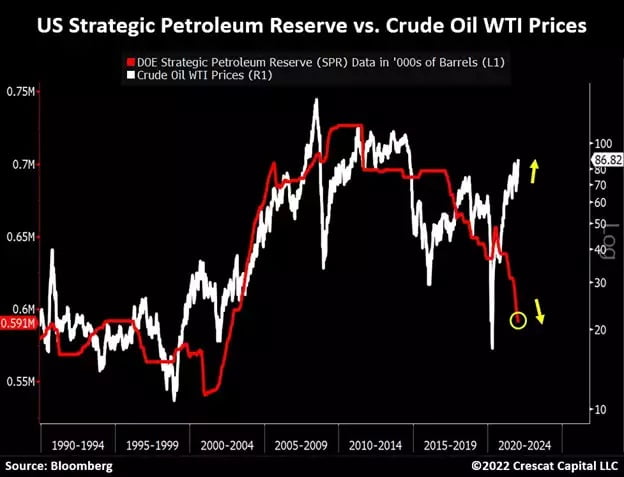

Remember when the US government decided to sell their Strategic Petroleum Reserves (SPR) to combat rising cost of fuel back in November? Well, oil is now at its highest price in seven years while SPR is at its lowest level in almost 20 years illustrating that there is little true “strategic” planning at all going in our government regarding our country’s energy supply and demand.

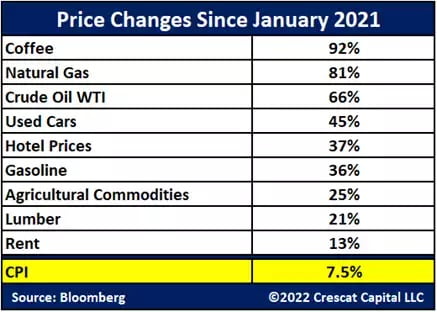

CPI Vastly Understated

We believe strongly that true inflation rates are significantly higher than the latest CPI print of 7.5% year over year. The chart below looks at a variety of price changes (YoY%) ending in January compared to what the Bureau of Labor Statistics calculates for the Consumer Price Index (YoY%). These are true price changes having a material impact on household budgets. Inflation is raging and CPI is not credible.

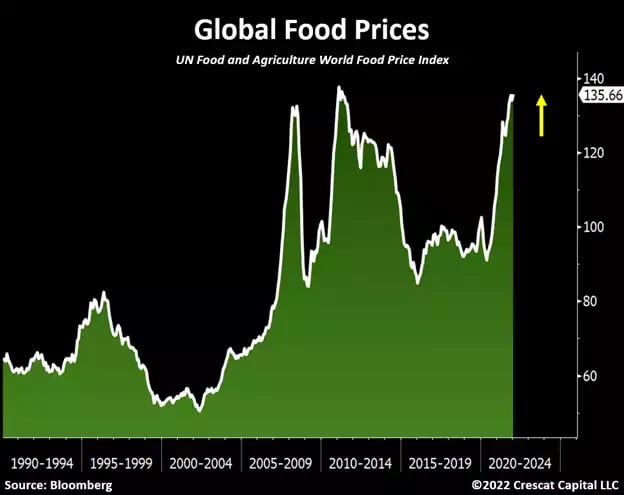

Global food prices are surging and starting to drastically increase the cost of living for the bottom 50%.

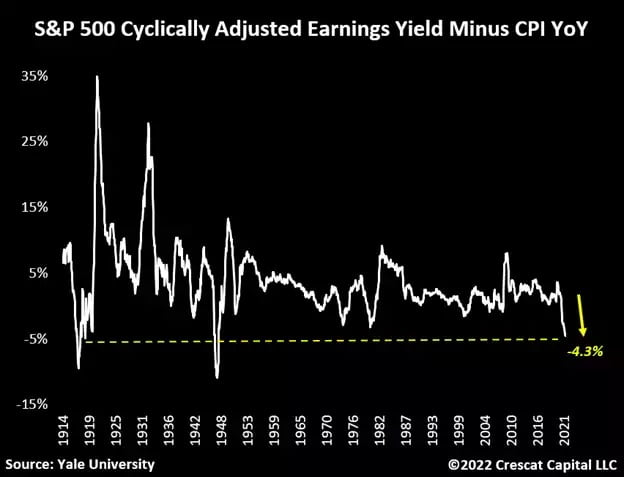

Most Negative Real Earnings Yield in 75 Years

If we invert Professor Robert Shiller’s Cyclically Adjusted Price to Earnings (CAPE) and subtract by inflation rates, today we have the lowest yields in 75 years. The last two times we reached such depressed levels were in 1917 and 1947. Most of those declines were driven by double-digit inflation rates. This time it’s driven by both excessive valuations and historically high inflation rates. US equity markets are extremely expensive today.

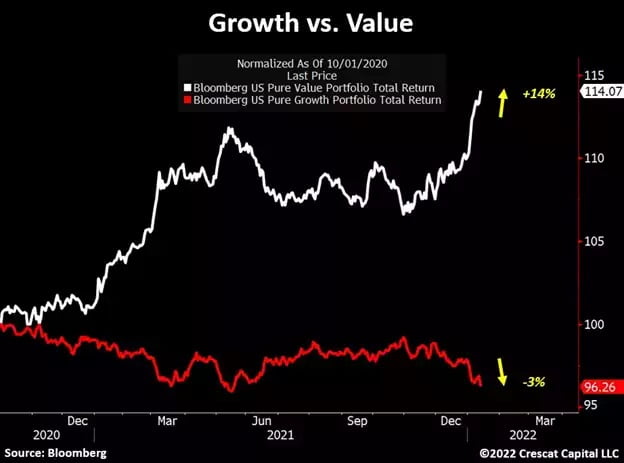

The Great Rotation

Investors today must act to save themselves because there is no policy action that will do it for them. We think investors need to get their skates on if they want to prosper and not perish from this shift. We believe the smart money is getting ahead of the curve in what is destined to be a massive rotation, if not a stampede, out of overvalued financial assets and into undervalued inflation-hedge assets. The valuation and growth disparities between financial assets (equities and fixed income securities especially long duration assets) and tangible assets (including scarce commodities and equities of raw material producers) have never been more compelling. At Crescat, we call this overriding theme “The Great Rotation”.

This idea is like the growth-to-value rotation already underway in equity markets, but at Crescat today, we specifically favor the energy, materials, and agricultural sectors within the value indices. We see risks in other perceived value sectors, that could be “value traps” especially in companies with bloated balance sheets and where profit margins are likely to be squeezed by rising labor costs in addition to rising raw materials prices.

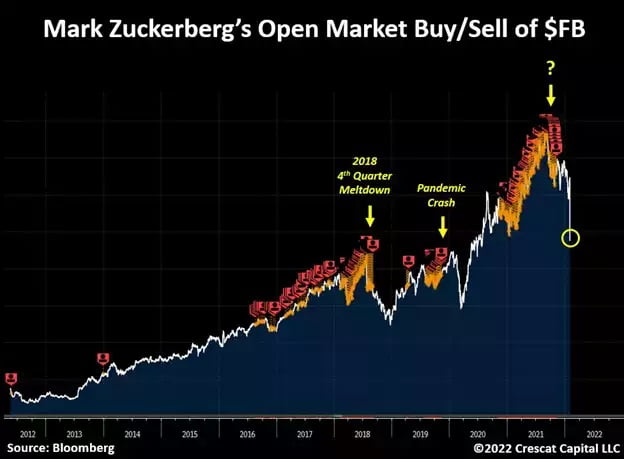

Insiders Want Out

Founders and insiders of major companies are selling shares, including Tim Cook, Larry Page, Elon Musk, Jeff Bezos, and Jen-Hsun Huang. Mark Zuckerberg sold Meta Platforms shares ahead of the last three times the stock crashed. This type of behavior is reminiscent of other major market tops.

Riskier Assets Leading the Way

Small and micro-cap stocks, which have a high correlation to the S&P 500 and equity market at large, are both already down on a year-over-year basis, suggesting other indices are at risk to follow the same path. Russell 2000 just turned negative on a year-over-year basis. If history is any guide, the S&P 500 should follow soon.

Other key parts of the equity market are already collapsing: Cathie Wood’s ARK ETF, ‘meme’ stocks, software companies, crypto funds, venture capital firms, and Chinese equities are just a few.

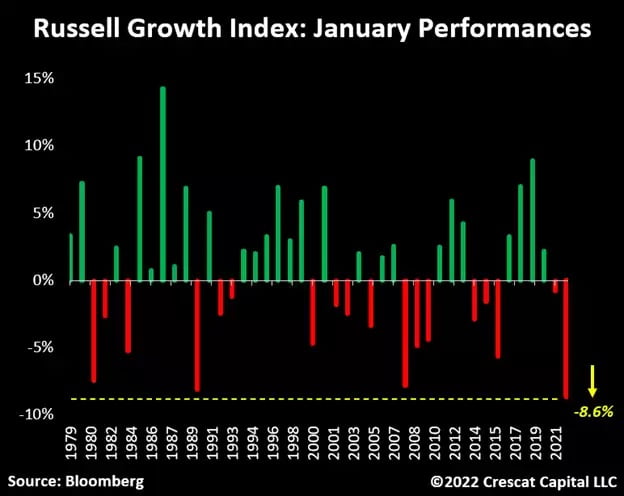

Also, Russell Growth index just had its worst January in history. It was the first time in over 30 years that Nasdaq and Treasuries declined as much as they did in one month. In our view, we are entering a new macro regime, the onset of a risk parity unwind.

SaaS Rationalization

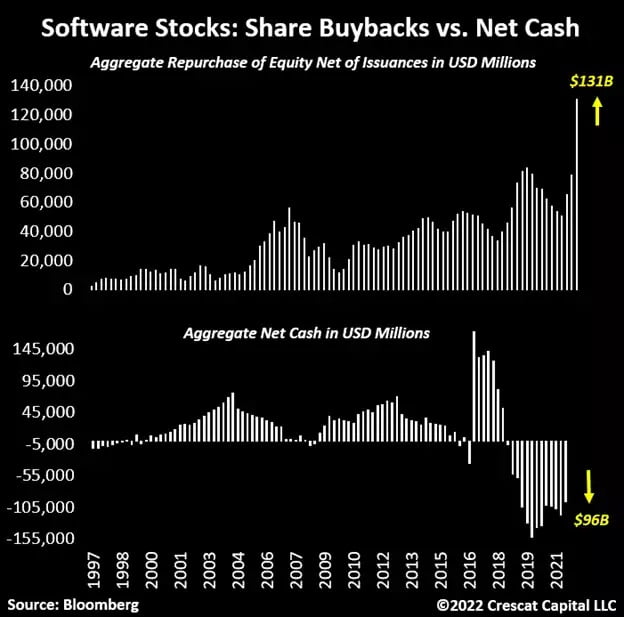

One of the leading industries of this cycle has been the software companies. These stocks have now underperformed the S&P 500 index by almost 30% since February 2021. This is an important sign that investors are starting to transition away from hyped and overvalued assets as part of the Great Rotation we have been calling for. Keep in mind that even after the recent selloff, software stocks still trade at similar multiples that we saw back in the tech bubble.

It is interesting how software companies just did their largest share buyback in history at these still highly elevated valuations and their stocks continue to selloff. As shown in the second panel of this chart, overall the industry increased debt to help finance equity repurchase programs.

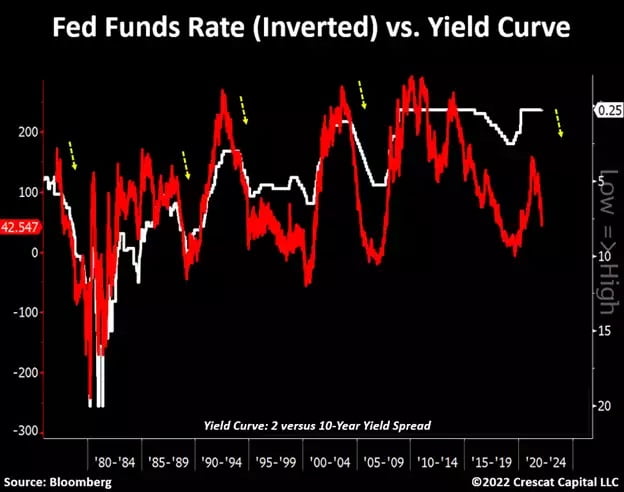

Rate Hikes Leads to Yield Curve Inversions

Historically, almost every time the Fed entered a tightening cycle, the 2 vs. 10-year yield curve flattened in tandem. We urge investors to pay close attention to this. A yield curve inversion is arguably one of the most bearish signals for financial markets out there. It almost always leads to an economic recession.

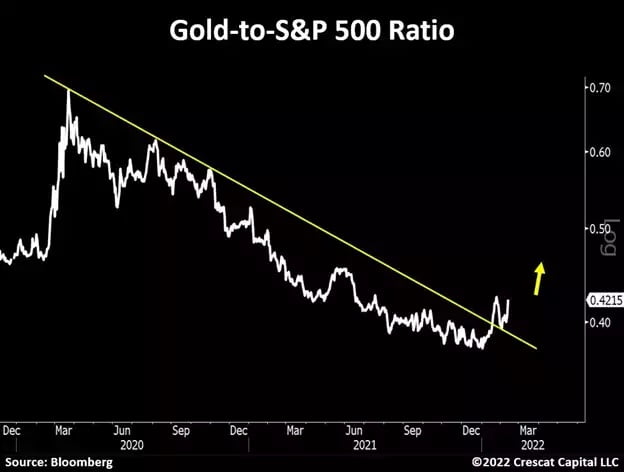

Gold Outperforming Overall Stocks

After a breakout from a two-year resistance level, the gold-to-S&P 500 ratio is holding its ground. We think this ratio is very bullish for the overall precious metals industry which remains in a long consolidation period. The weakness in the S&P 500 given the latest hawkishness by the Fed is one of the reasons this ratio has been rising. Gold performed well in December and has been going up in February month to date at same time as stocks have been falling.

Debt-to-GDP Resolution

We just had a major breakout in Japanese 10-year yields after forming a long-term double bottom. Central banks must allow long-term rates to rise first if they ever want to raise short-term rates. Almost all developed economies are experiencing the same.

dsadsa

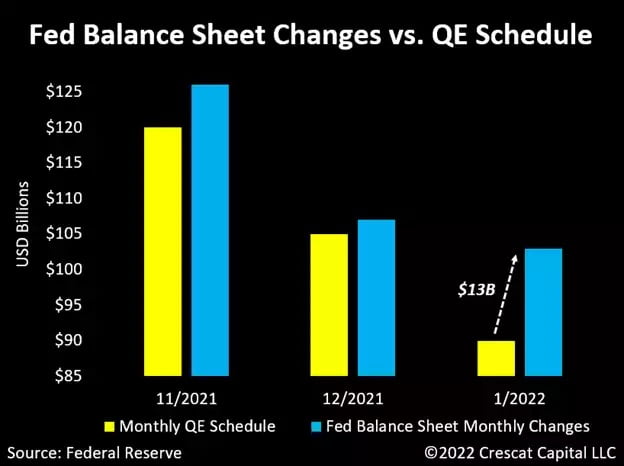

The Fed Just Can’t Resist Coming to the Rescue with QE

The Fed balance sheet continues to rise more than its tapering schedule, exceeding it by about $21 billion so far since November. The largest overstep was in January, almost $13 billion, which also happened to be the same time Nasdaq had its second worst January performance in history. Coincidence?

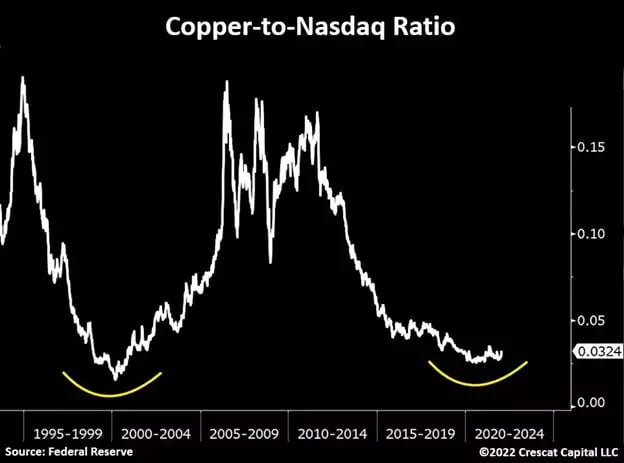

Copper is King in the New Green Economy

We would much rather own copper than Nasdaq, an undervalued, supply-constrained clean energy metal vs. a historically expensive index. The nice-looking double bottom formation in the Copper-to-Nasdaq ratio is just the cherry on top.

Suppressed Energy Production

For those calling for peak inflation soon, keep in mind that since the end of Q1 of 2021, natural gas and oil are up 85 and 55% each. In addition, we are yet to see the increase of owner’s equivalent rent in CPI after the largest house prices’ increase in 30 years. That doesn’t look like peak inflation to us.

Rising Fertilizer Prices Propel Agricultural Commodities

Agricultural commodity prices are being propelled higher by soaring global fertilizer prices that in turn have followed a surge in its key feedstock, natural gas. Around the globe, natural gas is used as a raw material as well as fuel for nitrogen fertilizer production. Prices for all material ingredients of fertilizer have risen sharply over the last year. Fertilizer export bans are also indicative of scarce supplies and contributing to rising prices globally. Last September, China banned exporting phosphate fertilizer to ensure domestic supply. Russia banned fertilizer exports soon after. Fertilizer supply constraints are not likely to go away soon. This has big implications for food price inflation still ahead of us.

A Supply-Demand Mismatch

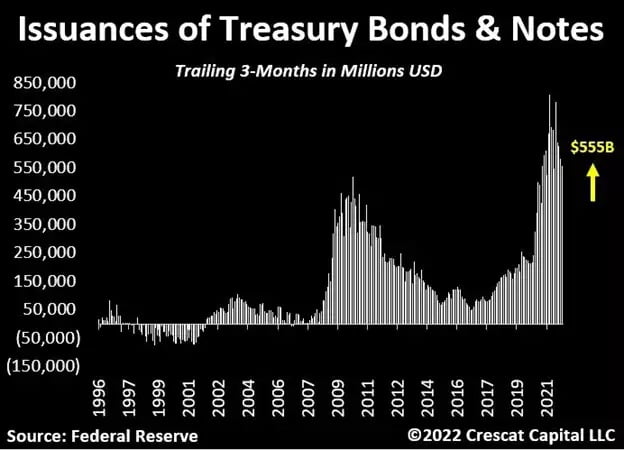

We just saw another $462 billion of Treasury bonds and notes were issued just in the last 2 months. Back in October 2021, the Fed was buying almost 50% of these issuances. Now it’s “only” buying 26%. No wonder nominal yields have been moving up. We think the 10-year yield is headed towards 2.5% to 3% and will likely cause major implications for long duration assets.

Crescat’s Investment Strategies

It is an exciting time to be running hedged investment strategies, like our Global Macro and Long Short funds, because the abundant opportunities to generate alpha by capitalizing on both the long and short sides of the markets. For those interested in just the long side, a portfolio of deep value investments today in the commodities and natural resource sectors should be a great way to get ahead of the inflation curve – where our Precious Metals and Large Cap strategies are focused on today.

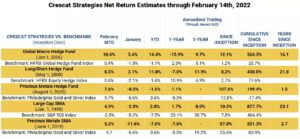

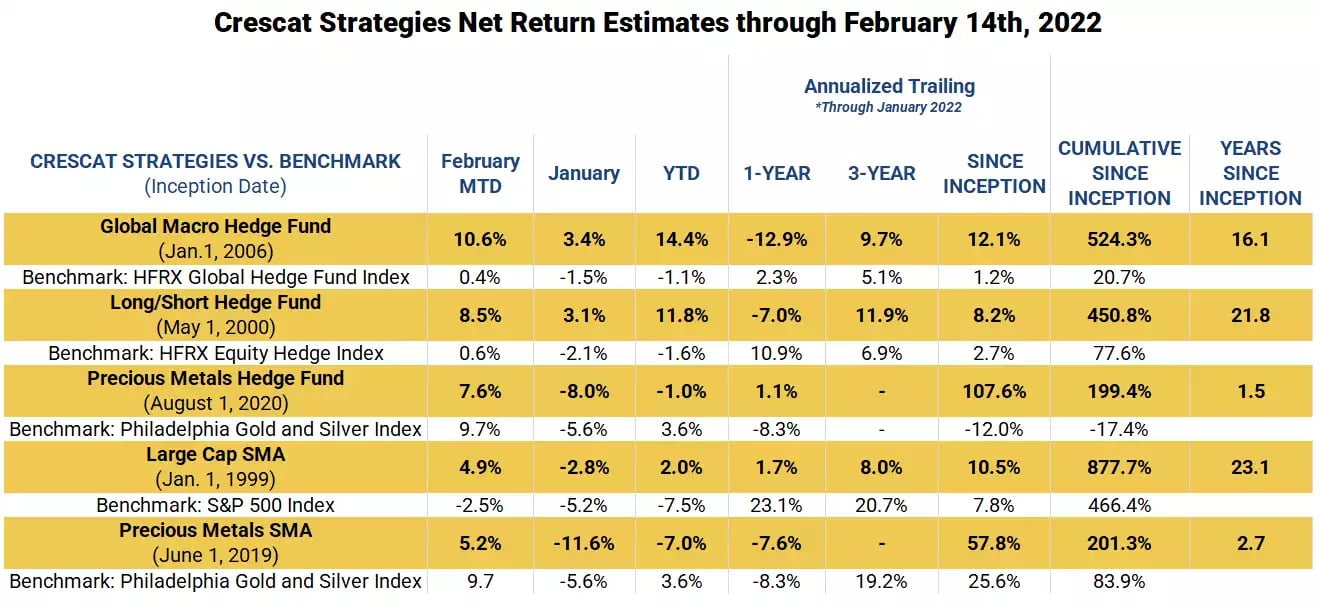

Official Performance through Year End 2021

Year-to-Date Estimated Performance

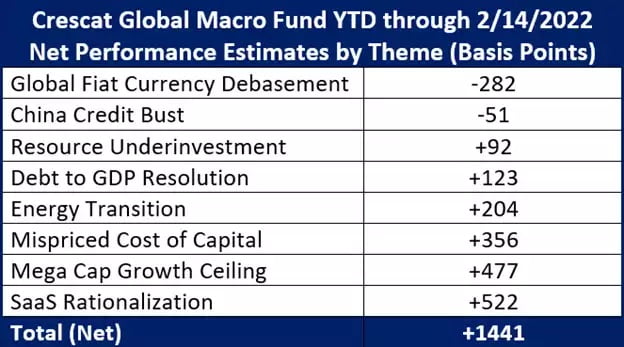

YTD Profit Attribution by Theme

Crescat Capital is a global macro asset management firm. Our mission is to grow and protect wealth over the long term. Our goal is industry leading absolute and risk-adjusted returns over complete business cycles with low correlation to common benchmarks. We encourage you to reach out to a Crescat representative to learn more about any of our five strategies. You can find both Marek Iwahashi and Cassie Fischer’s contact information below.

Sincerely,

Kevin C. Smith, CFA

Member & Chief Investment Officer

Tavi Costa

Member & Portfolio Manager

For more information including how to invest, please contact:

Marek Iwahashi

Client Service Associate

303-271-9997

Cassie Fischer

Client Service Associate

(303) 350-4000

Linda Carleu Smith, CPA

Member & COO

(303) 228-7371

© 2022 Crescat Capital LLC

Updated on

Sign up for ValueWalk’s free newsletter here.