{kind=link}

By Due. Originally published at ValueWalk.

When was the time you checked your savings account? If it’s been a while, I’m sure that you were expecting a big, juicy return. Guess what? You’re probably severely disappointed to find out that you’ve made nothing.

Q4 2021 hedge fund letters, conferences and more

Considering that your bank is paying you a measly 0.00000000000000001% this shouldn’t be all that surprising. But, why is your bank treating you that way?

Banks often pay low-interest rates on savings accounts. At the moment, the national average interest rate is 0.06% and inflation is around 5%.

Financial institutions profit from having higher borrowing rates than the rates they pay people who deposit money into savings accounts. And, this is one reason why savings account rates are so low. To keep making free money on savings accounts, banks keep loan rates low so they can make money on loans.

Another reason? Some banks may not need to offer higher interest rates is that they’ve already attracted a large number of customers and aren’t competing aggressively for new customers, according to research conducted by Itmar Drechsler, a professor of finance at the University of Pennsylvania.

To make matters worse, if you’re dealing with a big bank you may have to shell out pesky account fees. And, don’t get me started on the unresponsive customer service who could care less about how much money you’ve got in your bank account.

To be fair, though, I’m not completely hating banks. It’s a safe location to park your money. And, these historically low-interest rates are awesome if you’re looking to pay your first home or refinance your mortgage. But, if you want to make money, instead of losing it, check out these 9 banking alternatives.

-

Neo Banks

In the past few years, several financial technology companies have emerged that offer mobile-first banking services, including low-cost checking accounts. A Neobank, such as Chime and Current, can partner with a bank to provide accounts. And, in rare cases, becomes a bank itself. No matter how you slice it, neo banks are FDIC-insured and can act as regular online bank accounts.

By using technology, these institutions provide services other banks and online banks cannot. I’m talking about perks like two-day-early direct deposits and 24/7 access. There are also no costs associated with maintaining branches. So, these savings are passed on to customers through lower fees and competitive rates.

Let’s take Chime as an example here. With a 0.50 percent APY, Chime is one of the best online savings accounts currently available. When compared to traditional accounts, you can grow your funds faster with this high-yield account. If you have at least a penny in your account, you’ll earn interest. And, there’s no cap on the amount of interest you can earn.

When you make purchases, you can even save even more with the Save When You Spend feature. Chime rounds your debit card transactions up to the nearest dollar and transfers the difference to your Savings Account whenever you use your Chime debit card.

-

Treasury Inflated Protected Securities (T.I.P.S.)

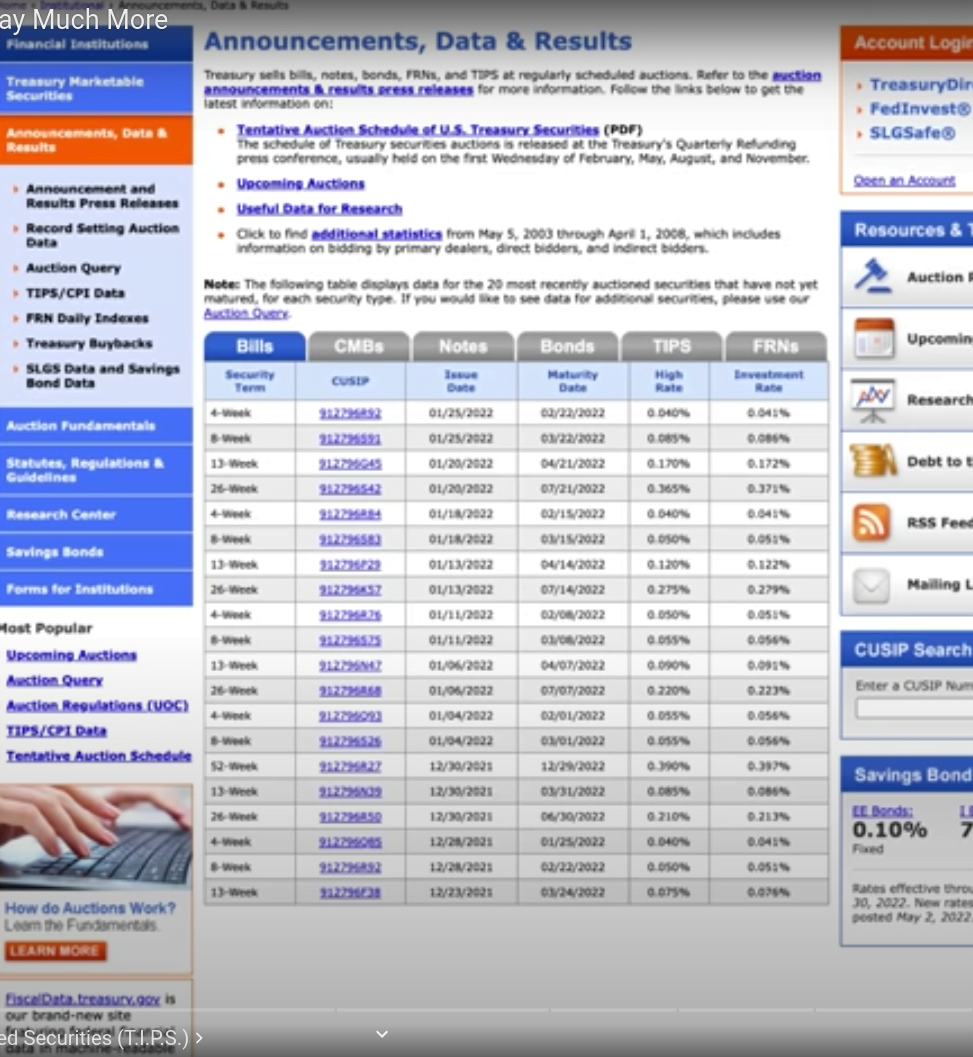

You can buy Treasury Inflated Protected Securities online at TreasuryDirect.gov. These are issued by the government and are known as T.I.P.S. for short. But, how exactly do they work?

They are tied to the CPI or the consumer price index. Here’s some Economics 101 for you. The CPI basically measures what goods and services are being paid for. Prices are going up or down, so in theory, if inflation starts to increase you’ll see the CPI go up, and then what T.I.P.S. are paying will also increase, so the yield should go up.

Here’s where things get really cool. The tax features of T.I.P.S. are that when you buy a tip you don’t have to pay state or local taxes if you want to buy them they start out at a hundred dollars and increase by a hundred dollars at a time.

You can check out TreasuryDirect.gov to know what the current interest rate and yield are on tips. By selecting the column mark T.I.P.S., you will scroll through the terms, and you will be able to see the yield. From there you can figure out how much you’re going to make.

TreasuryDirect.gov is where you can learn what the interest rate or yield is on a TIP if you bought one. There you’ll see different columns, so select tips and it’ll show you the yields that are currently paying and the various terms.

-

Online Investment Apps

AMC or GameStop are common examples of meme stocks you purchase through online investment apps like Robinhood.

So, here’s the deal with Robinhood. As opposed to most online brokers, Robinhood does not offer mutual fund trading. They only support stocks, ETFs, and cryptos. Despite offering commission-free trading, Robinhood makes money from your business in several ways.

It works like a neo bank in the sense that you can open up an account, get a debit card, and start purchasing items. There are also ATMs all over the country if you need cash.

And guess what they’re paying? Point three percent. While that’s not a huge amount, it’s still more than the national average.

But, Robinhood isn’t your only option. There are also apps like M1 Finance. You receive one percent from their M1 Plus program. In addition, they offer a debit card with a one percent cash back. The only catch is that charge $125 for this account. But, your first year is free.

-

High Yield Bonds

From a technical standpoint, high-yield bonds are pretty much the same as regular corporate bonds because both provide debt issued by a firm with the promise of paying interest and returning capital at maturity. With junk bonds, however, the credit quality of the issuer is poorer.

There are two basic bond categories, high-yield and investment-grade, based on this credit quality. According to the major credit rating agencies, high-yield bonds have lower credit ratings. A bond rated below “BBB-” from S&P or below “Baa3” from Moody’s is considered speculative and will have a higher yield. An investment-grade bond is one that has a rating at or above these levels. Bonds with ratings of “C” or lower could default as low as “D” (currently in default).

In spite of their “junk bond” image, high-yield bonds have been found to have higher returns than investment-grade bonds for most long-term holding periods. At the same time, high-yield bonds come with default risk and market volatility. So, definitely talk to a financial advisor before switching over.

If you’re interested, though. I recommend checking out the American Century High Income Fund and the Nuveen High Municipal Bond Fund.

-

High Yield Stocks

Let’s say in the realm of high yield. But, we’re gonna look at high yield stocks.

“When you’re seeking out high-yield stocks, remember: You need more than headline yield – you also need an element of safety,” advises Brian Bollinger over at Kiplinger

“In today’s world, which is characterized by historically low-interest rates, stocks with eye-popping dividend yields are often too good to be true,” he adds. Investing in high-dividend stocks requires extra scrutiny to avoid falling into yield traps due to dangerous debt loads or declining businesses. Those looking for retirement stocks that can generate income for decades into the future should take note — especially since some of these stocks offer returns between roughly 5 and 9%.

“Research firm Simply Safe Dividends developed a Dividend Safety Score system to separate stocks with safe dividends from those that are more likely to cut their payouts over a full economic cycle,” says Bollinger. “By focusing on companies with more conservative payout ratios, stronger balance sheets and business models that generate predictable cash flow, investors can improve their chances of selecting dependable income investments.”

-

Blended Approach

Do you want a little bit of high-yield stocks and bond investments? Would you also like to keep some in that high-yield savings account? If so, then a blended approach might be right up your alley.

The easiest way to make this transition is if you already have a Robinhood, Betterment or M1 Finance account. Because you have money in their high-yield cash management programs, you can start adding stocks or ETFs now.

Personally, I think that M1 has a slight advantage since you can assemble your investment pie however you like.

-

Real Estate Investment Trust (REIT)

The purpose of real estate investment trusts, or REITs, is to pool investors’ funds to buy and fund income-producing properties. Commercial properties like office buildings, apartment complexes, or hotel buildings are owned by REITs. Through stock investments in those companies, you can invest in real estate without owning any of the actual properties.

There are many reasons why REITs appeal to investors. The first benefit is that, since you do not own the properties, you do not have to maintain them. Another benefit is that, in general, REITs pay higher interest than other kinds of investments. The reason for this is that companies are required to distribute 90% of their taxable income to their investors as dividends.

Additionally, when you invest in REITs, you have the option of reinvesting the income you earn from them, so your investment (and income) will grow even more.

Investments in REITs can be made through major brokerage firms (i.e. the New York Stock Exchange or NASDAQ), or through non-traded REITs. You might want to stick to publicly traded REITs if you are new to the concept because they are more liquid and easier to sell than non-traded REITs.

REITs may require a significant amount of money from investors if they’re considering buying real estate properties. For example, the minimum investment for many REIT companies ranges anywhere from $1,000 to $25,000.

-

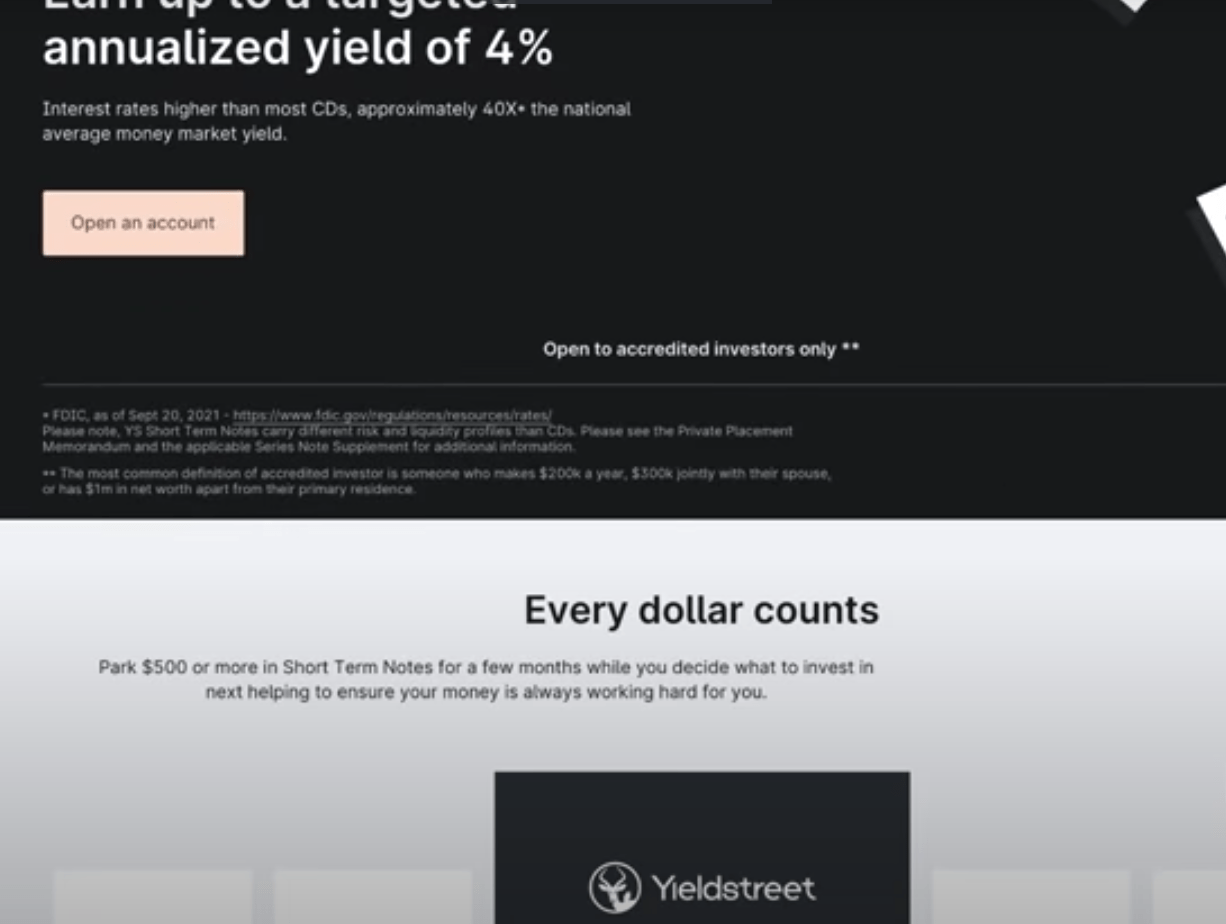

Short-Term Notes

A short-term note is a financial product that provides investors with the opportunity to earn interest over a 120 or 180-day period. A note’s maturity date is when the note’s investors receive their principal along with monthly interest payments. That means this is perfect for investors who are looking for an extremely liquid financial product.

Investing platforms such as Yieldstreet raise funds through their Short Term Notes program, along with warehouses and credit lines, to finance investment opportunities.

Interest rates on Yieldstreet are higher than most CDs, approximately 40X the national average money market yield. Additionally, you can roll over maturities in order to build an optimal investment strategy by investing multiple times.

-

Crypto Savings Accounts

Last, but definitely not least, are crypto savings accounts.

Full disclosure here. This is the riskiest baking alternative. On the flip side, rates can be outrageously high.

BlockFi, for instance, advertises rates that range from 0.10% to 9.50%. Another option, Celsius, offers several yields of around 9%. There’s even one with one nearly at 14% for Americans and a 17% rate for international customers. By contrast, the highest-yielding savings accounts tend to have interest rates of between 0.50% and 0.75%. And, if you forgot, the national average rate for a regular savings account is 0.06%.

How exactly does a crypto savings account work?

In general, a crypto interest account lets you earn interest on digital assets you bought on a crypto platform. In return for interest, you lend bitcoins or altcoins to other people. It actually functions similarly to how savings accounts work at traditional banks. You deposit money, the bank borrows it, and you are repaid plus interest. Generally, you can withdraw your money whenever you want.

Article by Jeff Rose, Due

About the Author

Jeff Rose is an Iraqi Combat Veteran and founder of Good Financial Cents. He teaches people wealth hacking. He is a frequent on CNBC, Forbes, Nasdaq and many other publications. He is author of the book “Soldier of Finance: Take Charge of Your Money and Invest in your Future” where he teaches how he escaped from $20,000 in credit card debt to a life of wealth.

Updated on

Sign up for ValueWalk’s free newsletter here.