{kind=link}

By Umair Tariq. Originally published at ValueWalk.

Black Bear Value Partners commentary for the first quarter ended March 31, 2022.

“A nickel ain’t worth a dime anymore.” – Yogi Berra

To My Partners and Friends:

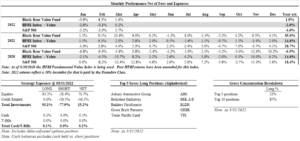

- Black Bear Value Fund, LP (the “Fund”) returned +1.6% in March and +1.9% YTD.

- The S&P 500 returned +3.7% in March and -4.6% YTD.

- The HFRI Index returned +0.2% in March and -2.6% YTD.

- We do not seek to mimic the returns of the S&P 500 and there will be variances in our performance.

- Note: 2022 returns reflect our reduced 10% incentive fee.

Q4 2021 hedge fund letters, conferences and more

Note: Additional historical performance can be found on our tear-sheet.

I write to you amidst a volatile market with a good dose of geopolitical and global economic uncertainty. While Black Bear is up on the year, I want to caution everyone that in this environment, markets can act irrationally, and I would not expect our partnership to always be immune. That said, as I will discuss below, we are positioned to do well in this environment both in terms of the investments we have and our ability to deploy capital when others are retreating.

From time to time I am asked the following question: “What’s the market telling you?” It can be disappointing or even offensive when I say, “seems like more sellers than buyers” or “the market tells me people haven’t changed too much.” Stocks SHOULD be viewed as proportional shares of businesses no different than the dentist down the street or your local bank. However, due to the auction-driven stock market, stocks serve as an extension of people’s emotions which can be quite volatile. On their own, stocks wouldn’t do anything…PEOPLE do things and people can be extreme in their opinions and behaviors. As a result, stocks just tell me how people may be feeling in the moment independent of the business. This is the opportunity for the fundamental investor. Often when people get scared, they sell to avoid future mark to market losses independent of business fundamentals. We are invested based on what the business is telling us…not the stock…and utilize opportune discounts in the market to our advantage.

Brief Discussion on Homebuilding/Housing

Frequently people seem intent on fighting yesterday’s battles. Housing led the last multi-year downdraft causing many today to try and paint parallels. The valuations in homebuilding and homebuilding-adjacent businesses are extremely cheap and incorporate a lot of bad news. This theme is a meaningful portion of our portfolio. While mortgages are more expensive today than they were 3 months ago, they are still cheap in absolute and historical terms. While higher mortgages rate reduce affordability increased wages can help mitigate that issue. Underwriting standards have improved since the financial crisis. In fact, it isn’t that easy to get a mortgage with all your documentation in order.

The industry is healthier both in terms of operating efficiencies/scale and healthy balance sheets. If business slows down, it will not be 2008 redux.

Right now, there is 1.7 months of supply of existing homes. That is not a lot. People have a choice to rent or buy. Current rental vacancies are ~5.6% which matches the multi-decade lows and contrasts with ~10% vacancies in the lead up to the GFC. Additionally, the 0.9% homeowner vacancy rate ties the lowest level on record and is below the 1.6% long-term average and peak of 2.9% in 2008 (Thanks to the team at Credit Suisse for this info.)

Home prices are up because people need places to live and we have had chronic underbuilding for a decade. We need more homes, and we need them in the locations people are moving. National averages are not helpful as we own a builder in specific areas of the country. Additionally, averages obfuscate the economics to each mover. For example…homes in Florida may be more expensive relative to past homes in Florida…but not to homes in New York/New Jersey/Connecticut. Affordability is relative.

Inflation/Credit Shorts/Pricing Power

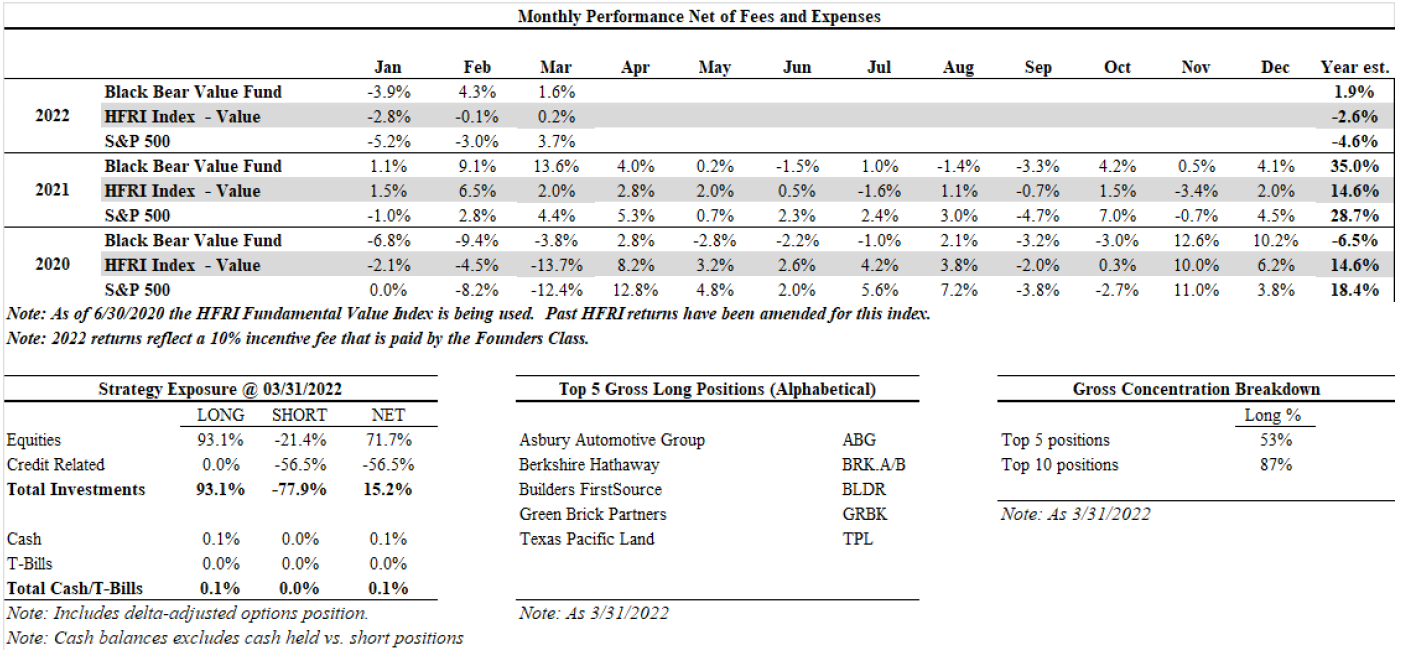

As a reminder we are short ~ 57% of the fund in various credit instruments. The investment is predominantly but not solely in options so 57% of our portfolio is not at risk.

With inflation rearing its head and proving not to be a temporary guest, the cost of money, AKA interest rates, has become an en vogue discussion topic. Is inflation transitory? No clue. But you generally do not roll back wages when you have increased them. Some of the inflation will remain here and set a new baseline for the future. As supply chains normalize inflationary pressures should decrease. However, the world is one big chain reaction and if wheat is not flowing from Ukraine and natural gas/oil is not flowing from Russia to the EU, the dominoes can hit in unpredictable ways both in magnitude and duration.

While credit instruments have widened it still does not make sense that a fair price for credit is in the low-mid single digits. Additionally, there seems to be a big push domestically for increased compensation for labor. This will hurt operating margins for many companies and impair their credit profile. In a less accommodating interest rate environment we may see something that we have not in a while…companies defaulting! People are accepting a lousy return considering inflation and default risks. The real return of these investments is negative.

As a result, we remain short credit instruments that range from US Junk to Investment Grade to Emerging Markets. I am still dubious that ETF’s can orderly handle a massive sell-off in credit. If the government had not stepped into the market in March 2020 these instruments would have had liquidity issues.

We own businesses that have pricing power and limited/no dependance on the need for external funding. This is important because as input and wage costs pressure profitability of many companies, our businesses should be able to weather the storm and capitalize thru both organic market share gains and/or acquisitions of companies that may not have had a healthy balance sheet or operating structure.

In a vertical market, where money losing companies can seize on the markets imagination and raise endless funds, the staid and true businesses seem a lot less interesting. Times may be changing and those businesses that can endure will benefit those who own them.

Top 5 Businesses We Own

Asbury Automotive Group

Asbury Automotive Group, Inc. (NYSE:ABG) has many similar qualities to AutoNation, Inc. (NYSE:AN), which we held for the last 5+ years. I don’t typically discuss portfolio activity but given the long-holding and likely questions, I figured I’d address the change in our holdings here.

While I admire the AutoNation business there has been a management change and an accompanying change in strategic and capital allocation priorities. It was painful to sell the business as it had been one of our core investments and I believed they were on a great track. Management’s strategy may wind up being successful, but it is different than what I underwrote and as a result a change was needed for our portfolio. I express my thanks to the team at AutoNation as our Partnership has benefited from your stewardship.

Asbury had been in the portfolio before. Entering COVID, I decided to concentrate our auto dealer investments into AutoNation. ABG is run by highly capable management who have made 2 accretive and sizeable acquisitions in the past 18 months. The fundamentals of both businesses are similar though there are some differences of note.

First a couple negatives. AutoNation has a name brand, whereas Asbury does not. While it’s hard to value what a brand is worth there is value attached to the AutoNation name that we will not have at a corporate level with Asbury. However, at the dealership/consumer level I am not sure there is much of a difference.

Second, Asbury has a fair amount of debt (2.8x proforma for acquisitions). I would expect this number to decline both as the operating business performs and debt is reduced.

One of the positives of Asbury is their recent acquisition of the Larry H. Miller Group. Typically, most auto dealers receive a commission when a service or warranty plan is sold with the purchase of the vehicle. The Miller Group has built an internal business that operates those plans which are both high margin (20+%) and sticky throughout the lifetime of a customer. As ABG rolls these plans out to their existing dealerships there is an opportunity for meaningful increases in cashflow for every customer transaction.

Inventories for cars remain tight and the unit profitability is still unusually high. I underwrite the business on a “steady-state” basis removing the benefits from reduced inventory. Two changes from this pandemic will likely remain in the industry.

First, OEM’s and dealers have historically been in a PUSH model where OEM’s send lots of inventory that sits on dealers’ lots. Both have witnessed that with reduced inventory, everyone wins (well maybe not the customer as much.) Working capital needed for inventory is lower and returns on capital and absolute profitability have increased dramatically. It stands to reason that dealer lots will not be stuck with 60-90 days of inventory when supply chains normalize.

Second, as digital business continues to grow, the need for headcount at the dealership declines. Most dealerships have managed to grow their businesses without much growth in employees. This operating leverage should continue to increase as dealerships become more fulfillment centers than showrooms/selling spaces.

ABG should be able to generate steady-state free-cash per share of $20-$30 implying we own the business at a 12-20% free-cash flow yield on quarter-end pricing. We should do well with or without much growth in the business.

Berkshire Hathaway

Below is the rough Berkshire Hathaway Inc. (NYSE:BRK.A) on-a-napkin valuation I like to do periodically. Recently BRK acquired Alleghany for $11.6BB. I assume a reduction in cash for this amount and an increase of $550MM in operating income. I do not give benefit to the increased float nor any synergies. Again, this is a rough exercise to sanity check our assumptions.

- Cash of ~$103,000 per class A Share (vs. $104k 1 year ago)

- Down/Base/Up marks cash at book value to an 8% premium (vs. to 10% a year ago)

- Investments based on December prices ~$248,000 per class A share (vs. $194k a year ago)

- Presume a range of stock prices that result in:

- Down = $149,000 per class A share (-40%- assumes portfolio is overpriced)

- Base = $211,000 per class A share (-15% – assumes portfolio is overpriced)

- Up = $285,000 per class A share (+15%)

- Presume a range of stock prices that result in:

- Operating businesses that should generate ~$17,000 of pre-tax income per Class A share (vs. $15k)

-

- Down = 9x = $153,000 per share – equates to ~8% FCF yield

- Base = 12x = $204,000 – equates to ~6% FCF yield

- Up = 12x = $204,000 – equates to ~6% FCF yield

-

- Overall (vs. $529,000 at quarter end)

- Down = $413,000 (-28%)

- Base = $526,000 (fairly priced)

- Up = $600,000 (13% underpriced)

Going forward I expect Berkshire to compound at good, not great returns. The likely question is why own it at all if we expect modest returns…

BRK is a collection of high-quality businesses, excellent management, and a good amount of optionality in their cash position. If the cash were to be deployed accretively the true value would be greater than an 8% premium (as mentioned above). The combination of a pie that is growing, an increasing share of said pie due to stock buybacks, upside optionality from cash and a tight range of likely business outcomes that span a variety of economic futures gives me comfort in continuing to own Berkshire.

Builders FirstSource

Builders FirstSource, Inc. (NYSE:BLDR) is a supplier and manufacturer of building materials for professional homebuilders, subcontractors, remodelers, and consumers. Their products include factory-built roof and floor trusses, wall panels and stairs, vinyl windows and custom millwork.

The fundamental discussion about homebuilders applies to BLDR. As more homes are built across the country, there will be an increased need for scaled sourcing of products to homebuilders. There is a large amount of fragmentation in the supply chain which provides BLDR a long runway for acquisitions and realistic synergies.

The management team has been using their prodigious free cash flow to both acquire new businesses and buy in their stock. While I historically always liked their business, their historic high-debt levels gave me pause. They have right sized their balance sheet and are taking a very thoughtful view on capital allocation on behalf of shareholders.

BLDR should be able to generate $7-$10 a share in cash in the medium term with significant upside if they can scale through acquisition and/or further penetrate existing markets. We own it at a 11-15% free-cash flow yield so little growth is needed for us to compound value at high rates.

Green Brick Partners

Green Brick Partners Inc (NYSE:GRBK) is a residential land developer and homebuilder. Most of their operations are in Texas, Georgia, and Florida. GRBK was formerly a private partnership between Jim Brickman and entities related to Greenlight Capital (managed by David Einhorn). David is currently the Chairman of the Board.

As discussed earlier, there is a long-term fundamental supply/demand imbalance in housing inventory. This is a direct result of underproduction of new homes amid a challenging mortgage financing environment over the last 10+ years since the Great Financial Crisis. Looking forward we should have increased housing demand from millennials as they enter the family-phase of life and desire more space.

It is rare to be able to partner with an excellent operator and an excellent capital allocator. As evidenced by our investment in AutoNation, when you marry those 2 concepts you can wind up with a wonderful result. GRBK has been reinvesting their cashflow in additional lots/land inventory. This masks the earnings power of the company. The company is valued somewhere between 5-8x steady-state earnings and potentially even cheaper than that. I tend to be more conservative given the potential for rate rises and inflationary increases in development costs. We have high-quality stewards at both the operating and Board level.

Texas Pacific Land

Texas Pacific Land Corp (NYSE:TPL) had fallen out of our top 5 in our past letter due to the increase in value of other investments and a modest reduction in our holdings. Additionally, I was cautious as there were some corporate governance issues to be addressed. We appreciate and express our thanks to management as well as some of our fellow shareholders for resolving one of the matters and having the unqualified Board Member exit the Board of Directors.

As a reminder, TPL is a royalty company with 100% of their acreage located in the Texas Permian Basin. In a nutshell they make money when drilling activity occurs but DO NOT have the capital needs as they simply provide access to land.

The incremental amount of work on TPL’s part is minimal as the extraction and movement of the oil/natural gas is undertaken by others. They are merely a toll collector with Returns on Capital of 80+%.

In an inflationary environment, businesses that have lower capital intensity both in capital assets and people stand to benefit. In other words, if oil goes up a lot, the incremental cost to TPL is close to 0 so it’s all incremental profit. This is a business that should benefit in a massive way if we have energy inflation. In the meantime, we likely own it at a 3-4% free cash flow yield with massive upside.

Ukraine

Part of this job is constantly reading the news and staying abreast of both national and world events. Every day I read the tragic stories about the unneeded bloodshed in Ukraine. As hard as it might be for us all to read it, it’s important to bury our nose in it and consider how we would feel if it was our family and friends. It is in that light that I decided to donate our February management fees to various Ukrainian efforts to help children. I would implore you to not ignore bad news. During our good days we need to remain sober and empathize with those less fortunate. Thank you to our partners who have both contributed thru their management fees and on their own to these causes. I hope that as our business grows, we can collectively do more.

Fund Updates

As the Fund has grown, we have had to make additional filings with various regulatory agencies. During Q1 we filed with the SEC to become an exempt reporting advisor.

2021 K-1’s should have been received. If you are not in receipt, please let me know. This was a higher-tax year than the previous 4. It seemed like there was a possibility for higher capital-gain rates in 2022 so I made the determination to realize some gains in 2021.

Our portfolio and business structure are set up to thrive in rocky waters. I am finding high-quality/inexpensive businesses to own and feel that we have some downside insurance protection from our equity and credit shorts. We will not chase or use our imagination when investing our capital. If we can stay sane when others are acting reckless, we can protect capital during tough times and take advantage of dislocations. Over the last 5-10 years there has been a lot of foolishness and creative investing which provides us a competitive advantage over the coming years.

Thank you for your trust and support.

Black Bear Value Partners, LP

Adam@BlackBearFund.Com

www.blackbearfund.com

Updated on

Sign up for ValueWalk’s free newsletter here.