{kind=link}

By John Huber. Originally published at ValueWalk.

Saber Capital Management’s commentary for the month of May 2022, titled, “Mental Tension and the Value of Falling Stock Prices.”

Dear Investment Partner,

In a recent interview, Ted Weschler described his investment process as an eclectic collection of different reading material that is likely unique to him. For example, he mentions reading USA Today, Furniture Daily, and Uranium Weekly, three completely different types of publications with very different audiences. He says the combination of those three very different sources (among many others) gives him a unique perspective on certain companies that occasionally results in a differentiated insight — a way of thinking about a company in a way that varies from the conventional view. These unique insights are what we all need as investors.

Q1 2022 hedge fund letters, conferences and more

I like Ted’s approach, partly because it justifies my own preference for reading a variety of different topics, from business filings to trade magazines to global news to sports to health and exercise, and more. Weschler said that he believes he can gain these insights because his reading material is unique only to him. Each publication he reads has many other readers, but there is no other person who reads exactly the same combination of his reading material. It’s like he’s creating his own unique code base inside his brain that only he has access to.

I got to thinking about how not only do we create a unique database in our minds based on the specific collection of material we study, but also how this code base is continuously getting updated every time we read something (or have a conversation, or join a meeting, or listen to a podcast, etc…).

And what’s interesting about this is because the mental database is constantly changing, you can actually read the same thing you’ve read previously (re-reading a book for example) and come away with a completely different understanding, sometimes even an opposing view from what you held before. I’ve noticed this numerous times, as I happen to (weirdly) like rereading the same books numerous times.

Emboldened by this newfound justification for my strange habit of rereading the same thing, I am steadily working my way through the old Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) annual meeting transcripts (videos are also on Youtube). The Berkshire meeting videos and the Buffett shareholder letters are definitely examples of things you can reread multiple times and continue to learn something new. Each time I reread the letters, I always find something relevant to a current company I’m researching or a current investing or business topic I’m thinking about. And since history often repeats itself (or at least rhymes), sometimes these old letters reference a situation that is very applicable today.

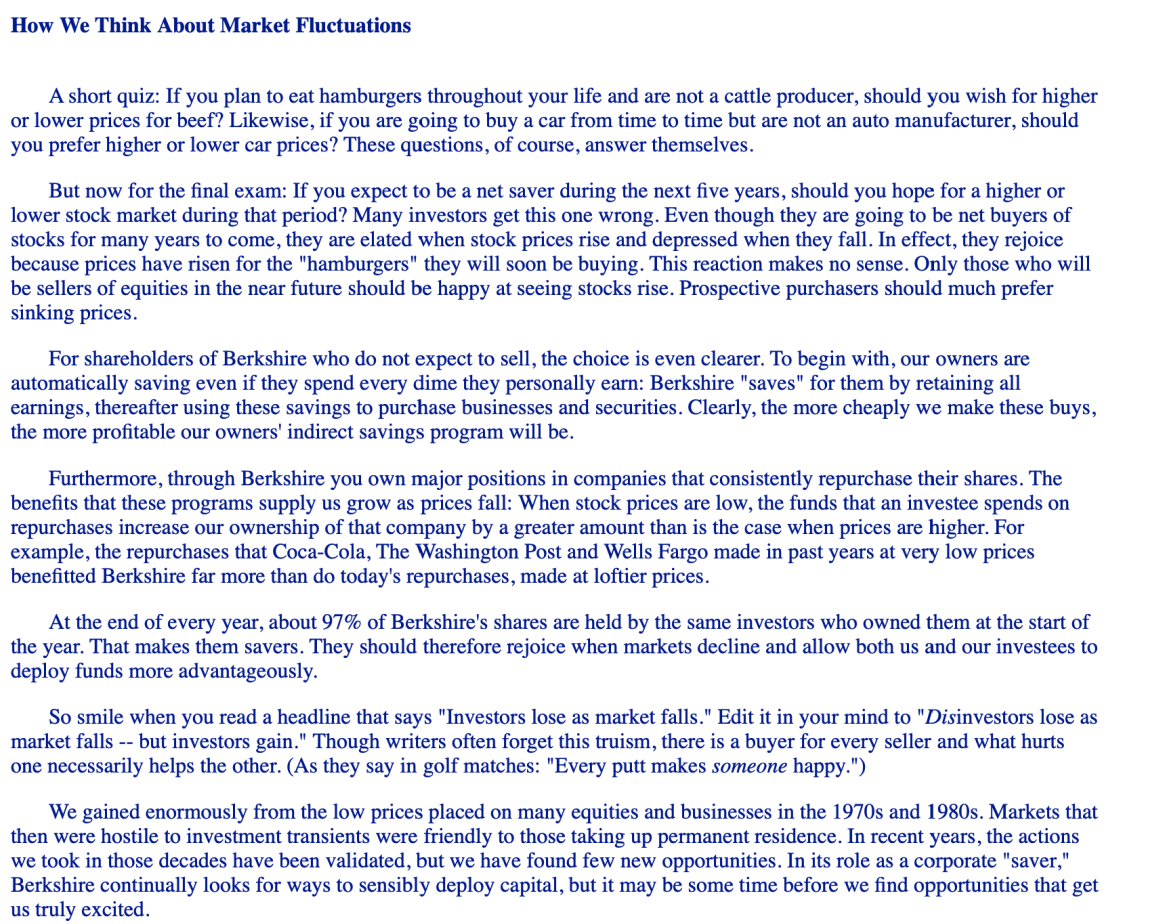

As an example: I’m currently reviewing the 1997 shareholder letter, and Buffett has this elegant description of how to think about market declines, which is obviously relevant to today’s environment.

The Value of Falling Stock Prices

I recently shared this paragraph here:

To summarize what Buffett is saying: as consumers, we would always rather see lower prices of things we regularly buy, from hamburgers to gasoline. But when it comes to stocks, we feel better when stocks are rising, not falling. But rising prices are counterproductive if we are planning to be net buyers of stocks.

What is so interesting about Buffett’s idea here is that it makes so much sense, yet very few people feel this way. Rooting for lower stock prices when you own stocks creates significant mental tension. But, if you make more money than you spend and thus have excess capital to invest, you are a net buyer of stocks. And that means — at least during those years when you are working and your earnings exceed your spending — you benefit from and should root for lower stock prices.

Note: Some will point out that this concept is oversimplified because there is a reflexivity component to stock prices (higher stock prices lead to people “feeling richer”, which drives real spending and thus real growth in earnings; in other words, stock prices can influence real fundamentals). But the reason it is so hard for us to internalize this concept is not because we are aware of the reflexivity aspect. It’s much less rational than that — most of us are happier when our stocks are rising and upset when they are falling. This emotion has nothing to do with fundamentals; it’s just human nature.

So Buffett’s point: if you are planning to buy stocks for a while, you should prefer lower stock prices, regardless of the size of your existing stock holdings.

I wanted to also add two more points:

Buybacks

Not only do we want lower prices if we are net buyers of stock; but if our companies are net buyers of their own stocks (as many of our holdings are), we should want lower stock prices simply because that means our companies are creating more value when their stock prices are low.

NVR, Inc. (NYSE:NVR) has retired 78% of its shares over the past 3 decades. AutoZone, Inc. (NYSE:AZO) has reduced its shares by a similar amount in the past 2 decades. NVR, AZO and every other company that produces excess free cash flow — i.e. they spend less than they earn and thus are corporate net savers — they benefit if their share price goes lower. Their free cash flow will buy more shares as the stock price falls.

The great thing about owning a portfolio of companies that earn excess free cash flow that is used to buy back shares is that you benefit from lower share prices even if you are fully invested. Even if you’re not adding to your account, the companies are adding for you. You’re acquiring a greater percentage ownership of your portfolio holdings when your companies are buying back shares, and this value creation increases when the market value of your portfolio declines.

Taking Market Share

The final way we benefit from lower stock prices is when we own companies that are taking market share. Floor & Decor Holdings Inc (NYSE:FND) is a company that in my view has a very strong moat in the retail hard surface flooring industry. The company has been taking market share since its founding two decades ago. While home improvement is a cyclical industry and Floor and Decor’s own business volumes will be impacted during the next housing downturn, it will also have the opportunity (and in my view, likelihood) of taking significant market share as the majority of the market is small mom-and-pop local flooring shops, many of which will struggle to survive the next downturn. Floor and Decor offers a far better value proposition for customers: lower prices, far greater in-stock selection, which is much more convenient for professional installers whose time is money — they need inventory in stock to be able to complete jobs and get paid.

The unfortunate reality for many local distributors is they can’t compete with this value proposition (as the husband of an interior designer who cannot locate in-stock inventory, I can attest firsthand to the huge advantage that Floor and Decor provides and the market share that it is taking). Floor and Decor will see slower growth during a downturn, but it will emerge in a much stronger position when the dust settles. If you are a long term owner of these types of companies that can expand their market share, you shouldn’t be concerned with where the share price goes next year. Sometimes a lower share price and a tough environment in the near term leads to greater market share and more future earning power (and thus a higher stock price) in the long term.

So the takeaways from the 1997 letter:

- If you’re a net buyer of hamburgers, you want a lower price of burgers. If you’re a net buyer of gas, you want lower gas prices. If you’re a net buyer of stocks, you should want lower stock prices. It really is that simple, and the fact that this mindset is so foreign to most investors is what gives those with the right mindset a big advantage, similar to the time arbitrage concept.

- Companies that are buying back shares are the corporate equivalent of net savers. They earn more than they spend and thus benefit from a lower stock price as each dollar spent on buybacks acquires more value with a lower share price, benefiting the long-term owners of the company

- To the extent that lower stock prices coincide with difficult economic conditions, the best companies often benefit indirectly from lower share prices as they are able to take market share, thus improving the long-term earning power of the company (and ultimately the long-term share price)

So shareholders benefit from lower prices in three ways (two directly and one indirectly): the simple fact is that when you’re buying something, you should prefer a lower price. This directly applies to individuals or companies buying shares of stock. And companies indirectly benefit through improving their long-term position through market share gains.

Disclosure: John Huber and clients of Saber Capital own shares of NVR and FND.

About John Huber

John Huber is the founder of Saber Capital Management, LLC. Saber is the general partner and manager of an investment fund modeled after the original Buffett partnerships. Saber’s strategy is to make very carefully selected investments in undervalued stocks of great businesses.

John can be reached at john@sabercapitalmgt.com.

Updated on

Sign up for ValueWalk’s free newsletter here.