{kind=link}

Courtesy of Nicholas Colas of DataTrek Research

The first job I had after graduating business school in 1991 was covering the US auto industry at the old First Boston, now Credit Suisse. This was just after the 1990 recession, and the Big Three were all on the ropes. Light vehicle demand was off +30 percent from its 1980s highs. The Japanese makers were all gaining share. Chrysler was essentially bankrupt, as were some of its major suppliers. Investors had left auto stocks for dead.

Fast forward a year, and US automaker/supplier stocks were market leadership. Chrysler had doubled, albeit from $5/share to $10. Vehicle demand was starting to recover. Incremental margins on new vehicles – minivans and SUVS – were fantastic. Every quarter saw these companies beat estimates, often by a wide margin. The lesson here is that recessions, while painful, offer investors tremendous money-making opportunities.

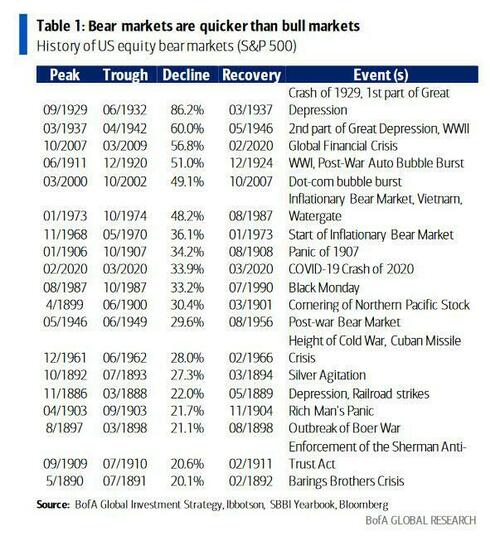

In fact, every recession and market crisis since 1973 tells the same story about US stocks generally, not just grimy cyclical names:

- 1973 – 1974: S&P 500 loses 37 percent

- 1975 – 1976: Index gains 70 percent

- 1981: S&P loses only 5 percent despite deep, Fed-induced recession

- 1982 – 1983: Index gains 48 percent

- 1990: S&P loses only 3 percent despite Gulf War I oil shock

- 1991 – 1992: Index gains 40 percent

- 2000 – 2002: S&P loses 37 percent

- 2003 – 2004: Index gains 42 percent

- 2008: S&P loses 37 percent

- 2009 – 2010: Index gains 45 percent

On its face, this pattern makes no sense. Why should investors so dramatically reset their expectations for future cash flows just because of a recession? Granted, bull markets always see some speculative excess. Stock prices going into recessionary bear markets are always too high simply because of that. But recessions are not exactly a surprise. Their timing is uncertain, of course. But everyone knows they occur, and that the economy eventually recovers, and US corporate earnings go on to make new highs.

The standard explanation is that markets cannot be sure of where earnings bottom or how long it will take for them to fully recover. Fair enough, as this data of S&P 500 earnings shows:

1990 Recession:

-

4-quarter trailing S&P operating earnings peaked in Q2 1989 at $25.53/share.

-

Trough earnings were $19.30/share (-24 pct from peak) in Q4 1990, 6 quarters after their prior peak.

-

S&P earnings finally made new highs in Q4 1993, 4 ½ years after their last peak, at $26.90/share.

2000 – 2002 (Recession, Dot Com Bubble Burst, 9-11 Attacks)

-

S&P earnings peaked in Q3 2000 at $56.79/share.

-

Trough earnings occurred 5 quarters later, in Q4 2001 at $38.85/share (-32 percent from peak).

-

It took 3 ½ years for earnings to make a new high, in Q1 2004, at $58.08/share.

2008 (Great Recession)

-

S&P earnings peaked in Q2 2007 at $91.47/share.

-

Trough earnings were $39.61/share (-57 percent from peak) in Q3 2009, 9 quarters after the prior peak.

-

It took 4 ¼ years for earnings to make fresh highs, at $94.64/share in Q3 2011.

On average, therefore, it takes 3-4 years for S&P 500 earnings power to recover fully after a recession and in the interim aggregate EPS can drop by anywhere from 24 – 57 percent. The latter is a huge range and merits some further explanation:

-

Every company has a different incremental margin – the profit it generates from its most recent dollar of revenue.

-

When revenues are increasing, as during an economic expansion, incremental margins are higher than base margins. When revenues are decreasing, as during a recession, incremental margins are lower (often dramatically so) than base margins.

-

The severity of an economic contraction determines how bad incremental margins eventually become.

Analysts call this operating leverage, and I can tell you from decades of experience that it is ferociously hard to calculate through a recession and into a recovery. Here’s why:

-

At the start of an economic downturn, incremental margins are very low or even negative. That is because companies tend to add to their cost structures at the top of a cycle. When the downturn comes, fixed costs are too high relative to declining demand.

-

As the downturn drags on, companies cut costs to align their operating model to lower demand. As economic conditions improve, marginal revenues come through at higher levels of profitability.

Pulling this discussion into the present day, all we know for sure is that equity markets don’t believe S&P 500 earnings will grow over the near term from their recent run rate of $54/share ($216/year). With the index’s close of 3,667 today, we are trading at 17.0x current earnings. That’s a fair multiple, spot on the 10-year average. This implies the market believes incremental revenues and margins (operating leverage) net to zero percent growth over the next year.

The history of earnings during recessions can give us a sense of where US large caps might bottom. Here are 3 scenarios, each using the same 18x multiple, not the 17x long-run average, for trough earnings since markets will assume strong incremental earnings leverage off the bottom for the reasons described earlier.

-

Modest earnings decline (15 percent): $184/share (down from $216/share currently)

-

S&P: 3,312

-

Earnings go back to 2018 – 2019 levels: $162/share, -25 percent

-

S&P: 2,916

-

Typical recessionary earnings decline (28 percent, average of 1990 and 2000 – 2002); $155/share

-

S&P: 2,790

These levels are not supposed to scare you; I mean them as a reason for hope. As profoundly difficult as the current investment environment is, it will end. Yes, inflation is a problem and yes, Fed policy is aggressive as a result. Stocks are bearing the brunt of the uncertainties those issues create.

A recession is likely; stock market volatility is very clear on that point, as were Fed Chair Powell’s comments yesterday. Companies will cut costs. Incremental margins will be awful for a quarter or two, but then improve dramatically. S&P earnings will recover and reach new highs in a few years’ time. This is how the pattern has worked across my +30-year career and I see no reason to think it will be different in the next cycle.

Takeaway: traders have a saying that sounds a bit wishy-washy but actually has some wisdom to it – “It’s too late to sell and too early to buy”. There will be some great returns once stocks settle out. The job now is to wait for the right valuations and catalysts to catch that move.