Courtesy of ZeroHedge

One year ago in keeping with its annual tradition, Goldman’s economics team published a list of 10 questions and answers for 2022 and while the end results was a mixed bag (professional subs can read the 2022 predictions and their outcome here), where Goldman was catastrophically wrong was in the only item that matters: inflation. Specifically, when asking if core PCE will fall below 3%, Goldman’s rhetorical answer was “yes” and boy was it wrong. And if you got inflation wrong, nothing else mattered (just look at the $20 trillion loss in global market cap as a result of unprecedented central bank tightening).

Of course, being wrong never stopped Goldman before, and earlier this week the bank’s chief economist Jan Hatzius published his list of most pressing questions for 2023, including a discussion on the bank’s most “out of consensus” forecast for the coming year, namely that the US will avoid a recession and will “continue progressing toward a soft landing.” Well, if nothing else, it appears that Goldman wants to extend the tradition of being right about the irrelevant stuff while being dead wrong about what truly matters.

Before we get into the weeds, here is a summary of Goldman’s broader economic outlook as laid out by Hatzius

Our most out-of-consensus forecast for 2023 is our call that the US will avoid an recession and instead continue progressing toward a soft landing. This forecast partly reflects our view that a period of below-potential growth is enough to gradually rebalance the labor market and dampen wage and price pressures. But it also reflects our analysis that indicates that the drag from fiscal and monetary policy tightening will diminish sharply next year, in contrast to the consensus view that the lagged effects of interest rate hikes will cause a recession in 2023.

We see the first steps in the rebalancing process this year as quite successful. Our jobs-workers gap has shrunk quickly at little cost, with all of the decline in labor demand coming from a drop in job openings. But there is much further to go in 2023. We expect the jobs-workers gap to narrow steadily next year due mainly to a further drop in job openings, but also to a limited increase in the unemployment rate to just over 4%. Both labor market rebalancing and a more moderate inflation environment should lower wage growth toward a more sustainable rate.

Supply chain recovery and the deflationary impulse in the goods sector that it promised to bring took much longer than we expected but have finally arrived. We expect this ongoing process to push core goods inflation negative next year, driving most of the decline in overall core inflation. This should help to push elevated short-term inflation expectations back toward normal levels.

We expect the FOMC to deliver 25bp rate hikes in February, March, and May, and then to hold the funds rate at 5-5.25% for the rest of 2023. We are skeptical that the FOMC will cut the funds rate until the economy is threatening to enter recession, and we do not expect this to happen next year.

The debt limit likely poses the greatest political risk next year, and we expect it to rival the 2011 episode in its disruption to financial markets and the economy. That said, we do not expect Congress to enact major fiscal changes. Republicans might press for spending cuts in a debt limit deal, but we do not expect substantial cuts next year. The White House might press for increased fiscal support, but this also looks unlikely as we believe a soft landing is more likely and a divided Congress would have difficulty responding to a recession even if one occurs.

Incidentally, while Goldman may be wrong about everything else, we agree that a divided Congress will be unable to respond to a recession (which will occur), which means that the only support possible in 2023 and 2024 will be from the Fed, and yes: the firehose is coming.

Without further ado, here is a look at the top 10 questions (and forecasts) from Goldman’s econ team:

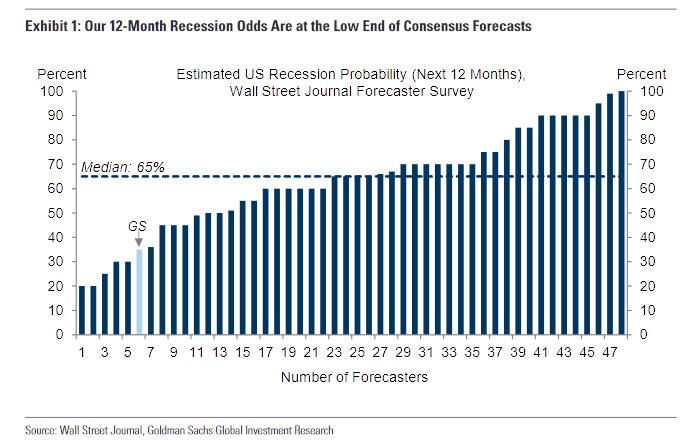

1. Will the US economy enter recession in 2023?

No. The consensus 12-month recession probability stands at 65%, well above our own 35% probability.

Part of our disagreement with consensus arises from our more optimistic view on whether a recession is necessary to tame inflation. We have argued this year that an extended period of below-potential growth can gradually rebalance supply and demand in the labor market and dampen wage and price pressures with a much more limited increase in the unemployment rate than historical relationships would suggest. We see this adjustment process as having gone quite well so far, though there is much further to go in 2023. We agree both that calibrating policy just right to stay on this low-growth path is difficult and that there is still uncertainty about how sticky inflation will prove to be, and for that reason our 12-month recession probability is about double to triple the unconditional historical average.

If views on what it will take to reduce inflation were the sole source of disagreement, then we would expect the consensus Fed forecast to be more hawkish than our own. Instead, both the consensus Fed view and market pricing are a touch more dovish than our forecast of a 5-5.25% terminal rate. This implies that much of the disagreement arises instead from differing views on near-term growth momentum and especially on the lagged impact of the rate hikes already delivered on the economy.

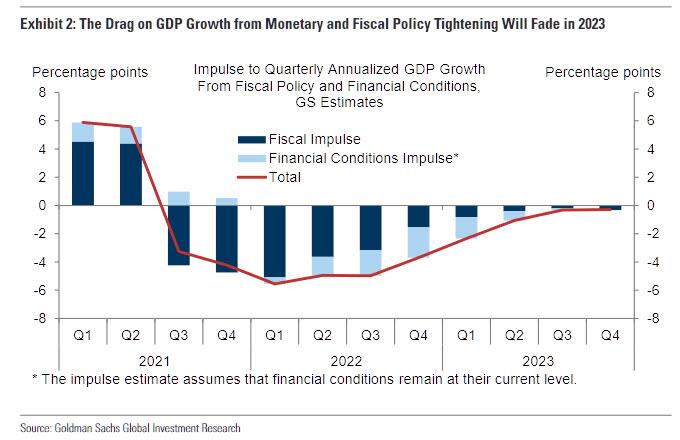

We expect more resilience in underlying demand next year than consensus because our analysis indicates that policy restraint has played a very large role in slowing demand growth this year but will fade quickly next year. Exhibit 2 shows that the combined drag from fiscal policy tightening and from monetary policy tightening via financial conditions has been very substantial but will diminish in 2023.

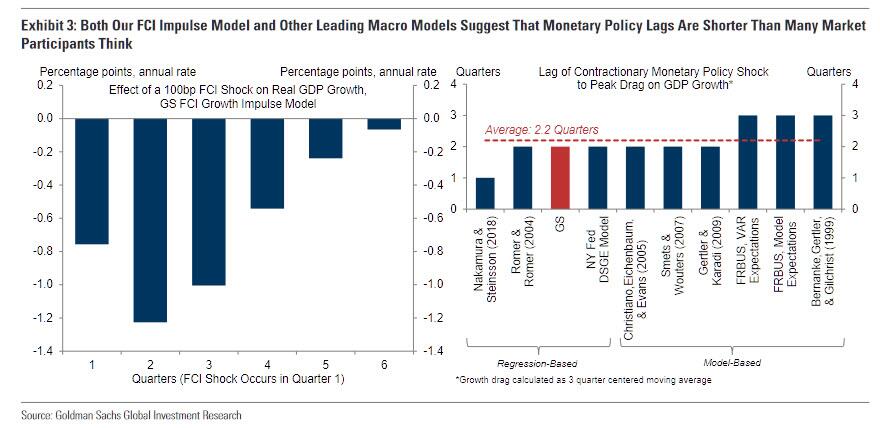

In contrast, the consensus forecast reflects a view that the “long and variable lags” of monetary policy will push the economy into recession next year. We recently showed that other macro models support the conclusion of our financial conditions index growth impulse model that the peak impact of rate hikes on GDP growth is front-loaded, as shown in Exhibit 3.

Much of the disagreement between our view and the implicit consensus view likely arises from two sources. First, our approach recognizes that rate hikes affect the economy via broad financial conditions as soon as markets anticipate them, which in 2022 was well before they were delivered. Second, some forecasters seem to confuse lags from monetary policy to GDP growth with lags to GDP levels—in fact, Milton Friedman’s famous assessment that policy acts with long and variable lags clearly referred to the time until the peak impact on the level of GDP.

2. Will consumer spending grow at least 1%?

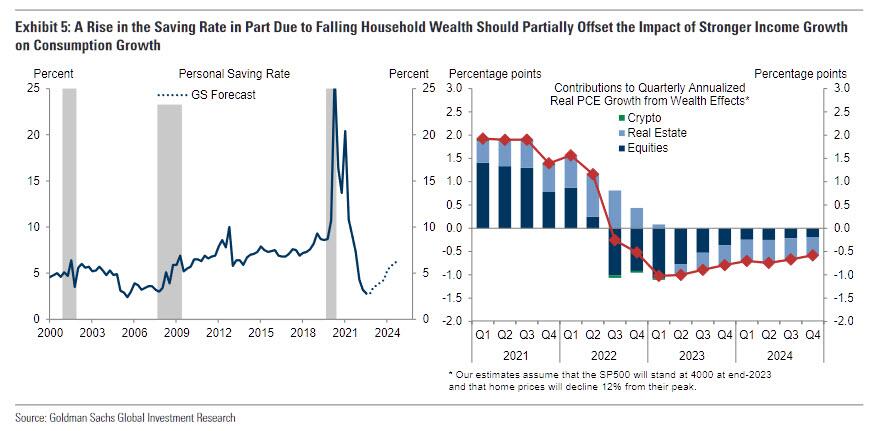

Yes. Real disposable income fell from the spring of 2021 through the summer of 2022 as inflation outran wage growth and special transfer payments included in pandemic relief packages expired. Exhibit 4 shows that we expect real income to rise 3.5% in the year ahead, supported by positive real wage growth, large cost-of-living adjustments on transfer payments including Social Security and food stamps, a jump in interest income, and a decline in the effective tax rate as a spike driven by capital gains and bracket creep reverses. While gains from interest income and tax rate normalization will accrue mostly to high-income households and have less impact on spending, the turnaround in real income is nonetheless a key reason that we have a relatively optimistic 2023 consumer outlook.

The impact of firmer real income growth on consumption should be partially offset by a rise in the saving rate next year. We expect the saving rate to increase in part because higher interest rates have reduced household wealth by lowering home and equity prices, and in part because the lower- and middle-income families that tapped excess savings to support their spending this year as transfer payments expired will have less to draw on next year. One important form that drawing on excess savings has taken is the rebound in consumer credit use, and while it remains below its pre-pandemic level as a share of income, its recent rapid growth rate is not sustainable and will have to slow next year.

We expect these forces to net out to consumption growth of roughly 1.5% in 2023.

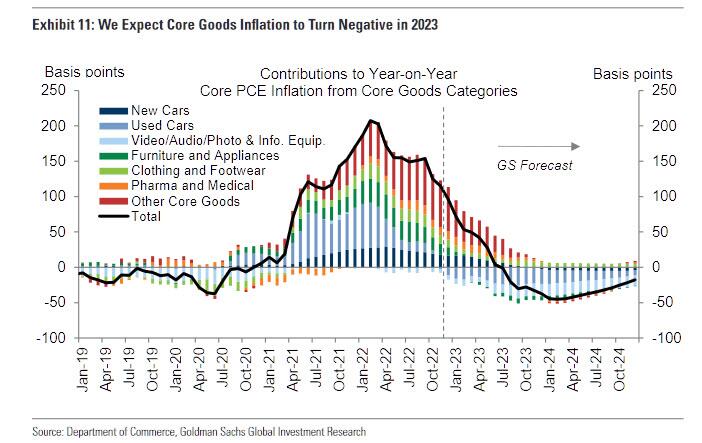

3. Will core goods inflation turn negative year-over-year?

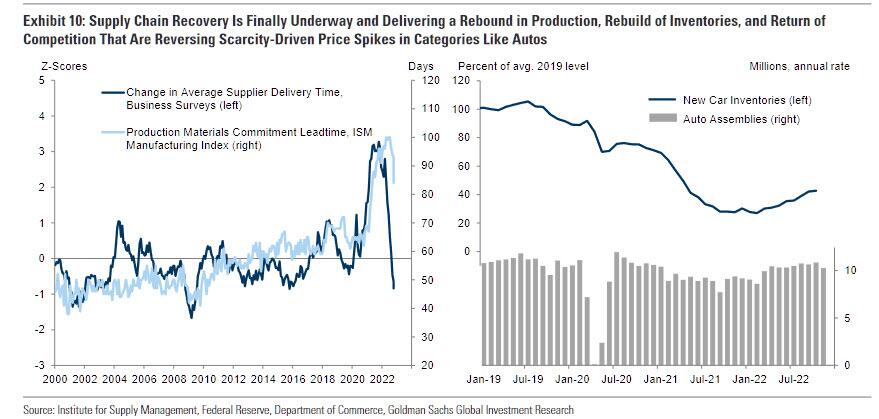

Yes. One of our largest forecast misses in both 2021 and 2022 arose from mistiming the supply chain recovery, which was delayed by further global shocks and in turn delayed the disinflationary impulse from the goods sector that we had expected to push core inflation meaningfully lower this year. But now supply chain recovery finally appears to be underway, lowering costs and enabling production of scarce items like autos to recover, as Exhibit 9 shows. As inventories are rebuilt, competition should reverse the scarcity effects that raised retail margins and consumer prices earlier in the pandemic.

More moderate commodity price inflation, falling transportation costs, and downward pressure on import prices from past dollar appreciation should also help to reduce core PCE goods inflation, which has already fallen from a peak of 7.6% year-on-year to 3.8% in November and should turn negative next year. Core goods inflation ran modestly negative last cycle, and we expect it to run somewhat more negative than usual for a while as elevated prices of items like used cars revert to more normal levels.

We expect a more limited decline on the services side, with core services PCE falling from 5% to a still high 4.5% by December 2023, in part due to lags in the official data for the two largest categories, shelter and health care. However, Chair Powell’s recent focus on the sharp decline in alternative measures of rent inflation that will lead the official data by longer than usual suggests that Fed officials are comfortable looking ahead to an eventual deceleration and will not overreact to the lagged official data next year.

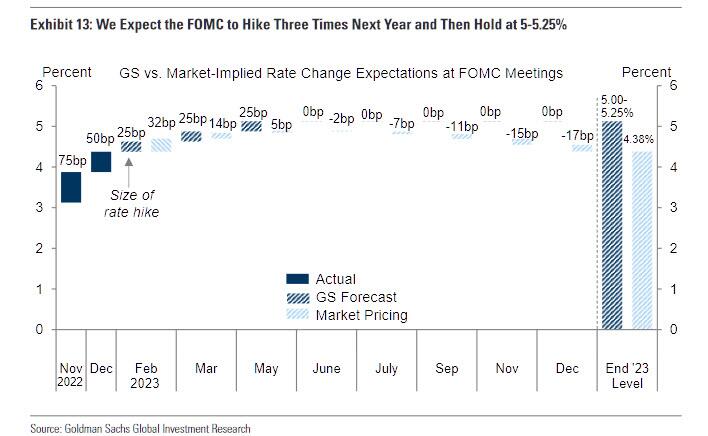

4. Will the Fed cut the funds rate?

No. We expect the FOMC to deliver three 25bp rate hikes in February, March, and May, and then to hold the funds rate at 5-5.25% for the rest of 2023. In contrast, market pricing implies a peak funds rate of 4.75-5% and declines to about 4.4% by the end of 2023, as shown in Exhibit 13.

There are two possible rationales for cutting the funds rate in the future. The first rationale would be that if inflation declines, Fed officials might decide that policy does not need to be as restrictive anymore. We are doubtful that the goods-driven decline in inflation that we expect in 2023 would be sufficient to give the FOMC confidence that inflation is moving down in a sustained way, which Powell has said is the criterion for cutting. But more than that, we remain skeptical that the FOMC will cut just for the sake of returning to neutral because we suspect that the Fed leadership does not have enough confidence in its neutral rate estimate for it to exert much gravitational pull on the policy rate.

The second and we think more likely rationale for cutting at some point would be that the economy is entering recession or threatens to do so without an easing in monetary policy. We see this as the more natural path—if tighter monetary policy succeeds in convincingly reducing inflation, we expect the FOMC to just leave the policy rate unchanged until something goes wrong. We have cuts in our forecast over 2024-2026, but we do not intend for the timing to be taken literally and instead think of our path of cuts as a placeholder for an uncertain future date when something goes wrong.

We often caution that market pricing is a probability-weighted average of many scenarios and is not directly comparable to our modal forecast of the Fed path, which assumes that the economy will avoid recession next year. We suspect that the downward slope in the yield curve in 2023 mostly reflects some probability of cuts in a possible recession scenario, while the downward slope in 2024 likely reflects both some probability of cuts in a recession and some probability of cuts if inflation moderates without a recession. Our own probability-weighted average forecast of possible Fed paths also implies that the yield curve should slope downward but is somewhat more hawkish than market pricing.

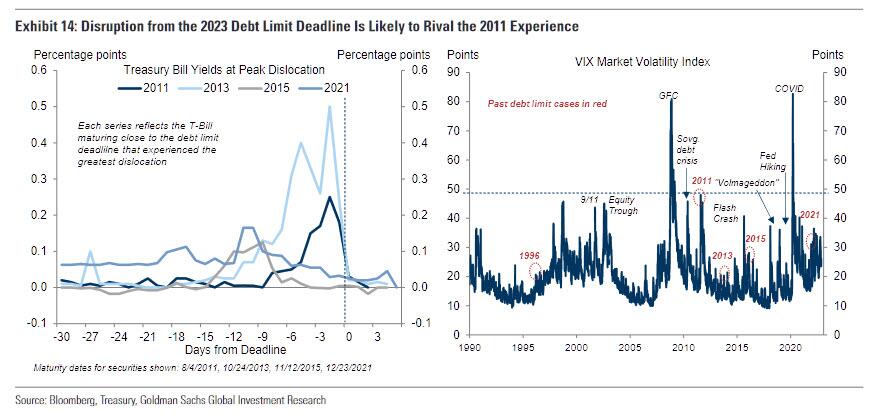

5. Will the debt limit have as negative an impact on financial markets in 2023 as it in 2011?

Yes. The political and fiscal conditions next year will be similar to the last two extremely disruptive debt limit increases, in 1995 and 2011. Like next year, in those periods a Democratic President in his third year faced a Republican House after losing the majority in the midterm election. Those episodes also followed a run-up in public debt as a share of GDP and/or a rise in federal interest expense, similar to the experience over the last few years. However, midterm gains of 54 seats in 1994 and 63 in 2010 gave Republicans a clearer political mandate and the votes to carry it out, at least in the House. By contrast, Republicans netted only 9 seats in the 2022 midterms and enter 2023 with a very thin House majority. Public focus on the public debt is also much lower compared to those prior periods, and Republicans have not emphasized fiscal restraint nearly as much recently as they had in the mid-1990s or early part of the Obama Administration.

Prior disruptive debt limit standoffs led to increased market volatility and a sell-off in Treasury securities maturing around the debt limit deadline, and we would expect this to occur next year. In 2023, we would expect yields on bills maturing around the deadline to rise by at least as much as they did in 2011 and 2013, and for volatility in financial markets to rise similar to those periods (Exhibit 14).

There is also a real chance that Congress fails to raise the debt limit in time next year, forcing Treasury to reduce daily payments to the level of receipts (i.e., immediately eliminating the budget deficit), resulting in a spending cut of around 10% of GDP at an annualized rate. While we think it is more likely that Congress manages to avoid this and raise the debt limit before it constrains Treasury’s ability to pay its obligations, the risk appears higher than at any point since 2011.

The deadline for Congress to raise the debt limit before Treasury must cut back net borrowing will likely be sometime in August but could be as late as October depending on Treasury cash flows (Exhibit 15). An early signal of the risk the debt limit poses will come at the start of 2023, when the new House of Representatives is seated. If Republicans reinstate the “motion to vacate” that allows any member of the House to call for a vote for a new speaker of the House—several Republican House members have recently called for this in return for their vote for speaker—it could be difficult for the next speaker to put a clean debt limit increase to a vote until forced by financial markets.

{kind=link}

Quickly running through the other five questions (and answers) we have the following:

- Will the jobs-workers gap fall below 3 million? – Yes

- Will the job openings rate fall from its peak by more than the unemployment rate rises from its trough? – Yes

- Will wage growth slow at least 1pp? – Yes

- Will one-year Michigan consumer inflation expectations fall below 4%? – Yes

- Will Congress enact substantial fiscal policy changes in 2023? – No.

For more detailed on these, and other questions and predictions, read the full note available to pro subs.