{kind=link}

Courtesy of ZeroHedge

The S&P 500, the world’s biggest and most liquid equity index influences the sentiment or price of most global assets. However, as discussed here repeatedly over the past few years, its performance has been skewed by mega-cap growth stocks, i.e., the Generals. Of course, in 2022, they had a very tough time. Tesla (-65.0%), Meta (-64.2%), Amazon (-49.6%), Alphabet (-39.1%), Microsoft (-28.0%), and Apple (-26.4%) all underperformed to sometimes dramatic effect. And given these 6 names alone still comprise around 19% (down from 26% this time last year) of the world’s most important stock index, DB’s Jim Reid notes that even macro-only investors need to pay attention.

Of this list, Tesla has been the most volatile this year falling 12.2% on the first day but having two +5% plus days, including yesterday. It’s -2.8% so far in 2023.

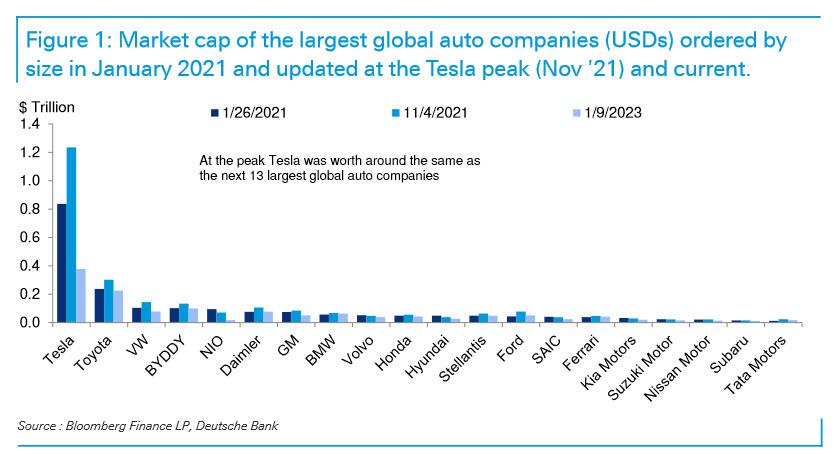

Which brings us to today’s Chart of the Day from Jim Reid, which updates a graph from his “bubble chart book” in January 2021. Back then, he showed that Tesla’s market cap was around as big as the next largest 8 global auto companies. That was obviously a premature concern as at the peak in November 2021 (market cap $1.24tn), it was then worth around the same amount as the next 13 largest – an incredible stat.

Fast forward to today and it’s now back down to being worth a bit more than just the next two largest ($378bn market cap).

While Reid admits that he not is a single-name stock analyst, he says it’s interesting to debate what valuation such a disruptor should have relative to the competition: “After all, non-fossil fuel cars will continue to dominate the roads for some years, but most car companies will also compete for the spoils in the electric market. It is true that Tesla bulls have pointed out for some years that disruptors such as Apple and Amazon have maintained a dominant position in their respective sectors. But it’s not clear if the sectors/products are comparable. The bulls might also point to Tesla still having increased by 5 times since the March 2020 Covid lows. So, the starting point is important.”

In any event, at the peak, we were still in a world of zero yields and expected to stay there in perpetuity by many. As such, companies with an expected high earnings stream in the future were given very high multiples. This wasn’t the fault of those companies impacted.

So for macro, Reid says that “it is interesting to debate how much of the recent fall in such stocks is down to the interest rate environment changing, and how much was a fundamental overvaluation story.” That matters if the interest rate environment changes again (not if but when) and as such is important for macro.