Holy cow!

Holy cow!

NVIDAI (NVDA) just saved the Nasdaq all by itself by reporting $2.1Bn in earnings for their quarter, which ended on April 30th but that was actually 20% LOWER than last year – it was, however a 15% beat of expectations. What really got the stock going was the revenue guidance, which was raised from $7.18Bn in Q2 to $11Bn – a 53% increase thanks to non-stop demand for NVDA’s very expensive AI chips, which are currently being scalped on the market for double their usual cost.

“Demand [related to generative AI and large language models] has extended our data center visibility out a few quarters and we have procured substantially higher supply for the second half of the year,” Nvidia (NASDAQ:NVDA) executives said on an earnings call.

This is nothing we didn’t know already but the market reaction is surprising as you would have thought the good news was priced in as NVDA is already up 200% from the October lows. This morning’s gains will make NVDA “worth” more than META or TSLA (for the moment). And, of course, MRVL, AMD, AI, PLTR and SYNA are all popping as well – as are MSFT and GOOGL – anyone who said the word “AI” in a conference call is up this morning.

Perhaps NVDA will end up making $20Bn this year instead of the $11Bn they were projecting. Does that really justify putting them in the $1Tn club at 50x best-case earnings? They had the right chip at the right time but so have Intel (INTC) and AMD at other times. Chips are a very cyclical sector and I an never one for chasing them.

However, INTC was going to be our Stock of the Year for 2024 if it was sill below $30 in November and it’s more like $28 this morning as they do NOT have the right chips at this time – but what better time to buy them than when they are down? $28.25 is $115Bn in market cap and INTC will be lucky to make $1.6Bn this year as it is still an investment year but that cycle ends next year, when they expect to make $7Bn – which would be 16.4x.

We were hoping to catch it closer to $25 but now I’m worried they will say “AI” and pop to $35 so, for now, let’s add INTC to our Portfolios as such:

In the Income Portfolio, let’s:

-

- Sell 5 INTC Dec 2025 $30 puts for $5.80 ($2,700)

- Buy 15 INTC Dec 2025 $30 calls for $6.50 ($9,750)

- Sell 10 INTC Dec 2025 $40 calls for $3.60 ($3,600)

- Sell 5 INTC Sept $30 calls for $2 ($1,000)

That’s net $2,450 on the $15,000 spread so we have $12,550 (512%) upside potential at $40 and we’ve used 113 of 939 days we have to sell so maybe 8 sales left can generate another $8,000 and bring our upside potential over $20,000 and, more importantly, generate about 40% per quarter in INCOME – which is the point of this portfolio!

![]() The net Portfolio Margin of 5 short Dec 2025 $30 INTC puts is just $955 – so it’s a very margin-efficient trade but we do have the potential of having $15,000 worth of INTC stock assigned to us so we will set aside 1/2 of an allocation block – which are $30,000 each in our $150,000 portfolio.

The net Portfolio Margin of 5 short Dec 2025 $30 INTC puts is just $955 – so it’s a very margin-efficient trade but we do have the potential of having $15,000 worth of INTC stock assigned to us so we will set aside 1/2 of an allocation block – which are $30,000 each in our $150,000 portfolio.

In the Long-Term Portfolio (LTP), which has $500,000, we will be more aggressive with:

-

- Sell 10 INTC Dec 2025 $35 puts at $9 ($9,000)

- Buy 30 INTC Jan 2025 $25 calls at $7.50 ($22,500)

- Sell 20 INTC Dec 2025 $30 calls for $6.50 ($13,000)

- Sell 10 INTC Sept $30 calls for $2 ($2,000)

Notice we bought the Jan 2025 $25 calls instead of the $9 Dec 2025 $25 calls but that’s because we can always spend $1.50 to roll them but, for now, we have a net credit of $1,500 on the $30,000 spread so $31,500 (2,100%) upside potential plus a solid $10,000 of potential short-call sales as well. The more aggressive puts require $2,349.03 in net margin and the LTP has 20 $50,000 allocation blocks and we’ll assign a full block to this one as we HOPE INTC goes lower and we can double down.

We also have a golden opportunity to fill out the missing parts of Tuesday’s SQQQ hedge, which will well-cover both portfolios potential long ownership of Intel – what a great morning – thank you NVDA shoppers!

Meanwhile, Fitch has warned that the United State’s AAA credit-rating on NEGATIVE WATCH as debt ceiling talks continue to go nowhere. Fitch said that a missed payment after June 1 would likely be “inconsistent” with a triple-A rating. The ratings firm also said that potential workarounds—such as invoking the 14th amendment to ignore the debt limit—would undermine U.S. creditworthiness. S&P downgraded the U.S. credit rating after a similar standoff over the debt limit in 2011 and has never raised it back.

Losing an AAA credit rating for the U.S. would have a negative impact on the National Debt and interest payments. It would likely increase the borrowing costs for the Government, as well as for companies and consumers that rely on Treasury securities as a benchmark for interest rates. Higher rates would also increase the Government’s debt service burden, which is already 12% of its $4.66Bn in Revenues at $594B.

According to S&P, a one-notch downgrade of the U.S. credit rating could raise interest rates by 0.25 percentage points and increase annual interest payments on $32Tn in debt by $80 billion – that is the cost of the GOP temper-tantrum!

As the Democrats have been saying for 50 years (since Nixon!), the problem with deficits are not about Discretionary Spending, which is only 38% of the non-Military budget – it’s about LACK OF TAXATION as the Government only collects $2.6Tn of Income Taxes and $1.5Tn of Payroll Taxes and $445Bn in Corporate Taxes. That’s $4.5Bn against a $6.1Bn budget so we’re $1.6Tn short – very simple…

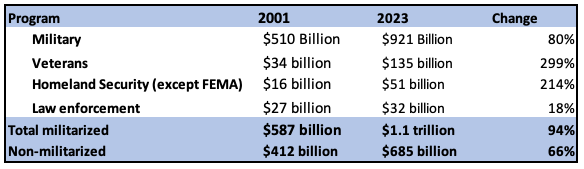

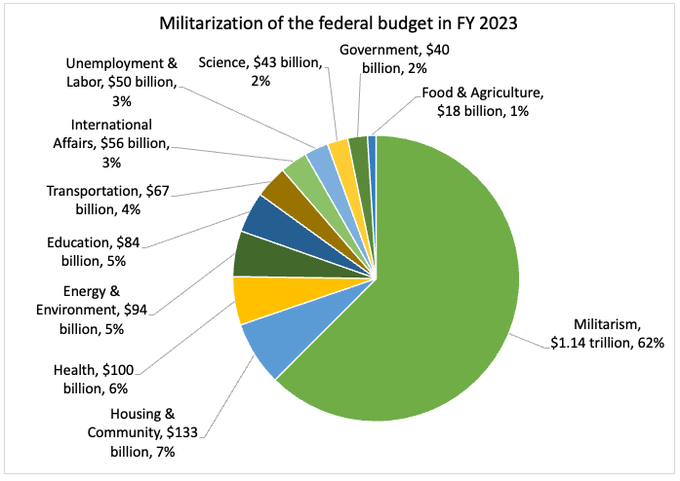

Part of that, of course, is the GOP/Trump-approved 2023 Defense Sector Budget of $1.8Tn and that’s up $800Bn since the 2001 budget (see chart above). As with all these “must have” Defense increases, they never come along with any way to pay for them – just more and more debt and now, when we hit the debt ceiling – cutting it back is off the table and, instead, we’re supposed to steal more money from Social Security and Medicare (which the recipients worked their whole lives saving for and is supposedly ENTRUSTED to the Government – not gifted to it!) or cutting the Health Budget (we saw how well that worked out leading up to Covid) or Housing or Feeding our Citizens.

Part of that, of course, is the GOP/Trump-approved 2023 Defense Sector Budget of $1.8Tn and that’s up $800Bn since the 2001 budget (see chart above). As with all these “must have” Defense increases, they never come along with any way to pay for them – just more and more debt and now, when we hit the debt ceiling – cutting it back is off the table and, instead, we’re supposed to steal more money from Social Security and Medicare (which the recipients worked their whole lives saving for and is supposedly ENTRUSTED to the Government – not gifted to it!) or cutting the Health Budget (we saw how well that worked out leading up to Covid) or Housing or Feeding our Citizens.

The ENTIRE US non-Defense Discretionary Budget of $800Bn is LESS than the INCREASE in the Defense budget over the past 20 years!

That’s from 2021! Perhaps if we spent less, other countries would not feel pressured to spend as much. Remember how Trump was beating up on NATO to spend more? That’s because we were looking more and more like idiots by comparison.

Just like this country spends 2-3 times more on Healthcare than other counties (yet we have the worst outcomes), the US spends 4-5 times more on Defense per capita as well. Perhaps, like Russia, our outcomes would be poor as well if they are ever tested. As I noted about politicians having to wear patches from their sponsors yesterday – a good portion of those patches would be from Defense Contractors.

So Defense spending is out of control but even more out of control is how little we tax Corporations. $445Bn is not even 10% of Corporate Profits (and that’s AFTER massive deductions, depreciations, loopholes, etc.) and it’s not even 10% of total tax collections and it’s only 1.7% of our $25Tn GDP.

So Defense spending is out of control but even more out of control is how little we tax Corporations. $445Bn is not even 10% of Corporate Profits (and that’s AFTER massive deductions, depreciations, loopholes, etc.) and it’s not even 10% of total tax collections and it’s only 1.7% of our $25Tn GDP.

The GOP solution is not to raise Corporate Taxes but to cut Social Security and Medicare, which contribute 7% of the GDP – about 4x more than Corporations do. That massive 5.3% gap, which has been pretty consistent since Reagan jacked up the Military and slashed Corporate Taxes, if you multiply it by a cumulative $415Tn of GDP (1982-2022), it comes to $22Tn of underpaid Corporate Taxes. That plus the interest on the unpaid amount is our ENTIRE National Debt!

THAT is what is wrong with our country and it’s very easy to fix by simply making companies pay their fair share of income taxes. Will that ever happen? No it won’t so enjoy it while you can – the debt collectors are knocking on the door while Congress pretends we can fix this by squeezing more money out of the bottom 90%.

AI Overlords can’t take this mess over fast enough in my opinion!

{kind=link}