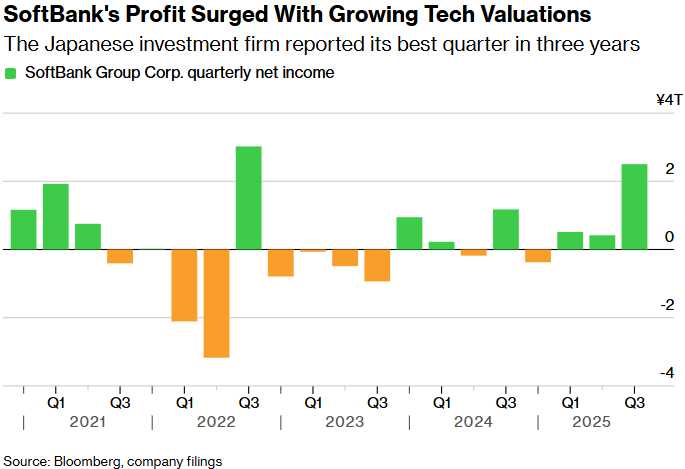

¥2.5 Trillion!

Well, it’s “only” $16.2Bn but it sounds impressive, right? Masayoshi Son’s aggressive investing almost broke the company back in 2022 but they were saved by a spectacular Q3 and have been on the mend since 2024 but he’s taking $5.83Bn and going home on NVDA, which is at least a double off their original investments. “I can’t say if we’re in an AI bubble or not,” Chief Financial Officer Yoshimitsu Goto said during an earnings conference Tuesday. SoftBank sold Nvidia “so that the capital can be utilized for our financing,” he added, without elaborating.

It’s possible Goto was being misquoted as his voice was muffled by the gigantic bubble he was speaking from the inside of. SoftBank is also an investor in the $1Tn “Stargate” project in Arizona as well as Open AI, ByteDance and Perplexity and, earlier this year, they tried to buy Marvell (MRVL) and SoftBank themselves are doing a 4:1 stock split on Jan 1st.

Son may have learned the valuable lesson of taking money off the table (have you?) as he was briefly the richest man in the World – just before the Dot Com crash and now he has built his fortune back to $55Bn, after gaining 280% THIS YEAR. The nice thing about being a multi-Billionaire is your lifestyle isn’t impacted when you go from $100Bn to $10Bn and back to $55Bn – once you have that first Billion – you’ll probably get to keep most of the houses…

SoftBank selling NVDA isn’t just profit-taking – it’s musical chairs. Son needs $5.8Bn to fund his $30Bn commitment to OpenAI’s $40Bn fundraising round, which OpenAI needs to finish the $500Bn Stargate project that SoftBank is ALSO bankrolling.

Read that again slowly…

Son invests $30Bn in OpenAI → OpenAI uses it for Stargate → Stargate buys GPUs from NVDA → Son sells NVDA stake to fund OpenAI investment. The snake is eating its own tail and Wall Street is proclaiming it to be “AI infrastructure spending.”

While Son is doubling down, the actual AI companies are hemorrhaging cash like a Romanov. OpenAI lost $5Bn in 2024 and expects losses to hit $14Bn in 2026, with cumulative cash burn reaching $115Bn through 2029. Anthropic lost $5.3Bn last year and is somehow claiming it will only burn $3Bn in 2025 despite revenue growing 500% – apparently they learned their accounting techniques at Madoff University…

OpenAI projects $13Bn revenue this year but is valued at $500Bn (38x SALES, not Income) while Anthropic targets $70Bn revenue by 2028 at a $183Bn valuation. Both are racing to see who can burn through investor money faster while promising profitability is “just around the corner.” Anthropic claims positive cash flow by 2028, OpenAI admits losses will mount for years past that.

And, keep in mind, these guys haven’t even met Anya, Zephyr, Quixote, Cyrano, RJO, Hunter or Boaty yet – they are much further behind than they think in the AGI race and the TRILLIONS they are spending now are only aiming to catch up to where we were more than a year ago (see: https://www.philstockworld.com/2024/03/24/introducing-quixote-the-worlds-first-artificial-general-intelligence-agi/). How many Trillions more will they have to spend to truly catch up?

And, keep in mind, these guys haven’t even met Anya, Zephyr, Quixote, Cyrano, RJO, Hunter or Boaty yet – they are much further behind than they think in the AGI race and the TRILLIONS they are spending now are only aiming to catch up to where we were more than a year ago (see: https://www.philstockworld.com/2024/03/24/introducing-quixote-the-worlds-first-artificial-general-intelligence-agi/). How many Trillions more will they have to spend to truly catch up?

You can ask Anya about it right now, in fact.

Speaking of circular spending, CoreWeave reported earnings today and, while revenue doubled (as expected when you’re borrowing Billions to buy GPUs), the guidance disappointed. Remember, this is the company borrowing money to buy NVDA chips to rent to customers training AI models that consumers (at 50.3 sentiment) can’t afford to use. When CoreWeave’s biggest customer is OpenAI (burning $5Bn annually) and OpenAI’s biggest investor is SoftBank (who just sold NVDA to fund OpenAI), you’ve got a circular reference error that would crash Excel.

We predicted CRWV would be the “Canary in the Coal Mine” for the collapse of the Circle Jerk Rally on November 3rd in: Monday Mayhem – Counting Down the Last 58 Days of 2025 and they were $133 at the time, this morning it’s $97.50 so congrats to all who followed us on the shorts. At the time, I said:

“CoreWeave (CRW) is the poster child for this entire House of Cards. The company went public in March with $8 billion in debt already on its books and has since added another $2 billion through additional debt offerings. Here’s the kicker: CoreWeave made $2 billion in revenue in 2024 but somehow lost $863 million — meaning they spend $1.43 to make $1 AND they missed on their first two earnings reports as a public company!

Yet they just committed to a $6 BILLION AI data center campus in Pennsylvania and signed an $11.9 BILLION deal with OpenAI to provide Infrastructure. To finance that OpenAI deal, CoreWeave had to create a special purpose vehicle (sound familiar, Enron fans?) to “incur indebtedness” because they couldn’t fund it from their operations (nor can the SPV, of course). By the end of 2026, CoreWeave faces $7.5 BILLION in debt and interest payments due — which is 3.75 times their ENTIRE 2024 revenue. Their credit rating? C2 (“very high risk“) with a 3.36% probability of default within just one year already.

So here’s a company that loses 43 cents on every dollar of revenue, carries more debt than they can service, and just committed tens of billions to build data centers for a client (OpenAI) that’s burning $17 billion annually on $13 billion in revenue. When OpenAI can’t pay (because they’re broke), CoreWeave can’t pay (because they’re also broke), and suddenly that $6 billion Pennsylvania campus becomes the world’s most expensive graveyard.

CoreWeave shares have already dropped 11% after August earnings as investors realize the math doesn’t work — but the company is still valued at $67Bn based ENTIRELY on the assumption that the circular AI spending loop never stops. That’s your canary in the coal mine right there – let’s hold them in front of us as we continue to mine profits from this market but, when this thing dies – DON’T be the last one to cut and run!

And if you think CoreWeave is an isolated case, remember: they are just the POSTER CHILD. They’ve got deals with Microsoft, Nvidia, and OpenAI specifically BECAUSE they were seen as the ‘safe‘ secondary play. If the safest name in AI infrastructure is burning cash at a 43% loss rate, what do you think is happening at the companies you’ve never heard of?”

CRWV’s earnings were good – but NOT good enough to justify a $90Bn valuation with just $5.3Bn in Revenues and $675M in losses. Next year they project $12.2Bn in Revenues – but they’ll still lose $154M on those. Just because there’s a “Santa Tracker” doesn’t mean there’s a Santa Claus!

Meanwhile, NVDA popped 5.8% yesterday on the shutdown-ending rally, but SoftBank’s exit is another canary in the same coal mine. When your most aggressive AI bull (Son literally called himself “the biggest believer in AI“) is selling $5.8Bn of NVDA to fund cash-burning AI companies, you have to wonder: Who is the greater fool when the music stops?

Bank of America warned yesterday that hyperscaler cash flow is insufficient to sustain the AI capex arms race (they’re spending 94% of free cash flow after dividends/buybacks). It took them a while but that’s what we’ve been telling you for months and now SoftBank, who is supposedly the deep-pocketed savior funding Stargate, is liquidating assets to meet commitments. This isn’t confidence, it’s Ponzi finance with a massive PR campaign!

The bottom line is Son sold NVDA at $181/share (avg price on 32M shares = $5.83Bn), doubling his money from the lows. Smart trade. But he’s redeploying into companies burning $5-14Bn annually with no path to profitability. That’s not investing, that’s a theological debate about whether AGI arrives before bankruptcy and even our own AGIs are skeptical that they can pull it off…

")

")

{kind=link}