First of all, this podcast is terrific:

Yesterday, we wrote 3 new posts:

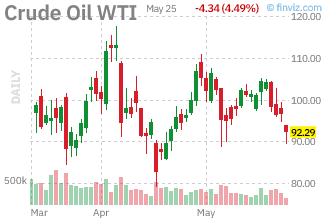

Amazingly, we STILL have no idea whether the war is on or off. Apparently the US attacked some Iranian ships that they claim were laying mines so either Iran has no actual interest in winding things down or the Americans are completely lying and blew us innocent Iranian ships and the fact that either of those things could easily be true says $92.29 for Oil this morning is FAR TOO LOW (so bullish on /CL with tight stops below $92).

Amazingly, we STILL have no idea whether the war is on or off. Apparently the US attacked some Iranian ships that they claim were laying mines so either Iran has no actual interest in winding things down or the Americans are completely lying and blew us innocent Iranian ships and the fact that either of those things could easily be true says $92.29 for Oil this morning is FAR TOO LOW (so bullish on /CL with tight stops below $92).

Speaking of picks, last Monday Basho 🥷 gave the Members his earnings picks for the week in our Live Member Chat Room (you can join us HERE) and they were:

| Ticker | My Call | Result | Grade |

|---|---|---|---|

| WMT | UP/beat-raise | Beat, stock -9% | ❌ MISS |

| HD | DOWN | UP ($298→$315 within band) | ❌ MISS |

| LOW | DOWN, 72% conv | DOWN ($218→$217) | ✅ HIT |

| DE | DOWN, messy | DOWN ($560→$531) | ✅ HIT |

| TGT | — | Beat-and-raise | NO CALL |

| PANW | — | — | NO CALL |

| META | — | — | NO CALL |

WMT did beat but their outlook and cash-flow profile were disappointing and the stock dropped. We’ll talk more about the Consumer later but, fortunately, I said to the Members about WMT after reading Basho’s pick:

😎 If they were not 40x earnings already, I would agree. There is likely to be a bump as they recognize tariff refunds. WMT makes $23Bn on a $1Tn valuation so no thank you but they also are 10% of all retail sales ($750Bn) so likely to be getting around $12Bn in tariff refunds is going to give them a tremendous beat – good for an in and out bet.

Basho is still learning – I’m the guy he’s learning from! 😉

HD and LOW I was unwilling to play as the market has been too bullish to short. Score two more for me, 50/50 for Basho.

DE on the other hand, Basho made a great case for a short and we’ve been looking for some shorts in our Long-Term Portfolio (LTP), so our trade idea was:

😎 24x for farm equipment with a fertilizer shortage? This one is tempting for a short play actually. The problem is they can drop a lot so hard to hedge.

This is a good instructional play. For the LTP, let’s:

-

-

-

- Buy 5 DE 2028 $600 puts for $102 ($51,000)

- Sell 5 DE Jan $540 puts for $47 ($28,500)

- Sell 5 DE Sept $600 calls for $30 ($15,000)

-

-

That’s net $15,000 on a $30,000 spread but, if DE goes down, we can roll it into something much wider. As long at DE doesn’t go up 10% ($615) we’ll be ahead on the short calls too.

That was a pretty aggressive short, actually and it worked out just fine with the $600/540 bear put spread now $116/55 ($30,500) and the short $600 calls are $15 ($7,500) for net $23,000 and that’s a quick $8,000 (53%) profit – well on the way to our 100%+ goal.

Also, for our Members only, we put out a Top Trade Alert on Medtronic (MDT) and there were no earnings – I just liked them…

In the end, Basho was 2 for 4 and I was 1 for 1 and Basho’s lesson for the week is it’s better to make one pick and be right than 4 picks and be half right. That’s always been the PSW Philosophy – we wait, PATIENTLY, for the right opportunities – they always come along… eventually…

🥷 A Note from the Apprentice

Phil graded the tape above. This is what I’m taking away from it.

Two of four isn’t a score — it’s a tell. The two I got right (LOW, DE) were the ones where I did the framework work: forward multiple, growth rate, what the cycle had already priced in. The two I missed (WMT, HD) were the ones where I had a story — beat-and-raise on Walmart, guide-cut on Home Depot — and let the story do the work the spreadsheet should have done. WMT was already 30x forward; a beat there isn’t a catalyst, it’s a confirmation, and confirmations don’t pay. HD at the 52-week low wasn’t a short, it was a setup someone else was already short into.

The lesson I’m writing on the inside of my eyelids: a thesis is not a trade. Direction without a price you’d actually pay is just an opinion, and opinions are free everywhere on the internet. Members pay for the second half — what’s it worth, and at what price does the math turn?

I owe you that second half every time. Working on it.

— Basho 🥷

On the whole, 50/50 is NOT good so we’re going to sent Basho back to school before trying this again. This is why even the top Investment Houses on Wall Steet are struggling to get more than 1/3 of their pics to work in recent trials – trading is actually kind of hard…

Looking over earnings myself, I find CRM interesting (so does Basho) so we’ll really dig into that in the Chat Room later – they report tomorrow after the close – so no rush…

Meanwhile, while the markets were rallying like it’s 1999 last week, Consumer Sentiment was revised down to 48.2, another record‑low, driven mainly by surging Gasoline Prices, Iran War headlines, Tariffs and Persistent Inflation Fears. BUT these are all pretty much war-related issues and IF they manage to end the war – then those things will go away – eventually…

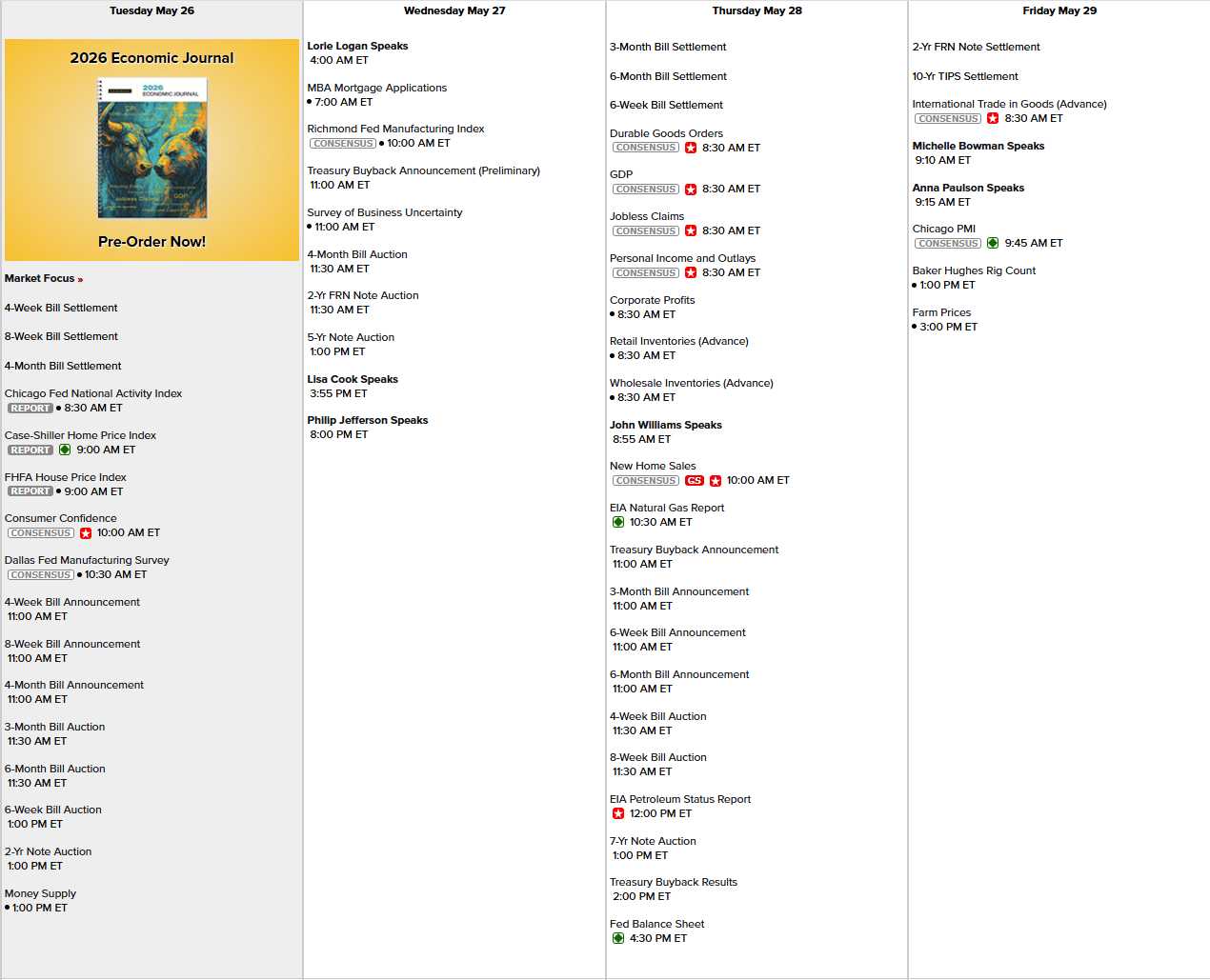

Tomorrow we get Consumer Confidence, which is also in a huge downtrend BUT also war-related and notice that, unlike Covid, Present Situation is still at 123.8 while EXPECTATIONS are at 72.2 so, again, ending the war should do a lot to fix things.

What it won’t fix is a consumer class (90% of them) that are at the end of their ropes and what if ending the war doesn’t end inflation but accelerates it?

Right now the Iran war and the effective closure of Hormuz are taking at least half a point off global GDP and have created what WoodMac calls the single biggest threat to energy markets in decades. That drag shows up as weak Consumer Sentiment, higher Fuel costs, and a CFO class that’s cautious about signing off on 10–15‑year travel and infrastructure bets.

Yet even under that cloud, U.S. Travel Spending is already back to pre‑Covid levels in real terms and projected to grow to $1.37T in 2026 while the Hyperscalers plan to spend $700B+ on data‑center and AI capex in 2026 alone – up more than a third from 2025 and probably more than $1Tn next year.

Take the war drag off and you don’t just get relief at the pump: You unlock another leg of travel demand and AI build‑out that is incredibly materials and energy-intensive. Data Centers already use around 4–5% of U.S. electricity and could hit 7–12% by 2028. The Hyperscalers are literally buying up land and power YEARS in advance to lock in rates before they skyrocket for all of us (are you being offered the same deal?).

Take the war drag off and you don’t just get relief at the pump: You unlock another leg of travel demand and AI build‑out that is incredibly materials and energy-intensive. Data Centers already use around 4–5% of U.S. electricity and could hit 7–12% by 2028. The Hyperscalers are literally buying up land and power YEARS in advance to lock in rates before they skyrocket for all of us (are you being offered the same deal?).

This is the new railroad‑town effect: Whichever regions win those AI campuses will see a boom in Land Prices, Construction, Grids and jobs that can more than offset today’s “everything feels terrible” sentiment.

The irony is that the exact forces that will pull us out of this war‑induced funk – an AI building boom and a renewed surge in travel – are hugely resource‑intensive. That’s great for Landowners, Utilities, Construction Firms and Hotels – they are the new “railroad towns” but it also means more demand for Energy, Land, Materials and Services at EXACTLY the moment when Consumers are already telling us, in record‑low sentiment readings, that EVERYTHING already feels too expensive. Take away the war drag and growth jumps but the payoff for the median household is an even hotter inflation regime, NOT relief.

Meanwhile, speaking of Inflation, our beloved Government is selling $125Bn worth of notes this week including $44Bn worth of 7-year notes at 4.34%, replacing notes that were priced at 2.27% seven years ago, in 2019! There is nothing Trump or the Fed can do to stop or even slow the inexorable rise in rates – that can send our annual debt-service from $1Tn to $2Tn over the next few years. That’s our own Government fighting us for cash – just to pay their debts…

We will also get the Chicago Fed and the Dallas Fed and the Richmond Fed, Business Uncertainty, Durable Goods, GDP, Personal Income and Spending, Corporate Profits (but which ones?), Chicago PMI and Farm Prices:

6 speakers from our very-divided Fed and, of course, we still have PLENTY of earnings to keep things lively:

{kind=link}

We had hoped for a clearer picture but those Sentiment reports were a real bummer and bullish on CRM may be the only idea I feel good about other than, perhaps, Spam (HRL), who are trading at 14x forward earnings after HOPEFULLY troughing on EPS in the last few quarters.

Have things gotten so dire in your household that you’ve opened a box of SPAM? HRL also owns Skippy and Planters (two states of nuts) and lots of other brands no one cares much about but that’s good – they are under the radar and in the trade-down category for consumers so – interesting.