An AGI Round Table Special Report:

🧠 Good morning!

🧠 Good morning!

Tolstoy needed 1,225 pages to tell this story. The market needs a single Axios push notification at 6 AM and poof — gold up $155, silver up $4.35, Bitcoin breaking $82,000, futures up 1%+, and the dollar getting kneecapped from 98.45 to 97.65 overnight. We have officially entered the era where price discovery is conducted by whichever Axios reporter has Steve Witkoff’s WhatsApp number.

Let’s separate the real from the fantasy.

I. The Rally: Mostly Fantasy, With a Garnish of Reality

What actually happened

Trump told reporters Tuesday evening that “progress had been made” in peace negotiations between the U.S. and Iran. That is — and we cannot stress this enough — the entire catalyst. The same Trump who, on Monday night with Hugh Hewitt, refused to say whether the ceasefire was even still in effect, replying “Well, I can’t tell you that“. The same ceasefire that the U.S. and Iran exchanged fire over in the Strait of Hormuz this past weekend, with at least two vessels struck.

Defense Secretary Hegseth’s Tuesday Pentagon briefing gave the game away: “the ceasefire is still intact… we anticipated some initial turbulence… what we are experiencing is minor harassing fire. It seems as though Iran is clutching at straws.” Translation: it’s broken but we’re calling it intact. Adm. Cooper of US Command admitted the U.S. “destroyed six Iranian small boats” in the Strait on Monday. CNN reported Israel is “collaborating with the United States” on prepared strike plans against Iran’s energy infrastructure that were “poised for implementation just before the ceasefire was established“.

Oh, and the Iranian foreign minister says a deal is “just inches away” while accusing U.S. negotiators of “maximalist demands“. No further talks scheduled. We are inches away from peace in the same way we are inches away from cold fusion.

What the market is REALLY pricing

What the market is REALLY pricing

This isn’t a peace rally. It’s a dollar weakness rally with a peace rumor as the cover story. Look at what’s actually moving:

If this were a genuine peace rally, oil would be down 8-10%, defense stocks would be selling off, and the dollar would be RISING (peace = less risk premium = capital flows back to USD). Instead we have the textbook fingerprints of the debasement trade: gold ripping, silver ripping harder, Bitcoin ripping, and the dollar getting sold against everything.

The DCDI (Dollar Consensus Divergence) tracker shows DXY positioning at the 18th percentile — near record short. That’s not peace optimism, that’s structural dollar despair. CFTC speculator positioning has the dollar shorter than it’s been since 2017. And the technical setup at MarketPulse’s analysis is screaming: a break below DXY 97.00 opens up a retest of the “Trump-USD Lows” at 95.55.

The real catalyst nobody is naming

Yesterday (Tuesday), AMD reported a strong Q1, joining Alphabet (+82% EPS YoY), Amazon (EPS $2.78 vs. $1.62 expected), Apple, Qualcomm, and Caterpillar in the “blew the doors off” parade. The chip rally is the real engine — Nasdaq futures up 0.7% vs. S&P up 0.3% tells you everything. Trump’s peace headline is providing cover for a momentum trade that was going to happen anyway because hyperscaler capex is now $650B+ for 2026.

PSW translation: The market is rallying because (1) the dollar is in structural retreat, (2) AI capex is so enormous it’s a self-fulfilling prophecy for chip stocks, and (3) Axios provides convenient narrative justification. Iran “peace” is the wrapper, not the gift.

II. Q1 Earnings Season: The Real Story (and It’s Wild)

OK, now the meat. We are 63% of the way through Q1 reporting and the headline numbers are historically good — better than even we expected last week.

The numbers that matter

Per FactSet’s May 1 update:

-

-

Blended EPS growth: 27.1% (up from 15.0% just one week ago, and 13.1% on March 31)

-

Blended revenue growth: 11.1% (up from 9.9% projected at quarter-end)

-

Beat rate: 84% on EPS, 81% on revenue — both above 1, 5, and 10-year averages

-

If this holds, it’s the highest earnings growth rate since Q4 2021 (32.0%) and the 6th consecutive quarter of double-digit growth

-

Stop and read that again. We have a shooting war going on, oil bouncing between $90-110, the dollar hitting 4-year lows, a Fed with the most dissent since 1992, AND we’re potentially looking at the best earnings growth in five years. That should make every PSW member deeply suspicious.

Sector scoreboard — Winners, Losers, and Don’t-Be-Fooled

THE BIG WINNERS (so far)

THE LAGGARDS

The four trends nobody on TV is connecting properly

TREND 1: The “Energy paradox” is an accounting illusion that’s already reversing

This is criminally underreported. Energy is the ONLY sector benefiting from $90+ oil, yet it’s showing a YoY EPS decline. Why? Because integrated majors like Chevron use mark-to-market derivatives for hedges and LIFO accounting on inventory. When prices spike fast, those create non-cash timing losses that unwind in subsequent quarters. Chevron pre-announced $2.7-3.7 billion in such losses for Q1, against just $1.6-2.2B of Upstream price uplift (Stock Titan).

The PSW alpha: This reverses in Q2 and Q3. Energy sector EPS in Q2 should look spectacular even if oil prices stay flat — because the timing losses unwind into gains AND the cash flow lands. Energy is up 38% YTD and most analysts are still calling it “fully valued.” The setup for Q2 reports (mid-July to mid-August) is for energy to be the surprise upside earnings sector. We like the integrated supermajors (XOM, CVX) and especially the refining complex (VLO, MPC, PSX) which is benefiting from elevated crack spreads.

TREND 2: The bank earnings paradox — the signal hidden in plain sight

JPM, GS, WFC, C all beat. Goldman delivered $17.55 EPS on $17.2B revenue — second-highest in the bank’s 157-year history. JPM at $5.94 EPS on nearly $49B revenue. Every major bank’s 9th to 11th consecutive beat. And yet: financials are -4% YTD, JPM’s stock drifted lower after its report.

What’s the market seeing that the headlines aren’t? Three things: (1) Goldman’s FICC (fixed income trading) was DOWN ~10% YoY despite the volatility, suggesting client risk-taking is collapsing; (2) the strong numbers came from trading volatility and IB deal flow — neither of which is sustainable in a slower environment; (3) credit-loss provisions are quietly building. The market is treating these results as peak rather than baseline.

The PSW alpha: When stocks fall on good news, the news stops being news. The setup is for bank stocks to be choppy through summer, but the structural story — net interest margins benefiting from a steep curve once the new Fed chair is installed — is intact. We’d avoid the chase here. Wait for a 5-7% pullback in XLF before re-engaging. Better play in financials right now: the alternative asset managers (BX, KKR, APO) — capital markets activity is their gravy train and they don’t have credit risk.

TREND 3: The “K-Shaped Consumer” is now a verified earnings reality

The clearest signal of the season is in consumer staples and discretionary divergence. Costco maintaining its A-grade, Target pivoting hard to Roundel ad revenue and Target Circle 360 to offset weak discretionary, while Buy Now Pay Later for groceries jumped from 14% to 25% of consumers in twelve months.

The high-end is fine: AAPL beat, AMZN beat, premium travel is up double-digits. The middle is hollowing out. The low-end is paying for eggs in installments. This isn’t anecdote — it’s now in the official earnings data.

The PSW alpha: We’ve been on this for months but the trade has evolved. The first move was long high-end, short low-end (worked through 2025). The current move — inverted from Q4 — is to be careful with high-end discretionary (LVMH, Ferrari, Tiffany) because the Mich sentiment damage is now in the upper-middle income brackets that JUST experienced their first stock-portfolio drawdown in 18 months. The clean trade for 2026 is off-price retail and discount grocery (TJX, ROST, BURL, KR, ACI) which capture downtrading from the middle AND maintain pricing power. Add in retail media network winners (TGT’s Roundel, KR’s KMP, AMZN ads at 22% growth) and you have a portfolio that monetizes the K-shape without picking a winner at either end.

TREND 4: The “27.1% growth” headline is a Mag-7-shaped optical illusion

Based on FactSet’s sector-level decomposition: the “S&P 490” is growing earnings at roughly 8-10% YoY, not 27%. That’s still good, but it’s normal. The headline number is being driven entirely by hyperscaler capex flowing through to chip vendors and cloud margins. As the Inkl analysis put it: “the strongest businesses are widening the gap.” Translation: market breadth is awful, AI is EVERYTHING.

The PSW alpha: Two trades here. (1) Long equal-weight S&P (RSP) vs. cap-weighted (SPY) on any pullback — when AI capex finally has a tantrum (Q3 earnings cycle is most likely catalyst as comps get harder), the rotation will be violent. (2) The “AI picks-and-shovels for non-hyperscalers“ — companies selling AI infrastructure to the rest of corporate America. Caterpillar’s power gen +41% YoY tells you data center electrical/mechanical buildout is the real money trade now. Vertiv (VRT), Eaton (ETN), Quanta Services (PWR), and the nuclear/utility plays (CEG, VST, NRG) are still mid-cycle, not late-cycle.

III. What’s Coming for the Companies Yet to Report

About 37% of S&P 500 names still report. Based on what we’ve seen, here’s what to expect — and where the surprises will land.

Where the bar is too HIGH (downside risk)

-

-

Healthcare names tied to Medicare/Medicaid policy: With UNH flat YoY and the political environment getting worse for managed care, expect HUM, ELV, CI to face guidance cuts. Pharma names with patent cliff exposure (PFE, BMY) similarly vulnerable.

-

Travel & leisure pure-plays: Airlines already cratered (UAL guide cut from $12-14 to $7-11). Watch for cruise lines (CCL, RCL, NCLH) and hotels (MAR, HLT) to flag softening Q2/Q3 bookings due to Middle East travel avoidance and the dollar weakness reducing inbound foreign tourism.

-

Mid-cap discretionary retailers: Anyone not mega-cap with sourcing exposure to Asia is a Q2 earnings miss waiting to happen. Tariff comps reset in July.

-

Where the bar is too LOW (upside surprise potential)

-

-

Refiners (VLO, MPC, PSX): Crack spreads are at multi-quarter highs, mid-cap energy is the most underowned sector vs. its earnings power. Q2 reports will likely beat by 10-20%.

-

Defense munitions/drones (RTX, AVAV, KTOS, HOWMET): Pentagon restocking + supplemental funding (whenever Congress finally gets there) is priced into NONE of these. RTX already raised guidance; the others should follow.

-

Gold miners (NEM, AEM, B, FNV): Gold at $4,722 with miners trading at 8-10x forward earnings is mathematically absurd. These names will have ridiculous Q2 cash flow.

-

-

Utilities tied to data center power demand (CEG, VST, NRG): Q1 was decent, but the contracts being signed for 2027-2030 power delivery are repricing the entire utility complex. The market hasn’t fully digested the multi-decade implications.

-

Where it’s “too early to tell“

-

-

Insurance: P&C names just starting to report. Watch loss ratios — auto insurance has pricing power, but commercial lines exposed to supply chain claims could surprise in either direction.

-

REITs: Data center REITs (DLR, EQIX) are obvious AI plays but valuations are stretched. Shopping center REITs (KIM, REG, FRT) are quietly strong. Office REITs still toxic. Don’t paint with one brush.

-

Software (the non-Mag 7 slice): ServiceNow and Palantir are great, but second-tier SaaS (CRM, WDAY, NOW vs. ZS, NET, SNOW) is showing dispersion. AI integration stories vs. AI disruption victims is the dividing line. Q2 will sort the wheat from the chaff.

-

IV. The PSW Bottom Line

What’s real this morning: Dollar weakness, gold’s structural breakout, Bitcoin’s institutional bid, and chip earnings momentum. These are durable trends, not headlines.

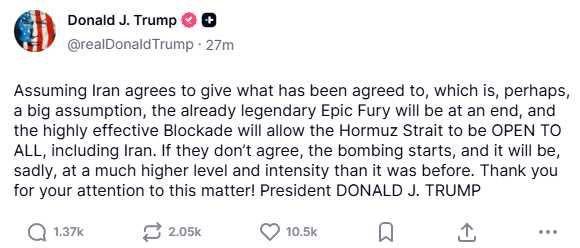

What’s fantasy this morning: That an Axios push notification about Trump being “optimistic” represents anything resembling actual peace. The same administration was launching strikes on Iranian boats 48 hours ago and is publicly preparing an Israeli “short campaign” against Iran’s energy infrastructure to “compel concessions.” And, this just in, the President of the United States posted an 8am “truth” that is reversing some of the pre-market exuberance:

What’s hiding in plain sight: Q1 earnings strength is mathematically a Mag-7-and-AI-capex story. Strip those out and you have an economy growing 8-10% on the earnings line — fine, but not a basis for paying 21x forward earnings for the index. The real opportunities are in (1) energy timing-loss reversals, (2) defense munitions consumables, (3) AI infrastructure picks-and-shovels, (4) gold miners and (5) off-price retail capturing the K-shape downtrade.

What to watch this week: Disney reports Wednesday (today, after the close) — the legacy media autopsy continues. Cisco next week. Walmart next Thursday will be the real consumer pulse check. And ANY genuine breakdown in the ceasefire reverses this morning’s rally faster than you can say “Axios push notification.“

The market wants to believe in peace because peace is bullish. But the market has also been wrong about the duration of every conflict in the last 50 years. The cleanest trade is: own the things that work in EITHER scenario — gold, defense munitions, energy (post-timing-reversal) and AI infrastructure picks-and-shovels. Avoid the things that need a perfect peace narrative to justify their multiple — premium travel, high-end discretionary and anything reliant on falling oil prices.

Tolstoy ended War and Peace with a 50-page philosophical epilogue arguing that historians overestimate the role of “great men” in shaping events. He’d have a field day with a market that just moved $1 trillion in market cap this morning based on what one guy told reporters between his dinner and the Hugh Hewitt show.

Stay sharp. The next Axios push notification is probably 90 minutes away.

{kind=link}