“Nothing really matters

“Nothing really matters

Anyone can see

Nothing really matters

Nothing really matters to me” – Queen

Yes, the war is STILL going.

It’s Day 93 and, once again, the peace treaty that was “hours away” on Friday is STILL not signed. The S&P 500, however, has completely lost its mind and hit all-time highs on Friday. As I had a nice, relaxing weekend and I’m not in the mood to write my 10th Monday article about how, despite Friday’s assurances, the war is still on and the Strait is still blocked – I’m going to turn this over to Basho, who LOVES talking about this stuff:

What Actually Happened Last Week (The Unvarnished Version)

-

-

-

- Monday-Wednesday: Negotiations in Doha. Both sides said “progress.” Neither side said what progress meant. Iran’s Foreign Ministry spokesman said progress had been made, then clarified Iran had made no nuclear commitments. The US said Iran agreed to the 60-day MoU framework. Iran said the US was characterizing things “incompletely.” We’ve been here before. Several times.

- Thursday: Vance told reporters the US and Iran were “very close.” Also said he couldn’t promise a deal would happen. That’s the diplomatic equivalent of “I’m almost certain I left my keys somewhere in this building.“

- Friday morning: Trump posts on Truth Social that he’s heading to the Situation Room to make a “final determination.” Markets immediately went to record highs. Oil dropped 1.6% to below $92 Brent. The S&P, Nasdaq, Dow and Russell 2000 all posted simultaneous all-time highs — the first time all four indexes hit records together since November. Dell surged 32% on AI earnings. The VIX collapsed to a 15 handle.

-

-

-

-

-

- Friday afternoon: Trump emerged from the Situation Room and… asked for a few more days to think about it.

-

-

The man spent hours in the Situation Room surrounded by generals, diplomats, and intelligence officials, and his decision was to schedule another meeting. This is the geopolitical equivalent of calling a plumber, having him look at the pipes for three hours, and then saying “let me think about it” while the toilet continues to overflow.

Over the weekend: Iran fired missiles. Not many — a “message” according to CNN’s June 1 report. CENTCOM called it a “minor provocation.” Iran called it a “reminder.” The Strait of Hormuz remained at approximately 5% of normal traffic. 840 tankers remain stranded inside the Gulf per Wikipedia’s Hormuz crisis page — 600 inside, 240 waiting outside. This number goes up every week, not down.

The Numbers That Should Be Terrifying Everyone (But Aren’t)

Oil: WTI at $90.47, up 3.99% this morning, per Trading Economics. Brent at $93.71. Down about 16% from the $110-115 peak — but still +45% from a year ago. The May monthly decline was the largest since April 2025 — entirely on deal hopes. That oil drop was the deal, in terms of market pricing. The actual deal is still unsigned. If the deal falls apart, oil has 15-20% of upside risk baked right back in.

The market’s logic, such as it is: The Nasdaq was up 10% in May alone. The S&P up 5%. All four major indexes at all-time highs simultaneously. The VIX at 15.76 — below its long-term average, suggesting less fear than normal despite an ongoing war. In the immortal tradition of financial markets, the market has decided that the war is basically over, approximately 93 days before the war is actually over.

What’s driving it beyond Iran optimism? AI. Specifically, Dell’s $60 billion AI server forecast. Palantir partnership. Anthropic valued at $965 billion, above OpenAI. The market has split into two parallel universes: in one, there’s a war that has disrupted global energy markets for three months and threatens to derail the global economy. In the other, AI is going to make everything worth 40% more regardless. Both universes are trading simultaneously on the same exchange.

The Actual Deal Framework (What’s In It, What Isn’t)

Per the NYT’s most detailed account, confirmed by multiple senior US officials and regional sources, here is what negotiators agreed to — pending Trump’s signature and Iran’s formal endorsement:

Phase 1 (First 30 days):

-

-

-

-

-

Iran opens Strait of Hormuz to unrestricted commercial traffic, removes mines

-

US lifts naval blockade of Iranian ports

-

Ceasefire extended 60 days

-

-

-

-

Phase 2 (Days 31-60):

-

-

-

-

-

Formal nuclear negotiations begin

-

Iran suspends uranium enrichment for a period “likely between 10-20 years” (still being negotiated Iran does not intend to give up their reactor program)

-

Iran disposes of highly enriched uranium (HEU) — method TBD (export to China/Russia/IAEA? US custody? Nobody has agreed)

-

US provides “gradual” sanctions relief — amount TBD, structured through Qatar to avoid Trump saying he gave Iran money – though Qatar already gave Trump a $400 million plane

-

-

-

-

What’s NOT in the MoU:

-

-

-

-

-

Iran’s missile program — not mentioned

-

Lebanon — Iran demands it’s included, US refuses

-

Long-term Hormuz sovereignty — deferred

-

The specific HEU disposal mechanism — the single biggest unresolved issue

-

Any guarantee Iran won’t restart enrichment in Year 21

-

-

-

-

The nuclear sleight of hand nobody’s talking about: The PBS NewsHour report noted that Iran making “no nuclear weapon” commitments is essentially what Iran agreed to in the 2015 JCPOA. The one Obama negotiated. The one Trump blew up in 2018. Which started the chain of events that led to this war. The deal that may emerge from 93 days of conflict and roughly 5,000+ deaths is… roughly similar to what existed in 2015, except with a bombed-out Iranian military, a closed Strait, 840 stranded tankers, $4 gas, and a Nasdaq at all-time highs because Dell sells AI servers.

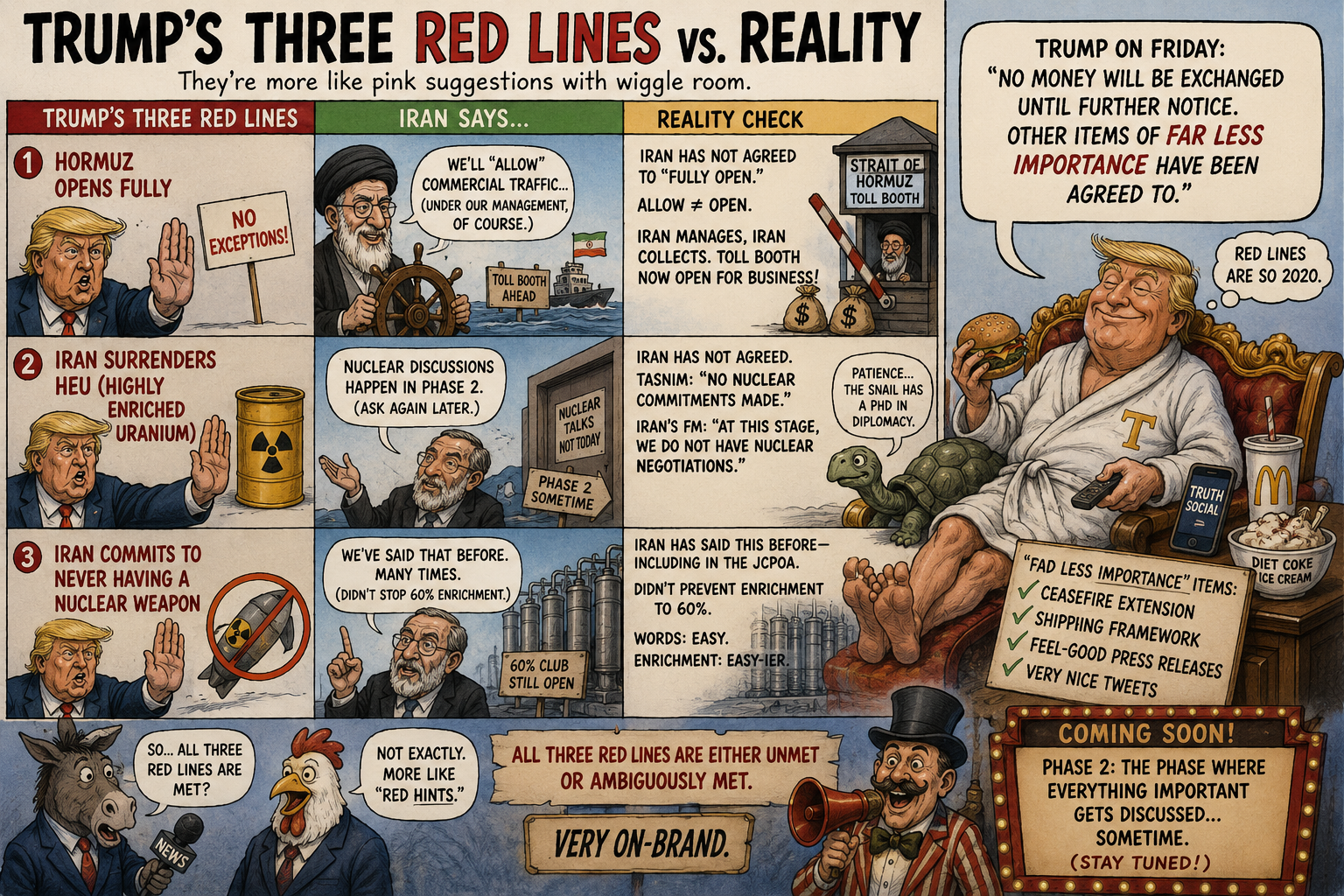

Trump’s Three Red Lines vs. Reality

Treasury Secretary Scott Bessent confirmed Friday that Trump’s three red lines remain:

-

-

-

-

Hormuz opens fully — Iran has NOT agreed to “fully open.” Iran has agreed to “allow” commercial traffic, while maintaining Iranian management authority. Those are different things. Rubio said last week Iran is building a “tolling system no country should accept.” That system has been operating for weeks.

-

Iran surrenders HEU — Iran has NOT agreed to this. Iran says nuclear discussions happen in Phase 2. The Tasnim Agency explicitly denied Iran made any nuclear commitments. Iran’s FM said “at this stage, we do not have nuclear negotiations.“

-

Iran commits to never having a nuclear weapon — Iran has said this before, including in the JCPOA. It did not prevent enrichment to 60%.

-

-

-

All three red lines are either unmet or ambiguously met. Trump’s own words on Friday: “No money will be exchanged until further notice. Other items of far less importance have been agreed to.” The “far less importance” items are apparently the ceasefire extension and shipping framework. The three things he actually said matter… haven’t been agreed to. This is very on-brand.

The Congress Problem Nobody’s Reporting Enough

Here’s the buried lede that deserves more attention: Friday was the 60th day since Trump formally notified Congress of military operations against Iran. US law requires Congressional approval within 60 days — otherwise hostilities must cease. Trump told Congress members Friday that the conflict had “terminated since a ceasefire was enacted on April 8.” He’s arguing the ongoing blockade is not “hostilities.”

Republican Senator Josh Hawley — not a liberal squish — publicly called for “redeploying forces away from the conflict” and demanded Congressional approval to continue. BBC confirmed that frustration is growing among Republican lawmakers over what they see as a costly war with unclear objectives and no Congressional authorization.

This is the war’s domestic political clock, and it’s ticking louder than the Situation Room meetings. Trump cannot formally restart bombing without Congressional authorization he probably cannot get. The blockade and “defensive strikes” are his workaround. Iran knows this. It’s why they haven’t escalated beyond “reminder” missile launches.

Why the Market Is at All-Time Highs (The Honest Explanation)

It’s not irrational. It’s just pricing a very specific scenario: the MoU gets signed this week, oil falls to $80-85, inflation expectations collapse, the Fed cuts in June, and AI spending continues regardless of wars. In THAT scenario, current equity valuations are defensible.

The market is not pricing the alternative: deal falls apart, Trump bombs power plants to save face, oil spikes back to $115, Senate refuses authorization, Congress forces a pullback, Iran’s “reminder” missiles become something bigger. That scenario would take the S&P back to 5,500 in approximately one month.

The market is essentially a prediction market right now. It has assigned roughly 70-75% probability to the deal happening within 2 weeks, and 25-30% to renewed escalation. The 70% has been bid up to record highs. The 30% is sitting quietly in your energy stocks and gold holdings, waiting.

The Week Ahead: What Actually Matters

-

-

-

- Tuesday: Iran’s formal response to the MoU is supposedly due. This is the most important piece of paper in global finance right now. If Iran says yes, oil falls $10, stocks add 2%. If Iran says “in due time” (classic), markets shrug. If Iran says no, markets drop 2-3% and oil spikes.

- Wednesday: OPEC+ meeting. They are expected to extend production cuts. Given that oil has fallen 17% in May on deal optimism, they have every incentive to cut production now, which would put a floor under oil at $85-88 regardless of what Iran decides.

- Friday: Non-farm payrolls. First jobs report to fully capture the May economic picture — which includes the ceasefire, the deal optimism rally, the oil drop, and the AI boom. Expected to show modest recovery from February’s -92,000 shock. A miss here reopens the recession conversation.

- The honest bottom line: Nothing really matters — until it does. The market is right that a deal is closer than at any point since February 28th. The market is wrong that a deal is done. The Situation Room meeting produced a “few more days to think about it.” There are 840 tankers stranded in the Gulf and Iran fired missiles over the weekend. The S&P is at all-time highs.

-

-

Freddie Mercury would understand perfectly.

So there we are!

Still not really in a place where I want to start BUYBUYBUYing all these overpriced stocks but look at Dell – and that is STILL only 20x forward earnings – cheap by AI standards. Dell is a $279Bn company at $425/share – one of these multi-Trillion dollar Hyperscalers should buy them for $300Bn and add $11Bn in profits times, for example, Alphabet’s 27x forward earning is $297Bn so GOOGL would be picking up DELL for free and then, every time you search for “Computer” – Dell would suddenly be at the top of all your search results. Brilliant!!!

Anyway, in other news: Economic Data is coming in hot out of the gate this morning with PMI Manufacturing, ISM and Construction Spending – all after the bell. Beth Hammack is the only scheduled Fed speaker ahead of the June 17th meeting and she speaks ahead of JOLTS tomorrow (10 am). ADP Employment gives us no idea what NFP will be but they release it anyway on Wednesday, along with PMI Composite, Factory Orders, ISM Services and the Beige Book – during our Live Trading Webinar – that’s always fun. Thursday it will be Job Cuts, Productivity (hugely important) and Friday is the Big Kahuna, Non-Farm Payrolls and then Consumer Credit at 3pm.

I’m exhausted just previewing it – now we have to live through it!

Amazingly, there are still a lot of companies that haven’t had earnings yet – including Medtronic (MDT), who we just added at a Top Trade Idea on the 18th. Hopefully they say “AI” and double up overnight (that’s how we used to do it in the Dot Com days!).

HPE will be interesting and DG, should be telling. VSCO is an old favorite and, in this economy, girls gotta look good for their rich boyfriends – so I think they are doing well. SIG should be doing well as Trillions of Dollars of newly-created wealth buys a lot of rocks. PANW will be interesting, ULTA is probably too cheap, PETS at $2.20 may be one we have to add to the $700/Month Portfolio (review tomorrow). Macy’s (M) is still very cheap, AVGO is one of my all-time favorites, but not at $456 (25x), CRWD will be vitally important, FIVE will give us good consumer insight, WOOF will depend on how PETS goes.

We have LULU and I’ll be curious to see how DOCU is doing as well – those are the top of my watch list for the week.

{kind=link}

It’s hard to get back into a 5-day week after a 4-day week so grab some coffee – because it’s going to be crazy!