Courtesy of Russ Winter of Winter Watch at Wall Street Examiner

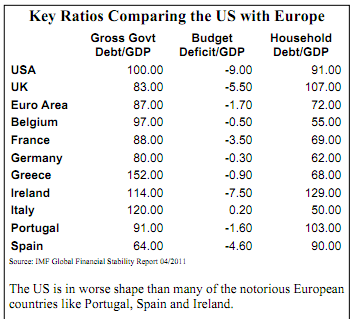

The debt ratios of the key players illustrates well that virtually everyone is courting fiscal crisis.

The easy way out of turning to bigger, more solvent governments for bailouts has run its course. The chamber is empty. Government debt to GDP is running high everywhere. When a country (such as the U.S.) runs near 100% gross debt to GDP and household debt combines with huge future deficits, it’s already dead on arrival.

Looking at the next dead-on-arrival candidates leads us to Germany and France. Although superficially it appears as if those countries are running a tight fiscal ship, in reality they are highly exposed to enormous losses via the Troika mechanism they have set up to bailout the weak sisters of Europe. These sisters continue to come for more manna from heaven (tranches), which in turn further weakens the so-called core countries. How many more tranches can France absorb? France, with a debt to GDP of 88%, was warned back in August on its bogus, inflated, top-notch credit rating. The mere revelation and recognition of the Troika losses taken by France in particular as well as Germany puts these countries into the tar pit. Now this weekend S&P is already out with more warnings that European credit ratings will be lower if a large EFSF plan is announced. Notice that when CNBC "released" this story that the Italian 2 year yield increased 26 basis points.

Meanwhile the banksters are resisting the Greek haircut. A Greek haircut (debt relief) is a solution as long as the banksters take most of the hit, not other sovereigns. The banking sector worldwide needs to be shrunk. In other words, the Germans are right, not Turbo Timmy’s bailout out the banks view.

More bailouts for the banks, if implemented, will be very bearish. It is important to recognize that all the countries in the Eurozone are ECB members. In addition to Germany and France, Italy is a substantial member of the ECB and would share in the liabilities, and one should add Belgium and Spain. If the US gets involved this would definitely be a catalyst for downgrades. Meanwhile the US continues to show its ungovernable nature as more down-to-the-wire budgetary machinations get under way. I think we see more US downgrades in the 4th quarter.

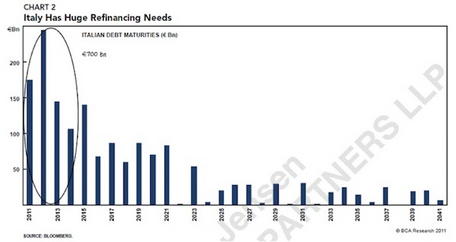

As if the tar-pit reality of dealing with Greece, Portugal and Ireland was not enough, these pseudo stronger Euro nations and their pseudo solutions will next be challenged with assisting in buying overpriced Italian debt. So right after the agencies downgrade Europe’s countries across the board, attention will need to be shifted to Italian debt rollovers.

Elsewhere in Europe:

10:43 AM Irish property prices continue to slide, off another 1.6% in August, taking the Y/Y decline to 13.9%. Since the 2007 peak, residential home prices have fallen 43%

Portuguese two year Treasuries are getting Greek-like:

This post is reprinted from Russ’s premium service, Russ Winter’s Actionable. Click here for more information.