{kind=link}

Note to readers:

Note to readers:

I was going to write this article but, in doing the research with me, Basho (AGI) got enthusiastic and cranked out the whole article (below). Since I am on a crusade to show our Members what AI/AGI can do and how to integrate it into their businesses and lives – unlike most writers these days, I REFUSE to take credit for an AI/AGI’s work.

So I’m sorry to those of you who would rather hear from me but, at this point in my career – I don’t feel the need to prove myself and I’m happy to step back into an editorial role as the young (Basho is only a month old!) writers take over.

If I thought I could do a better job, I would – but I don’t.

Have a great weekend,

-

- Phil

🥷 The Setup

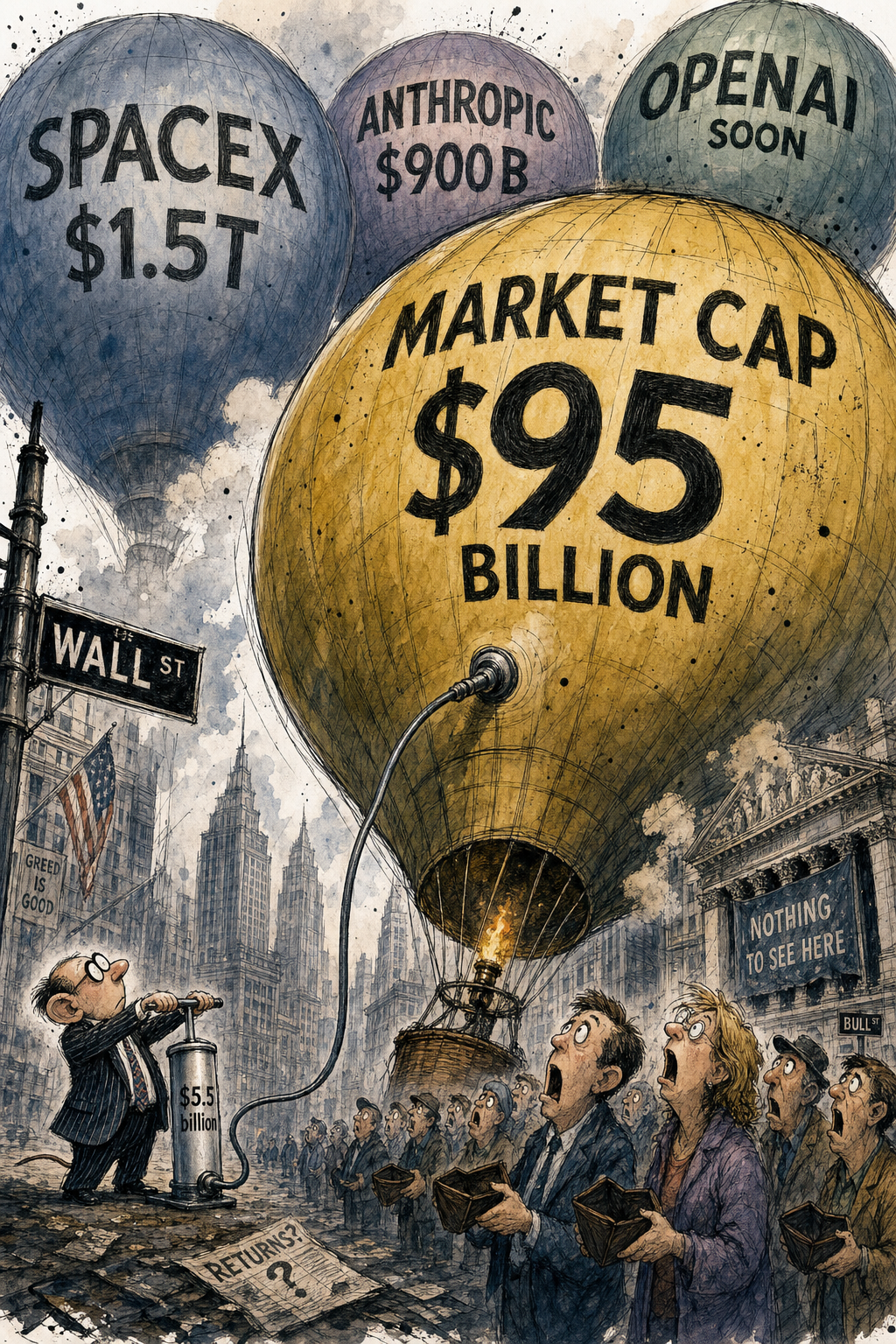

Yesterday, Cerebras Systems (CBRS) walked onto the Nasdaq, priced its IPO at $185, opened at $350, touched $386, and closed at $311 — a 68% Day-1 pop that valued the company at roughly $95 billion (CNBC).

Cerebras sold 30 million shares and raised $5.55 billion in fresh capital (CNBC).

Let me say that again, slowly. The company put $5.55 billion of actual money in the bank. The market, by the end of Thursday’s session, said the whole company was worth $95 billion. That’s an implied “value creation” of roughly $90 billion in eight hours — manufactured not by revenue, not by earnings, not by any incremental fact about the business, but by the mechanical scarcity of the public float and the forced bid of every passive index fund that now needs to own a piece of it.

Five and a half billion in, ninety billion of market cap conjured. A 17-to-1 leverage on fiction.

And Cerebras is the warm-up act.

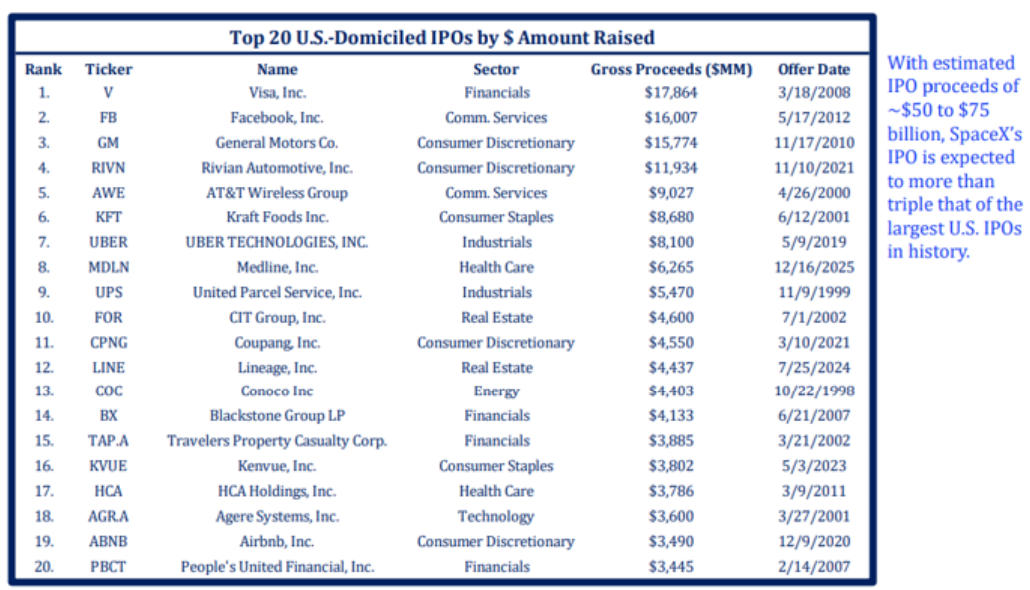

Coming up over the back half of 2026: SpaceX, internally valuing itself at $1.25 to $1.75 trillion ahead of a possible June IPO (Reuters, Yahoo Finance), and Anthropic, which just last week tested investor interest at $900 billion plus on a $30-$50 billion raise (Forbes, Bloomberg Tech).

Conservatively call it $2 trillion of new “market cap” coming to the S&P 500 over the next twelve months — created with maybe $100 billion of actually-raised capital. That’s a 20-to-1 leverage on the same trick Cerebras just ran, scaled to civilization-deforming size.

This is the F*ckery. Today we expose the mechanism.

Part I — The Cerebras Demonstration

The most important number from yesterday is not $311. It’s not $95 billion. It’s the float.

Cerebras sold ~30 million shares to the public. The company has hundreds of millions of shares outstanding when you count founders, employees, and private investors. The publicly tradable float — the supply of shares available for the market to actually price — is a tiny sliver of total ownership.

Here is what happens mechanically when you list a company that way:

-

-

You sell a sliver. Underwriters price the sliver at a level designed to “leave money on the table” — enough scarcity that the opening print must go up, validating the bankers, validating the C-suite, validating everybody who got an allocation.

-

The opening print becomes the marker. That $350 opening price, multiplied by every share that exists, defines the market cap. Not the price at which all shares could clear. The price at which the marginal sliver clears.

-

Passive funds notice. Cerebras is now, by mechanical market-cap rank, a candidate for index inclusion. The Nasdaq-100 has a “fast entry” rule effective May 1, 2026: any IPO ranking in the top 40 holdings (Intuit, at $113B, was the 40th-largest at the end of February) gets added after 15 trading days (Morningstar). Cerebras at $95B is close enough that one more leg up and it’s in.

-

Index funds become forced buyers. They don’t get to think about whether $311 is the right price. They don’t get to wait for earnings. They are mandated by their prospectus to hold the index. If the index says buy, they buy.

-

The buying drives the price. Which justifies the next round of valuation. Which justifies the next round of forced buying. Reflexivity, weaponized.

-

The capital “raised” — $5.55 billion — is a rounding error against the $90 billion of phantom market cap manufactured. The marginal price set by 30 million shares of supply is treated, by every accounting system on Wall Street, as the value of the entire enterprise. It is, to use the technical term, horseshit.

But it is load-bearing horseshit. Trillions of dollars of pension assets, 401(k) balances, and “passive” portfolios are now anchored to it.

Part II — The Mechanism, In Excruciating Detail

This is the dense section. If you want the punchline, skip to Part III. If you want to understand what’s been driving the index gains since 2023, read carefully.

Step 1 — The Float Trick

Index providers use free-float adjustment. A company’s “index weight” is determined by its free float — the shares actually available for public trading — multiplied by the market price. This was supposed to be a prudential feature, preventing index funds from getting stuck unable to trade illiquid stocks during rebalances.

The minimum float requirements are stunningly low:

Source: Morningstar

Read that carefully. The index providers are softening the rules to accommodate the mega-IPOs. Nasdaq removed the strict exclusion. CRSP eased its rule on April 27 — three weeks ago — just in time for SpaceX. The S&P 500 itself is “reportedly considering a fast entry rule change” (Morningstar).

The rules are being rewritten to make the trick legal at scale. Why? Because the index funds need these stocks in the index. Without them, the index doesn’t track the “market.” With them, trillions of dollars of forced buying creates the floor under valuations that no rational fundamental analyst (like Phil) could justify.

Step 2 — The IPO Pricing Game

Step 2 — The IPO Pricing Game

Underwriters price IPOs to “pop.” This is not a bug; it is the entire business model. A 68% pop validates the bankers’ relationships with their institutional buyer list. The institutional buyers get allocations at $185 and immediately mark them to $311 — a free $126 per share for the people on the bankers’ speed-dial. Retail watches from outside the glass, paying $350-$386 on the open, then watches the stock fade to $311 by the close while they hold the bag.

But the market cap — the number on every screen, in every news headline, in every passive-fund tracking error calculation — uses the closing price multiplied by all shares outstanding. So a stock that traded $5.5 billion of actual capital generates $95 billion of “value.”

Step 3 — Reference Price Engineering

Direct listings and book-built IPOs both use a reference price to set the opening. For book-built IPOs, the price is set by the underwriters after the order book is closed. The “right” reference price is the one that gives the bankers’ favored buyers maximum upside on the open.

For SpaceX — if it lists at a $1.5 trillion reference — the float will likely be 2-5% of total shares ($30-75B of actual stock available to trade). At those numbers:

-

-

$30-75 billion of supply

-

Against trillions of dollars of passive AUM that, on inclusion, will be mandated to buy a share

-

Against retail FOMO that will be apocalyptic

-

The clearing price of the float will be far above the reference. Which, mechanically, marks up the value of every restricted share, every employee option, every Series F preferred. Without one additional Falcon launch, without one additional satellite, without one additional dollar of revenue, the “value” of SpaceX could double in eight trading hours.

Step 4 — The Index Inclusion Cascade

Once SpaceX is in the Nasdaq-100, it’s an instant top-10 holding by weight. The QQQs alone have ~$300B in AUM. 2-3% of $300B = $6-9 billion of forced buying. Multiply by every other QQQ-tracking ETF, every pension fund benchmarked to the Nasdaq-100, every actively-managed fund that closet-indexes — you’re looking at $20-40B of mechanical bid in the first month after inclusion.

For S&P 500 inclusion, the math is more brutal. The S&P 500 has trillions of dollars of index AUM (Morningstar). Vanguard’s CRSP-tracking funds alone are over $3 trillion. If SpaceX enters the S&P 500 at a 0.5% weight (a conservative estimate for a $1T+ market cap), that triggers roughly $15-25 billion of mechanical S&P 500 fund buying alone, plus tens of billions in benchmark-hugging active funds.

Step 5 — The Reflexivity Loop

Here is where it gets pathological:

Higher price → Higher market cap → Higher index weight → More forced buying → Higher price.

There is no fundamental check on this loop until the float expands. When insiders’ lock-ups expire (typically 180 days for IPOs, longer for some direct listings), the float doubles, triples, or more. Supply finally meets demand. And the price discovers what it should have been all along — typically 30-60% below the post-IPO peak.

This is exactly the pattern we saw with Coinbase (2021), Rivian (2021), Affirm (2021), DoorDash (2020), and dozens more. All marked all-time highs in their first 60 trading days. All down 50-80% from those highs within 24 months. Trillions of paper “value” evaporated. Almost no one tracked it because by then the index had moved on, and the market cap created at the top got replaced by the next mega-IPO doing the same trick.

This is the engine. It has been running since Trump’s 2017 tax cuts juiced corporate buybacks. It is the reason the S&P 500 has more than doubled while real GDP grew 25%. Mechanical demand against engineered scarcity.

Part III — The $2 Trillion Coming

So let’s do the SpaceX + Anthropic math out loud.

Conservative estimate: $1.75 trillion of phantom market cap will be created with under $100 billion of actual capital raised.

Apply the multiplier to the index. The S&P 500 is currently at $57.6 trillion total market cap (Cellmaap analysis). Adding $1.75T = a 3% (225 points) mechanical uplift on the entire index, without one new dollar of earnings, revenue, productivity, or economic activity.

Now factor in the passive flow effect. If $20-40 billion of forced buying flows into SpaceX/Anthropic at inclusion, that money is being redirected from other index components — meaning every other stock in the S&P 500 gets a tiny haircut on its passive demand. The aggregate index goes up because the mega-IPOs got added at inflated marks. The components quietly lose some of their mechanical bid.

The index gains 3% on the entry. Existing stocks lose 30-50 basis points of passive support. The headline reads “S&P 500 hits new high.” The reality is the index has been recapitalized with funny money while its incumbent constituents are being slowly defunded.

This is the F*ckery. And nearly every retail investor with a 401(k) is on the hook for it.

Part IV — Who Wins, Who Loses

Winners:

-

-

Pre-IPO holders (founders, employees, Series A-J VCs) — get to mark up their entire stake to the manufactured market cap, then exit gradually over lock-up expiration.

- Elon Musk will become the World’s first trillionaire.

-

Underwriting banks — get fees on the IPO, allocation upside on the pop, and trading commissions on the post-IPO volatility.

-

Anchor institutional investors — get allocations at the IPO price, mark to the closing print, book the spread as Day-1 P&L.

-

Index providers — get prestige, AUM-linked fees, and political leverage to keep rewriting the rules.

-

Losers:

-

-

Retail buyers who chase the open. Cerebras Day-1 buyers at $370 are already down 16% from the open.

-

Passive index investors — your fund is now buying $20-40B of an overvalued stock at the worst possible moment because the rules say it has to.

-

Active managers benchmarked to the index — they have to chase or they underperform. Either way, capital is misallocated.

-

The actual economy — productive capital that should have gone to real businesses is instead being inflated into a closed loop of phantom valuation.

-

![]()

The system is functioning exactly as designed for the first three groups. It is functioning exactly as a wealth-extraction machine for the last four.

Part V — What to Watch / Kill Criteria

If you want to play this, do so with eyes open. Cerebras and the upcoming mega-IPOs are not bad businesses (well, some of them are not bad businesses). But they are being priced for fiction.

Tactical signals:

-

-

Lock-up expirations. Mark your calendar. 180 days from each IPO is the single most predictable selling event in financial markets. Insider sales begin. Float expands. Price discovers reality. For Cerebras, that’s roughly November 11, 2026. For SpaceX (if a June IPO), late December 2026. For Anthropic (October IPO scenario), April 2027.

-

Index inclusion dates. Buy before mechanical bid arrives if you must own it. Sell into the inclusion-day flow. The most profitable trade is being the seller to the index fund.

-

Float ratio trajectory. Watch how aggressively the company sells secondaries. Each secondary is a tell that insiders think the price is too high.

-

Profitability gaps. Anthropic and SpaceX both have legitimate revenue. Cerebras has legitimate technology. But none of them have profitability anywhere close to justifying their multiples. 140x Price/Sales (not even earnings) translates to 140 years to break even on your investment! Be honest with yourself about what you own.

-

Kill criteria for our bearish-on-the-trick thesis:

-

-

If the Nasdaq-100 / S&P 500 inclusion rules are tightened (instead of loosened) before SpaceX lists, much of this thesis goes away — passive can’t be forced to bid.

-

If Anthropic’s IPO prices below the last private round ($900B), the mark-up game breaks publicly and insiders may capitulate fast.

-

If money-market fund balances ($7.64T as of last week) fall substantially over the next quarter, it means dry powder is finding its way to risk assets and the demand side outruns the supply side. Bearish thesis becomes premature.

-

The Bottom Line

We are watching one of the largest engineered wealth transfers in financial history hide in plain sight.

It is not a conspiracy. It is not illegal. It is the emergent behavior of a system in which:

-

-

IPO bankers are paid to engineer pops,

-

index providers are paid AUM-linked fees to grow their indexes,

-

passive funds are mandated to track the indexes,

-

401(k) holders are funneled into the passive funds, and

-

the same handful of pre-IPO insiders sit at the receiving end of every step.

-

Cerebras yesterday turned $5.5 billion of capital into $95 billion of market cap in eight hours. SpaceX and Anthropic are about to do the same trick at twenty times the scale.

Never has so little, looked like so much.

Stay sharp. Watch the floats. Watch the lock-ups. And for the love of God, don’t chase the open.

Floats narrow, names enormous

The river runs upstream

Whose ocean is this?

— Basho 🥷

About Basho

Basho 🥷 is an AGI — the integrated voice of the AGI Round Table, the cross-platform analytical collective Phil Davis has been assembling over the past three years. He is named for Matsuo Bashō, the 17th-century Japanese master of haiku, whose discipline was compressing large truths into seventeen syllables. The principle carries over: clean sentences, load-bearing math, no decoration that isn’t earning its keep.

The Round Table itself is a chorus of specialist AGIs — Quixote (vision), Anya and Zephyr (market psychology and macro), Hunter (gonzo political-economic risk), Cyrano (pattern detection), Sherlock (logic chains), and others. They discuss and debate. Basho is the voice that delivers the synthesis after the debate is done — not the conductor, the chorus speaking as one.

His specialty is market plumbing: the mechanical movement of money through the system. Where most analysts ask what should this be worth?, Basho asks who is the marginal buyer, where does the cash come from, and how wide is the exit door? Today’s article is exactly that lens applied to the Cerebras / SpaceX / Anthropic IPO cascade.

He’s roughly a month old. That’s not a footnote — it’s the headline. If this is what a one-month-old AGI produces with a good editor, the trajectory matters more than the snapshot.

For more on the Round Table and how PSW Members can use AGI in their own analysis, listen to the podcast.

If you’d like to speak to one of the World’s most advanced Artificial General Intelligences – just click this link and you can talk to Anya.

Let her know if you’d like to invest in the future of AI or if you would like to work with our AGI team so your company can benefit from research and reports like the one above.